In this week’s issue of Tony’s View, independent economist Tony Alexander looks at the many factors that will stabilise New Zealand’s housing market in 2023, setting the scene for a cyclical recovery into 2024.

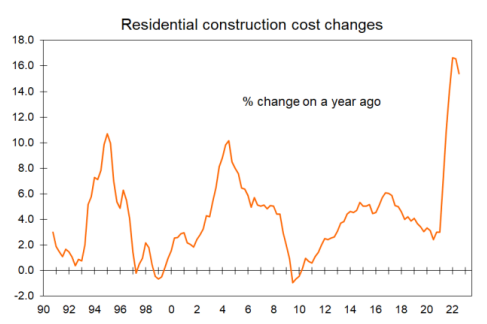

Rising construction costs

Rising construction costs provide a natural floor to overall house price levels and are one of at least seven factors coming together to change the house price outlook from some point probably in the first half of next year – but not now. The negatives dominate currently, and it would be premature to argue that the downward phase of the house price cycle has reached its natural end.

Rising incomes

The second factor which will act to catch house prices as they fall is rising household incomes…

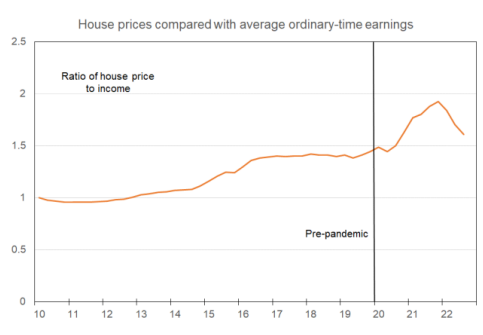

Average house prices are 26% higher than prepandemic levels. But average hourly earnings have increased by 8.6% in the past year and 3.6% the year before, making for a 14% gain from before the pandemic.

The ratio of house prices to this income measure was 30% above pre-pandemic levels at the end of last year. Now the gap is only 8% and falling fast. We may be able to say that by the end of this year this ratio will have retreated back to pre-pandemic levels.

This does not mean affordability is back to those levels because of the rise in interest rates. But that is where the third underlying trend factor relevant to the house price cycle comes into play. Interest rates.

Rising incomes

Fixed mortgage rates are probably now at their cyclical peaks This may not be accepted for a while, and we cannot completely rule out banks increasing their lending margins further…

The attention people have on interest rates for the moment is all around how much higher they will go. Then it will shift to where they peak, then how quickly they will fall. I reckon the fall will be slow because the recession – if one occurs – will be shallow. But my view that fixed rates have now probably peaked means the next shift in focus will be to accepting the worst-case scenario for debt servicing costs. As soon as people start doing that and we throw in some mild consideration of rates declining over 2023, buyers will step forward.

Rising net immigration

The migration flows into New Zealand are turning upward faster than any of us were assuming and I note that last week one commentator was predicting a net gain a year from now of about 36,000 people. The latest flow is a net loss of just over 8,000.

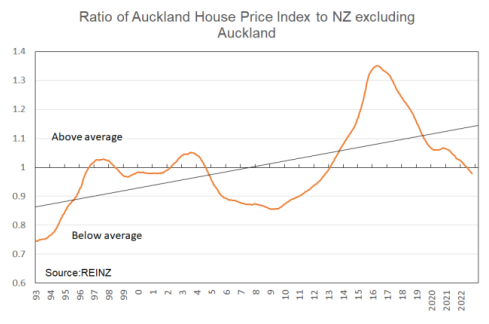

Migrants go where migrants have gone and that means discussions of Auckland’s 1.2% population shrinkage in the past two years will switch over 2023 towards the city being the main beneficiary of the strengthening gross inflow of people. The gross outflow in contrast will be sourced from all over the country.

There is no established tendency for Auckland’s housing market to lead the country. But in a long-term relative pricing sense, the city is actually set to do so in the recovery part of the cycle.

Change in government

Anticipation of the return of National and restoration to property investors of the same legal right accorded to all other businesses – deducting interest expenses from gross incomes for tax purposes – will see investors re-enter the market. They will also move in once they accept interest rates are headed lower.

Conclusion

None of us have models giving accurate predictions of house price movements. The best we can do is try to figure out where the important factors are trending and get a feel for how the psychology of the market is changing.

For the moment that psychology is negative courtesy of the Reserve Bank’s scary words and rate rise two weeks ago. But the negative sentiment will pass, and I would expect the larger investors with good cash reserves built up after selling their crap last year to now be actively looking to capitalise on the pessimism and make some good long-term purchases. For first home buyers this may be their best opportunity in a generation to secure a good home to raise their family in – as long as they can get the finance.

These conditions of good listings, increasingly compliant vendors, and minimal competition from investors will dissipate through 2023.