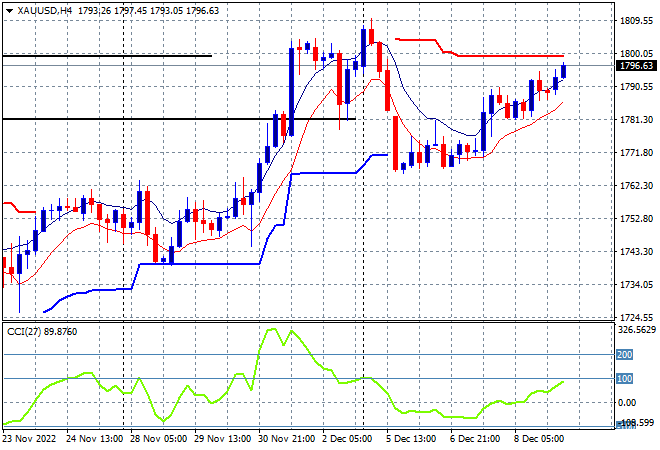

Asian stock markets are all responding positively to the inversion in risk sentiment on Wall Street overnight, putting aside concerns over global recession fears and higher inflation. The USD is pulling back sharply against most of the major currency pairs with the Australian dollar on its way to the 68 cent level. Oil prices are still depressed with Brent crude still slumped below the $76USD per barrel level while gold is working hard to fill in it start of week selloff, now in sight of the $1800USD per ounce level:

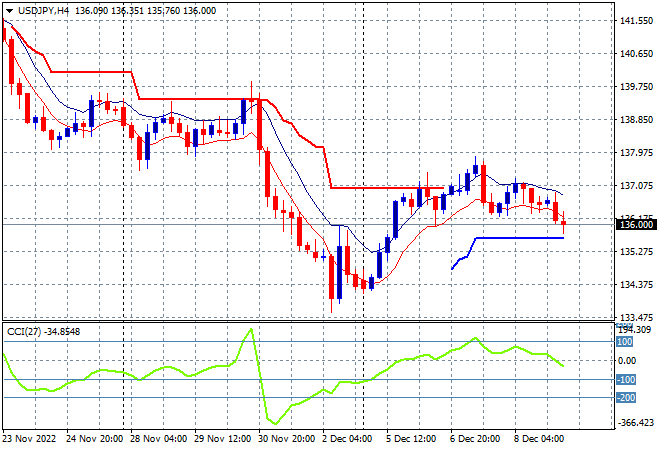

Mainland Chinese share markets are meandering around post the inflation print again struggling to convert into a positive finish with the Shanghai Composite right on the 3200 point level while the Hang Seng Index has lifted again following yesterday’s news that the HK government may ease COVID restrictions, gaining more than 1% to 19769 points. Japanese stock markets are playing catchup finally, with the Nikkei 225 finishing more than 1% higher at 27910 points while the USDJPY pair has been unable to get back above short term resistance at the 137 level , now depressed back down to the 136 handle proper:

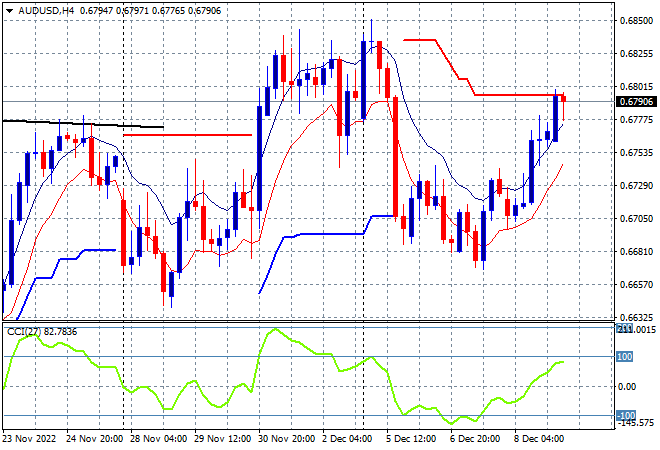

Australian stocks found a strong bid but were still mixed across the sectors as the ASX200 finished nearly 0.5% higher at 7211 points. The Australian dollar was able to claw back its start of week losses, now just below the 68 handle as it looks to take out short term resistance overhead:

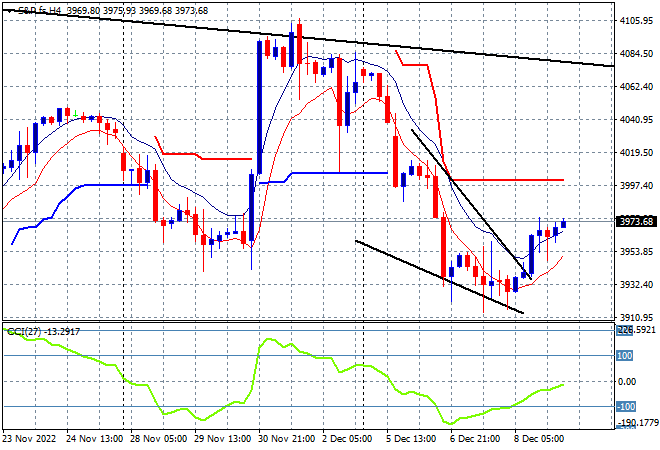

Eurostoxx and US futures have been able to climb higher from their overnight gains as we head into the London open with the S&P500 four hourly chart showing price action still under last week’s low and of course the very important 4000 point level, but looking slightly more promising:

The economic calendar finishes the trading week with US PPI and Michigan consumer sentiment prints.