The $200 billion Term Funding Facility (TFF) was the emergency funding facility deployed by the RBA during the March 2020 COVID crash to prevent banks from experiencing a credit crunch as global credit market froze up.

It offered banks next-to-free (0.1%) money in place of existing bonds that were much more expensive, with the aim of providing support to businesses during the pandemic-induced economic downturn. The term of this ‘free’ money was three years.

RBA analysts have undertaken a review of the TFF and concluded that there was little evidence that it increased overall lending, particularly to the small and medium enterprise sector:

“Lending growth was greater for TFF-eligible banks than for ineligible non-banks, but this was driven mostly by large businesses drawing on credit lines,” which tended to be paid back quickly, the authors said.

“Total lending to businesses was approximately steady for much of the rest of the TFF drawdown period, although aggregate lending to large businesses increased in mid-2021 as economic conditions improved.

“Meanwhile, aggregate lending to SMEs was little changed.”

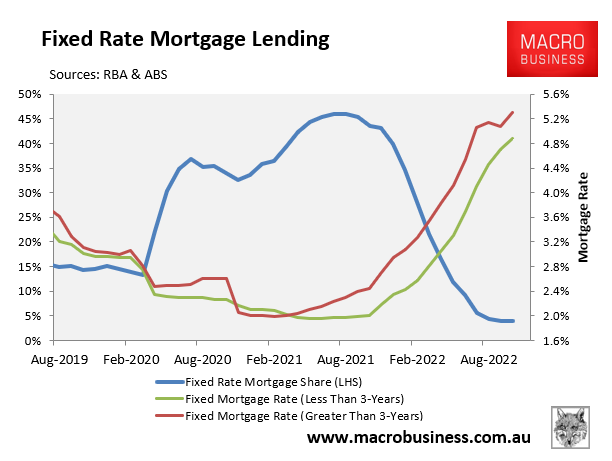

While the TFF did not boost business lending, it certainly did boost fixed rate mortgage lending.

As illustrated in the next chart, the TFF dropped fixed mortgage rates below 2%, which drove to the share of fixed rate mortgage lending from a long-term average of 15% to an all-time high 46% in mid-2021:

With the TFF now expired and central banks across the globe aggressively hiking interest rates, fixed mortgage rates have soared to more than double their pandemic level.

This poses a problem for the economy in 2023 as nearly one-in-four mortgages (by value) are reset to these higher rates.

In turn, the share of household income used to service principal and interest debt repayments will soar next year to its highest level in history.

The inevitable impact will be that household consumption will crater as more income is diverted away from spending towards debt repayments.