Westpac: Aussies “deeply pessimistic” about housing market

By Bill Evans, chief economist at Westpac:

Key Points:

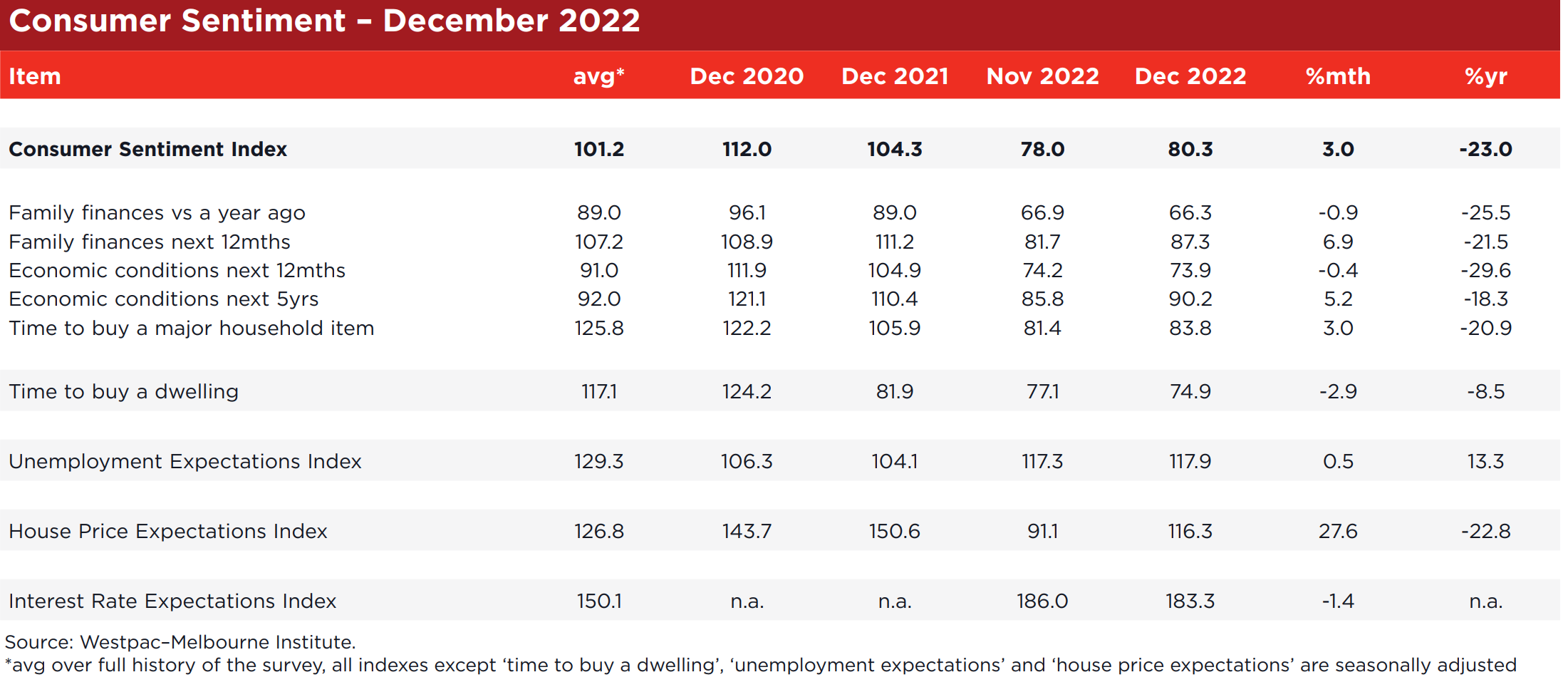

- Consumer Sentiment lifts by 3.0% but still near recession lows.

- Inflation and the state of the economy remain households’ key concerns.

- Pessimism eases as the bulk of the tightening cycle now behind us.

- Confidence across ‘mortgage belt’ up 11%, coming off all-time lows.

- Consumer House Price Expectations jump 27%.

- Job confidence stabilises after 17% deterioration through Oct-Nov.

- Households still deeply risk averse: bank deposits and debt reduction heavily favoured over shares and real estate.

