In July’s “Great Housing Debate” against Chris Joye, Stephen Koukoulas (‘The Kouk’) forecast a peak-to-trough fall in Australian dwelling values of only 7% based on the CoreLogic index.

This price forecast was on the back of an expected increase in the official cash rate to 3.0%, which was achieved at the December RBA meeting.

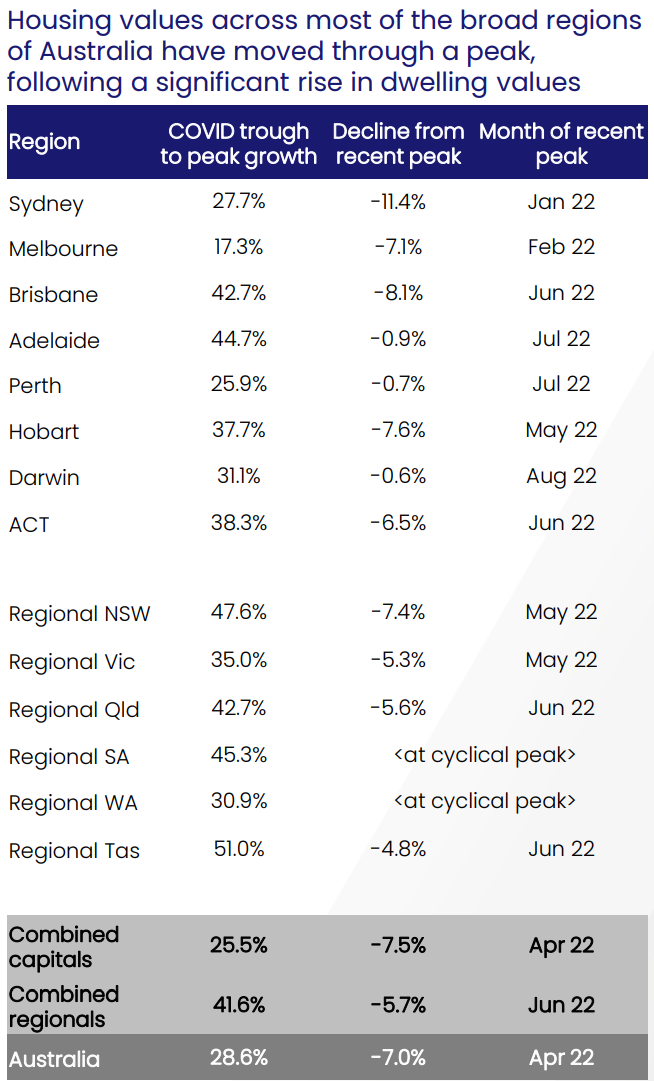

The Kouk’s forecast was already met at the end of November, with dwelling values nationally down 7.0% from peak, according to CoreLogic:

This week, the Kouk declared “the bottoming in house prices is near”, with prices only expected to fall another 3% to 4%:

“Prices are likely to have one final down-leg through to the first quarter of 2023 as a tightening in credit bites and the cyclical effect of the past couple of rate hikes impact. Prices could well edge down another 3% or 4%”, noted the Kouk.

Moreover, a “mix of factors suggests the time for a bottoming in house prices is near”.

These factors include the near term “peak in the interest rate hiking cycle” which will make borrowers “less fearful of taking out loans as a result”.

“A lift in housing demand from a resurgence in population growth will [also] be evident during 2023”, while “the ongoing strength in the labour market” will support house prices.

Finally, “building costs are rising at a pace relative to house prices”, meaning “supply will falter at the time demand is surging”.

It is no surprise that I view the Kouk’s house price forecasts as undercooked given the existing interest rate hikes (let alone further increases) are yet to fully work their way through the system.

Nearly one-in-four mortgages (by value) will also switch in 2023 from ultra-low fixed rates originated at around 2% to rates that are more than double these levels.

By far the biggest factor driving house prices is the cost of debt and borrowing capacity.

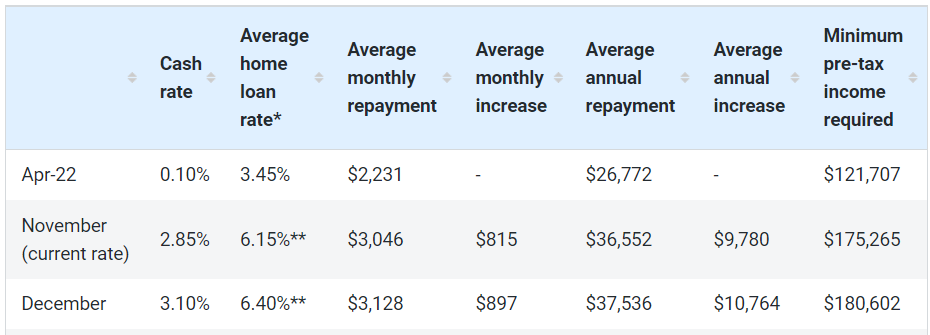

According to Finder, the amount of pre-tax income required to service a $500,000 mortgage has soared from around $121,000 in April 2022 to $181,000 as at December, following the RBA’s 3.0% of rate hikes:

Lower borrowing capacity equals lower house prices. The equation is that simple. And the more the RBA tightens, the further house prices will inevitably fall.