In its commentary accompanying Tuesday’s monetary policy decision, which lifted the official cash rate (OCR) another 0.25%, RBA governor Phil Lowe warned that “inflation in Australia is too high” and that “the Board expects to increase interest rates further over the period ahead, but it is not on a pre-set course”.

Lowe also acknowledged “there has been a substantial cumulative increase in interest rates since May” and “monetary policy operates with a lag and the full effect of the increase in interest rates is yet to be felt in mortgage payments”.

The big four banks’ current OCR forecasts are as follows:

- CBA: 3.35% by February 2023, then dropping to 2.85% by December 2023.

- NAB: 3.6% by March 2023, remaining steady into 2024.

- Westpac: 3.85% by May 2023, then dropping to 2.85% by November 2024.

- ANZ: 3.85% by May 2023, then dropping to 3.5% by November 2024.

Financial markets are also tipping a peak OCR of 3.6% by August 2023.

Therefore, based on these forecasts, the OCR will rise by between 0.25% and 0.75% from its current level of 3.1%.

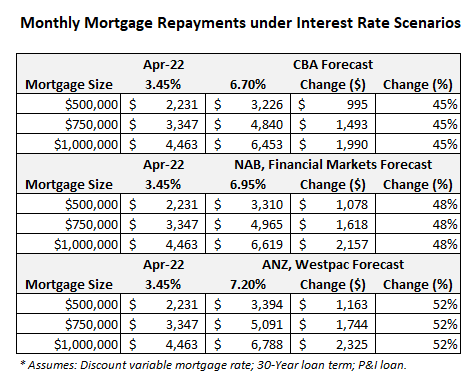

The impact on Australian mortgage holders from the above forecasts is illustrated in the below table, compared against interest rate settings in April 2022 immediately before the RBA’s first rate hike:

Depending on the OCR forecast, average variable mortgage repayments will rise by between 45% and 52% from their April 2022 pre-tightening level, adding between $995 and $1,163 in monthly repayments to a $500,000 mortgage.

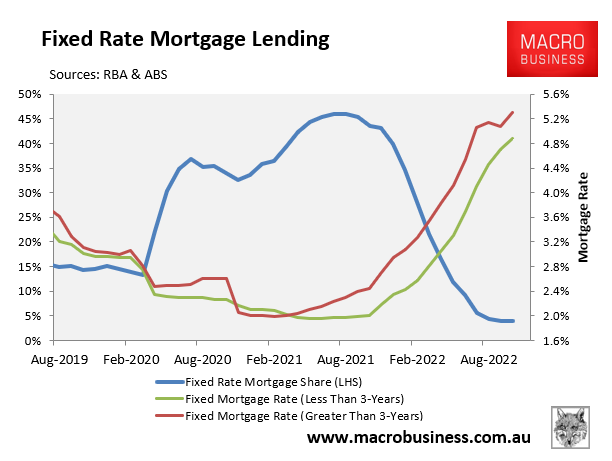

To add further insult to injury, the share of Aussie home buyers that took out fixed rate mortgages surged over the pandemic from a long-term average of around 15% to an all-time high 46% in mid-2021:

Nearly one-in-four mortgages (by value) will switch in 2023 from ultra-low fixed rates originated at around 2% to rates that are more than double these levels.

As a consequence, monetary conditions will tighten further in 2023 without additional OCR hikes from the RBA.

Finally, it is worth pointing out that the cumulative 3% increase in the OCR now matches the 300 basis point buffer on home loan serviceability assessment introduced by APRA in October last year and is 50 basis points above the previous 250 basis point buffer.

Accordingly, many borrowers rolling off ultra-low fixed mortgage rates will find themselves in extreme financial stress, with some unable to pay.

Thankfully, the RBA does not meet in January and Australian mortgage holders will be spared a ninth consecutive monthly rate hike.

Hopefully by the February meeting, the impact of the extraordinary tightening to date becomes apparent and prompts the RBA to stop hiking.