A relief rally on Wall Street out of nowhere helped lift risk sentiment overnight, snapping back a near week long selloff amid continued pessimism around global growth prospects, as China announced more pledges to underline growth. In currency land, the USD gave back some of its recent gains with Euro and Pound Sterling firming back near their highs while the Australian dollar eventually climbed back above the 67 cent level. US Treasury yields lifted slightly, arresting their weekly decline with the 10 year yield hovering back to the 3.5% level while the commodity complex saw oil prices pullback sharply again, with Brent crude below the $77USD per barrel level while gold is also clawing back its recent losses but is still shy of the $1800USD per ounce level.

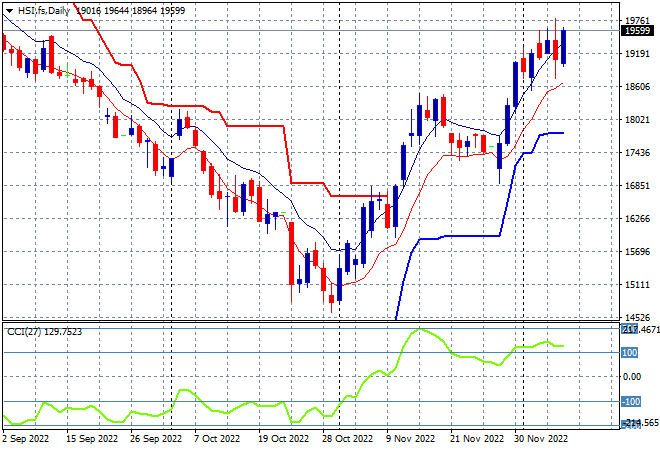

Looking at share markets in Asia from yesterday’s session where mainland Chinese share markets started lower at the open, with a small rally here struggling to convert into a positive finish with the Shanghai Composite moving back below the 3200 point level while the Hang Seng Index soared higher on news the HK government may ease COVID restrictions, lifting more than 3% to 19450 points. The daily chart was showing a perfect breakout here with a big surge up towards the 19000 point level, with futures indicating more upside here to finish the trading week on a solid note, as support is still defended at the 17600 area and daily momentum remains nicely overbought:

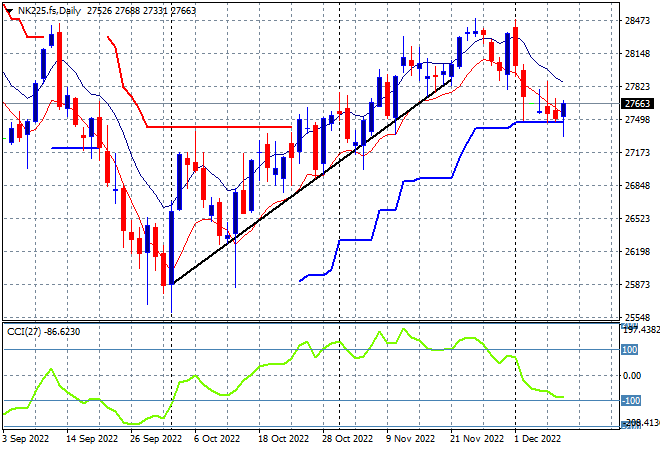

Japanese stock markets remains in sale mode, with the Nikkei 225 finishing 0.4% lower at 27576 points. The lack of a clear lead from Wall Street combined with heavy resistance at the 28400 point level had turned this pause into a rollover into short term support. The daily chart shows this pullback is possibly finished here if ATR support can be defended at the 27500 point level: