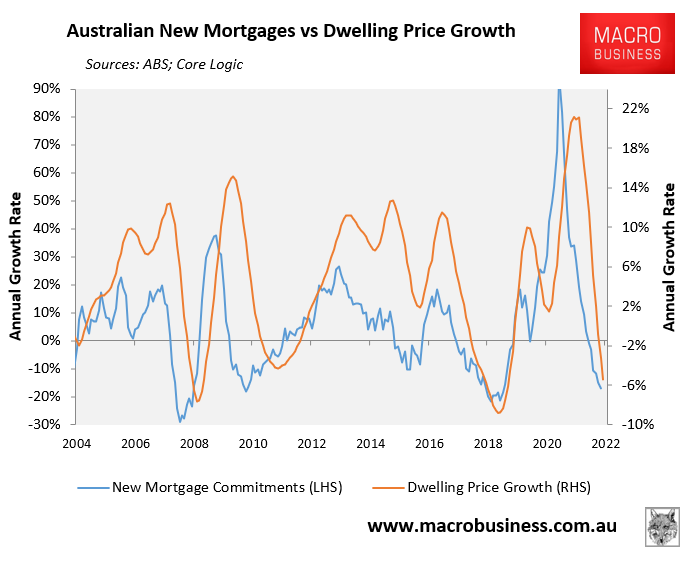

The latest housing lending data from the Australian Bureau of Statistics (ABS) revealed that mortgage demand has collapsed, down 17% year-on-year in October.

As illustrated in the next chart, the ABS’ mortgage lending data has historically been a strong leading indicator for house prices, with new mortgage demand typically leading dwelling prices by around three months:

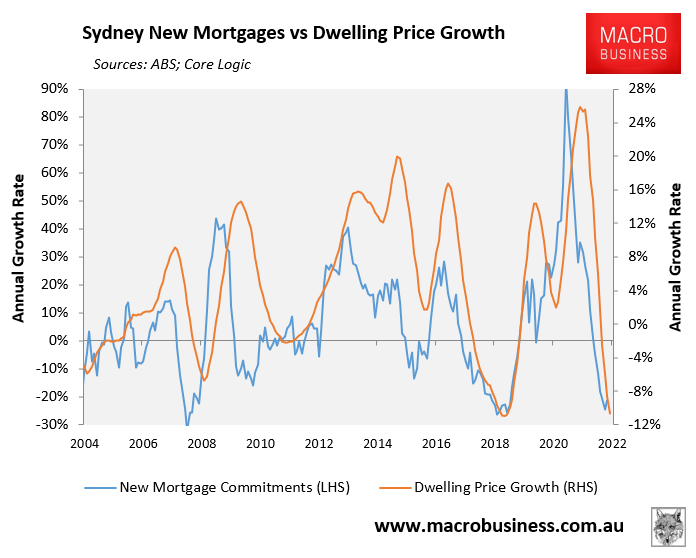

Australia’s housing correction is being driven by the three largest capital city markets, namely Sydney, Melbourne and Brisbane.

The below charts plot the ABS’ mortgage lending growth against dwelling values across each of these markets.

Sydney:

Sydney dwelling values had fallen 11.4% peak-to-trough in November to be leading Australia’s housing correction.

However, the annual decline in new mortgage commitments looks to have bottomed, suggesting the worst may be behind Sydney house prices:

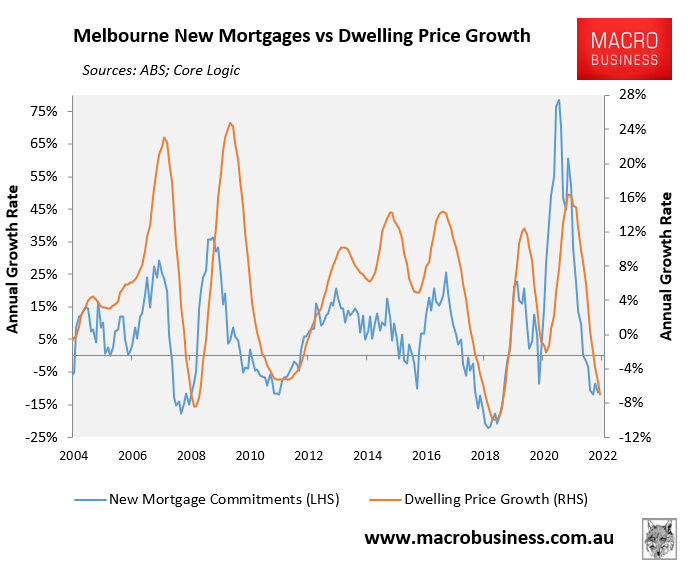

:

: Melbourne:

Melbourne dwelling values had fallen 7.1% peak-to-trough in November. But like Sydney, the rate of decline in new mortgages commitments has bottomed:

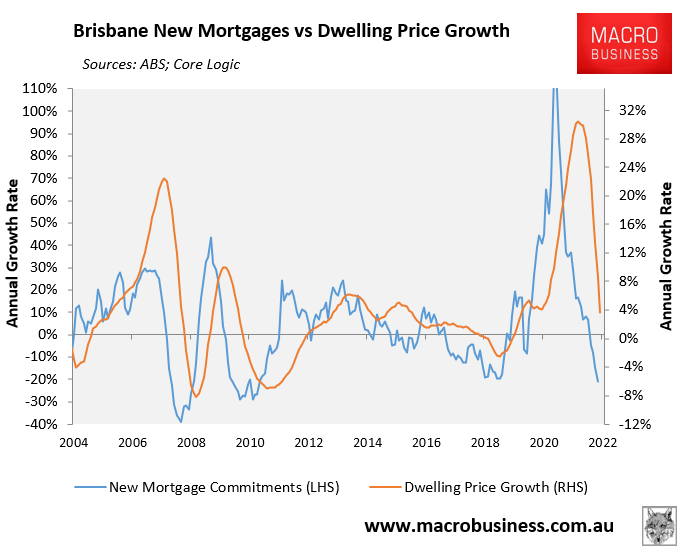

Brisbane:

Brisbane dwelling values had fallen 7.9% peak-to-trough in November. But unlike the other two major capitals, new mortgage growth is still falling:

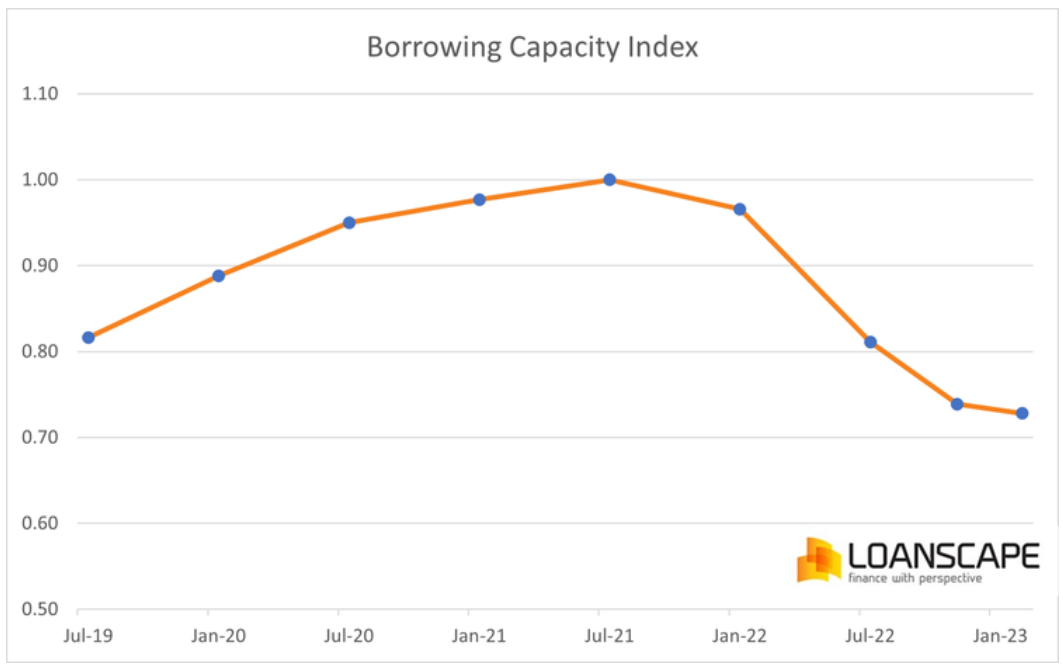

The collapse in mortgage demand and house prices makes sense in light of the Reserve Bank of Australia’s (RBA) aggressive monetary tightening, which had reduced borrow capacity by around 27%, according to Loanscape:

The above chart was before Tuesday’s additional 0.25% rate hike by the RBA, which will reduce borrowing capacity to around 70% of its peak level.

Thus, if a household was permitted to borrow $500,000 at the borrowing capacity peak in October 2021 (i.e. before APRA lifted the mortgage repayment buffer by 0.5%), they will now only be permitted to borrow around $350,000.

Given the above ABS mortgage data is only updated to October 2022, and there has been another 0.5% of tightening since, it is safe to assume that mortgage demand has fallen further, which will place additional downward pressure on house prices.