By Gareth Aird, head of Australian economics at CBA

Key Points:

- The December 2022 Board Minutes were the last scheduled piece of communication from the RBA until the all-important February 2023 Board meeting.

- The Minutes indicate that the Board considered no change in the cash rate for the first time in the tightening cycle.

- We believe the tightening cycle is close to its completion. We reiterate our call that the peak in the cash rate will be 3.35% (i.e. one further 25bp rate hike).

The RBA has gone out of their way to show they are not on a pre-set path

The December Board Minutes were the last scheduled piece of communication from the RBA until the all-important February 2023 Board meeting. As such, the Minutes were the last opportunity the RBA has to guide the market ahead of the first Board meeting next year.

The Minutes indicate the Board considered the case to leave policy unchanged in December. This is a new development. Over the course of the tightening cycle to date the Board had not considered the case to leave policy unchanged. The disclosure today that the Board considered leaving monetary policy on hold in December means the RBA is close to pausing in the tightening cycle. That is certainly the impression we take from the Minutes today.

The Minutes indicate the Board also considered the case to increase the cash rate by 50bp or 25bp in December. It is unusual that the Board considered both increasing the cash rate by a bigger-than-usual 50bp and leaving policy on hold.

It appears that the RBA is going out of their way to show us that all options were on the table in December. However, the key piece of information to us in the December Minutes is the new information; namely that the Board considered leaving the cash rate on hold in December.

The RBA retains a hiking bias, as expected. But the Minutes somewhat water down that hiking bias. More specifically the Minutes note, “a further increase in the cash rate was likely to be necessary to achieve a more sustainable balance of demand and supply, but there had already been a material increase in the cash rate in a short period of time and there were lags in the operation of policy”. The ‘but’ implies that another rate hike is not a sure thing.

The Minutes also state that members, “noted the importance of acting consistently, and that shifting to either larger increases or pausing at this point with no clear impetus from the incoming data would create uncertainty about the Board’s reaction function.”

That makes sense. However, the Minutes state that “the monthly CPI indicator for October confirmed that inflation had remained high into the December quarter but, at 6.9%, the outcome was a little below market expectations”. Inflation data below expectations could be considered an impetus to pause. That said, the Minutes note that members acknowledged that the monthly series was still new and needed to be interpreted with caution.

The Minutes state that, “members noted that a range of options for the cash rate could be considered again at upcoming meetings in 2023. The Board did not rule out returning to larger increases if the situation warranted. Conversely, the Board is prepared to keep the cash rate unchanged for a period while it assesses the state of the economy and the inflation outlook.”

Overall, we are left with the impression that the RBA would like to pause in the tightening cycle. But we don’t know what they are willing to hang a pause on. The case to keep the cash rate unchanged for a period of time to assess the state of the economy and the inflation outlook is strong. And yet the Board has not stated when that condition will be met.

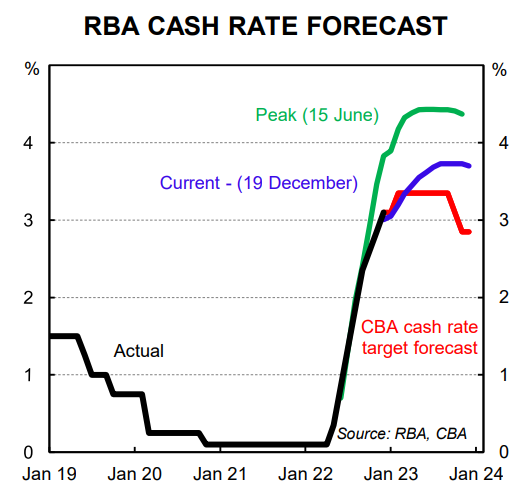

In summary the RBA’s forward guidance is sufficiently vague that all options will be on the table at the February 2023 Board meeting. Our base case is unchanged. We expect one further 25bp rate hike in early 2023 that would take the cash rate to 3.35%. We continue to expect rate cuts in late 2023 and have pencilled in 50bp of easing in Q4 23.

This is the final note of 2022 from the Australian Economics team. I would like to wish all of our readers a happy and healthy Christmas and New Year.