The Australia Institute (TAI) has lodged a submission to the review into the functions and operations of the Reserve Bank of Australia (RBA), which claims the Bank is “using wrong tools to fight inflation” and ignores the “economic power enjoyed by big business” due to the “composition of the Reserve Bank board”.

TAI instead calls for a greater focus on full employment, alternative methods of fighting inflation, as well as measures to insulate households negatively impacted by swings in interest rates.

Below are key extracts from TAI’s report.

__________________________________________________________________________________________

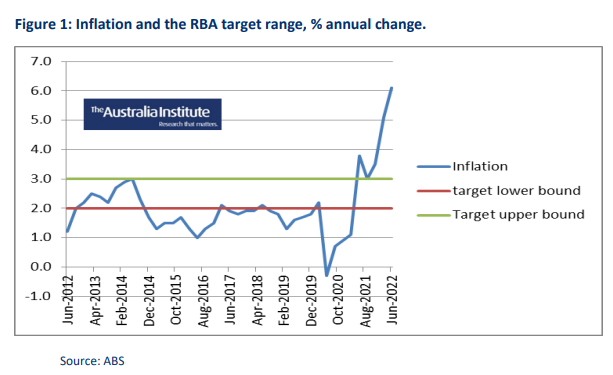

Despite its legislation, the RBA’s main objective today is fighting inflation and our assessment is that the outcomes have been poor. Its target of 2 to 3 per cent have been consistently missed over the last decade. We submit that the RBA has been using the wrong tools to fight inflation. It acts as if there is excess demand, especially in the labour market, and assumes that the appropriate approach is contractionary policy.

Recommendation: The RBA should adopt a policy of low inflation subject to success in delivering its other legislated targets including, of course, full employment. The RBA’s key performance indicator should be the performance of the economy overall…

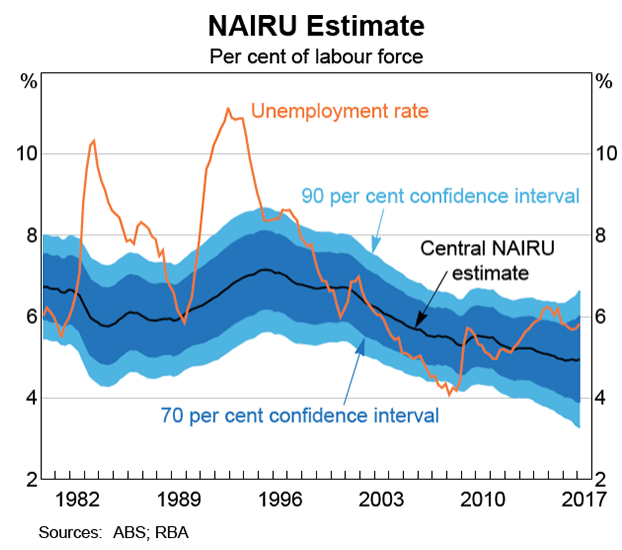

In that respect it has adopted features of neoliberalism including the use of the non-accelerating inflation rate of unemployment concept, a rate of unemployment to which the economy is automatically headed. In practice this amounts to assuming the economy is not far from the equilibrium rate of unemployment. From this the RBA can then claim it is not worth targeting unemployment and can instead concentrate on inflation…

As a final point on the NAIRU we want to point out that the obsession with the NAIRU means concentrating on the labour market as the source of any inflationary tendencies. Over time we have seen the price level increase relative to wages with a consequent increase in the profit share of national income. Against that background, demand increases in the last few yeas have allowed producers and other suppliers to increase their profit margins and so contribute to inflation…

Another aspect of this approach is being overly concerned about inflation expectations taking off among the workforce. Neoliberal models stress inflation expectations when business and workers are assumed to have more equal bargaining power.

The economic power enjoyed by big business is ignored in the RBA’s thinking. This suits the business interests that dominate the board of the RBA. Indeed, we argue that an important reason for the RBA’s bias towards business is the composition of the Reserve Bank board. The perception is that, under the guise of independence, business interests have captured the RBA. A good example was the RBA acting as apologist for big bank profits. Reforms to the RBA are needed to overturn its undemocratic nature. There is also a case for limiting senior staff movements between the private finance sector and government, including the RBA…

Recommendation: The RBA needs to study exactly how markups and corporate power have changed over the most recent business cycle to contribute to a better understanding of the recent inflation dynamics. The RBA needs to avoid using hypothetical constructs such as the NAIRU…

We point out that interest rate changes hurt ordinary households and so recommend that the use of monetary policy based on interest rate movements be used sparingly, rather than being a first-line method to impose austerity or provide economic stimulus. In addition, effort should be put into mitigating the effects of inflation rather than just fighting inflation. Simple indexation protects most people who receive government support and similar arrangements could apply to other income recipients…

We think the damage done by monetary policy is a good argument for keeping it in reserve and using other tools to manage the macroeconomy. It is indicative that high house prices and high debt levels are good for monetary policy because they mean households are forced to make significant changes to their spending in response to higher interest rates…

Recommendation: Monetary policy based on interest rate movements is a crude and harmful mechanism that needs to be used very sparingly. It should be treated as weak as a stimulus and cruel as an austerity tool. Interest rate increases need to be accompanied with an impact statement and an assessment of how the costs to affected individuals is weighed against any benefits from lower inflation…

At the moment minimum wages are adjusted for inflation and other factors just once a year. Those could be subject to more frequent indexation…

To mitigate the impact on indebted households the RBA should review the housing finance market and the role of the standard variable mortgage. The US, Denmark and France have fixed-rate long term housing loans while in Canada the rates are fixed for 5 years. We think there should be fixed interest loans in Australia reflecting the conditions prevailing at the time people finance housing.

A bank giving fixed rate housing loans may need to fund them with matching fixed rate liabilities. If the RBA loaned money with a 25-year maturity to home lenders it would match the maturity of the standard home loan. That could be done through a special RBA deposit with the home lender. There would be no risk to the home lender If those loans involved fixed interest rates and, in addition, the RBA deposits could be liquidated in the event that the retail customer paid off the loan…

To the extent that everyone is protected against inflation it is much less important that inflation be fought at all!..

Recommendation: The RBA initiate a research agenda that considers alternative methods of fighting inflation and the optimal approach to compensating various income groups for the effects of inflation. Where applicable, the RBA should advocate that all contractual forms of income should be subject to frequent indexation. Reforms in the home loan market are needed to insulate outstanding household debt from upward movements in interest rates.