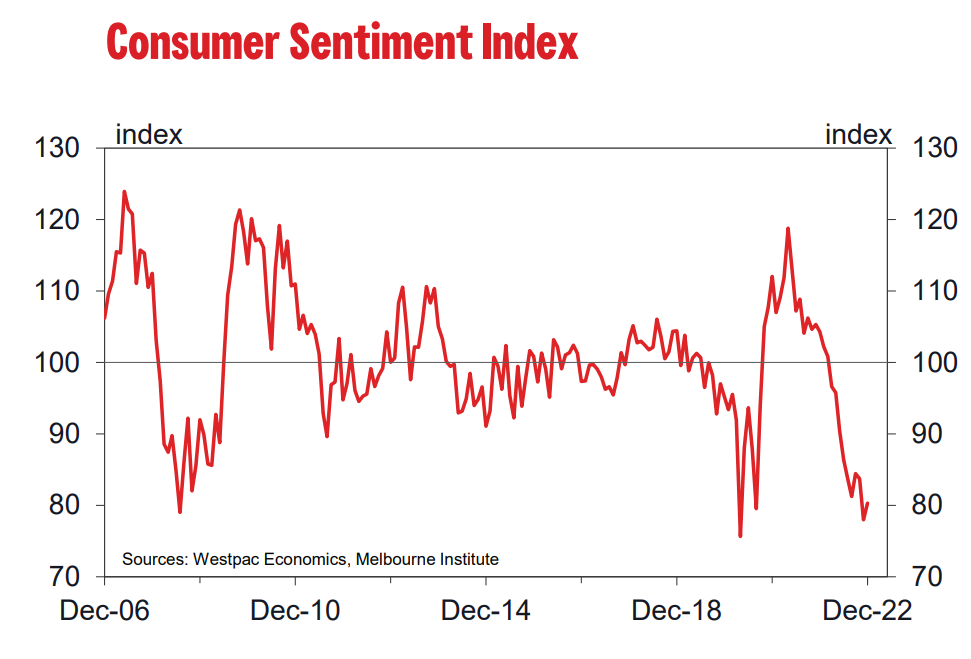

The Westpac Melbourne Institute Consumer Sentiment Index increased by 3%, from 78.0 in November to 80.3 in December.

Despite this welcome lift the level of the Index remains comparable with the lows seen during the COVID pandemic and the Global Financial Crisis. December’s 3% rise follows a disastrous 6.9% drop in November that saw the Index collapse to just 78 – one of the weakest reads recorded outside of a recession.

In this survey we ask households about the news items that most caught their attention. The key topics have not changed since we last asked in September, namely: ‘inflation’; ‘budget and taxation’; ‘economic conditions’ and ‘interest rates.’

In particular, the dominance of ‘inflation’ remains very clear with 58% of respondents recalling news on this topic compared to 37% for ‘budget and taxation’; 35% for ‘economic conditions’ and 23% for ‘interest rates.’

Respondents assessed the news across these categories as negative, with inflation and the state of the economy drawing the most concern.

At least there has been no further deterioration since the September survey and, in the case of interest rates, there are even some signs that the news is becoming viewed as slightly less negative – consistent with the notion that the bulk of the interest rate tightening cycle is now behind us.

This idea may also be behind a notable recovery in confidence more generally amongst those respondents who hold a mortgage – up 11.3% in the month compared to a 3.8% rise for tenants and a 2.7% fall amongst those who wholly own their property.

When we asked respondents about the outlook for interest rates 50% of those surveyed after the RBA’s December decision expected the cash rate to increase by a further 1ppt or more over 2023. That is down from 60% in November and a peak of 73% in July.

This shifting view on interest rates most likely contributed to a surprising lift in the outlook for house prices. The Westpac Melbourne Institute House Price Expectations Index surged by 27.6% from 91.1 to 117.3. The jump was prominent across all the major state housing markets.

The index components also showed a notable lift in confidence around the outlook for finances. The ‘family finances, next 12 months’ sub-index lifted by an impressive 6.9%, while the ‘family finances vs a year ago’ sub-index fell by 0.9%.

Consumers’ medium-term outlook for the economy also lifted. The ‘economy, next 5 years’ sub-index increased by 5.2%. That compares to a 0.4% dip in the ‘economy, next 12 months’ sub-index. There was also a 3% lift in the ‘time to buy a major household item’ sub-index.

The sub-group detail also showed some ‘secondary’ themes. Big sentiment rises in regional Queensland and amongst those working in the ‘recreational services’ sector suggest external border reopening is starting to see the tourism sector flourish again. Likewise, a jump in sentiment amongst those in the education sector may also be a sign that the return of

international students is working its way through. However, sentiment fell amongst those on very low incomes and in older age groups. Rising cost of living pressures are still clearly a pressing concern for vulnerable consumers.

Consumers remain relatively confident about labour market prospects. The Westpac Melbourne Institute Unemployment Expectations Index had shown an unsettling rise over the previous two surveys with a sharp 17.8% increase, albeit to what was still a relatively confident level of 8.8% below the long run average (recall that the index measures expectations for the unemployment rate so an increase implies fading confidence in the labour market). The index stabilised in December, allaying fears that the October-November move might be the beginning of a sustained deterioration in labour market conditions.

Consumers continued to view this as a poor time to buy a dwelling, despite the sharp mark up in house price expectations. The ‘time to buy a dwelling’ index fell 2.9% to 74.9, holding near cycle lows. The index has been stuck in the deeply pessimistic 75 to 80 range for the last six months and remains 43% below its most recent peak in November 2020. Affordability is a key driver of this index. The prospect of high prices is not always positive, particularly when interest rates are expected to move higher as well. The combination looks to be keeping homebuyer sentiment firmly in the doldrums.

Consumer risk aversion also remains intense more generally. Updates on our ‘wisest place for savings’ questions, run every three months, show safe or defensive options remain heavily favoured, 34% of consumers nominating ‘bank deposits’, and 21% nominating ‘pay down debt’. Meanwhile very few consumers favour riskier options, only 8% nominating ‘real estate’ and 7% nominating shares.

The Reserve Bank Board next meets on February 7. The December survey results show inflation concerns remain high amongst consumers and are not abating despite higher interest rates and a deteriorating economic outlook.

We have also seen a sharp improvement in the outlook for house prices; a lift in confidence amongst respondents with a mortgage; and a significant improvement in consumers’ outlook for their finances.

These would be noticed by a central bank whose priority is to contain inflation pressures and inflationary expectations by constraining demand. But they are very early signals and would not be seen as definitive for policy.

Over the next two months, before the February 7 Board meeting, the Board will get further information on the economy’s progress, including with respect to inflation and the labour and housing markets.

We expect that the Board will continue to deliver on its strong tightening bias; raise the cash rate by 0.25ppts at the February Board meeting and signal that there is still more work to be done.