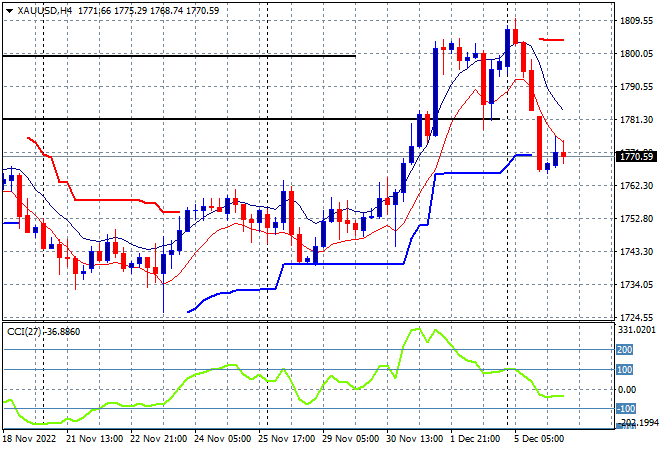

Asian stock markets have had a mixed reaction to the post US PMI selloff from overnight, with the USD still strong against most of the major currency pairs but not enough to scare all but domestic markets. The RBA lifted as expected which put a slight damper on the Australian dollar which was already under pressure more than others from overnight. Oil prices are still depressed and failing to beat overhead resistance with Brent crude hovering just above the $83USD per barrel level while gold is trying to hard to bounce off its recent overnight lows but is struggling here just above the $1770USD per ounce level:

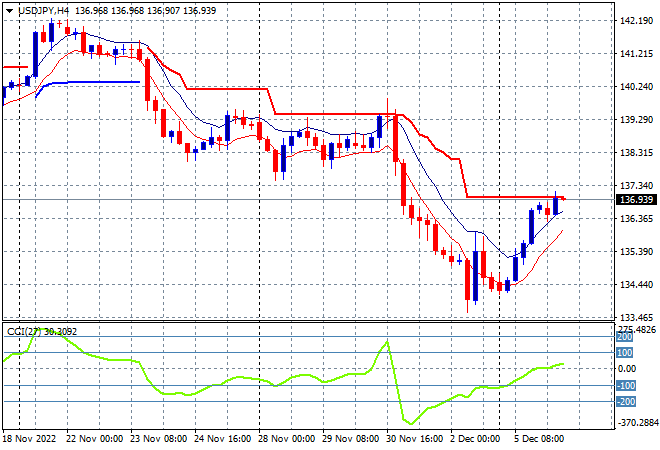

Mainland Chinese share markets started lower at the open but have managed some gains post the long lunch break with the Shanghai Composite above the 3200 point level while the Hang Seng Index has retreated, this time down 1% to 19318 points. Japanese stock markets were able to finally find a bid however it was quite modest with the Nikkei 225 finishing 0.3% higher at 27915 points while the USDJPY pair is still moving higher after its overnight bounceback but is not yet threatening short term resistance at the 137 level:

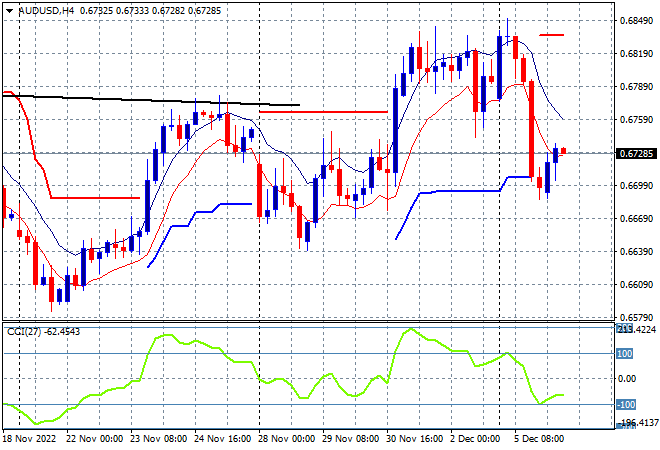

Australian stocks had a down day due to the action on Wall Street overnight and the RBA rate hike with the ASX200 finishing 0.5% lower at 7291 points. The Australian dollar was able to claw back some of last night’s losses before the meeting but hasn’t engaged the next gear higher, still stuck here just above the 67 handle with short term momentum still clearly negative:

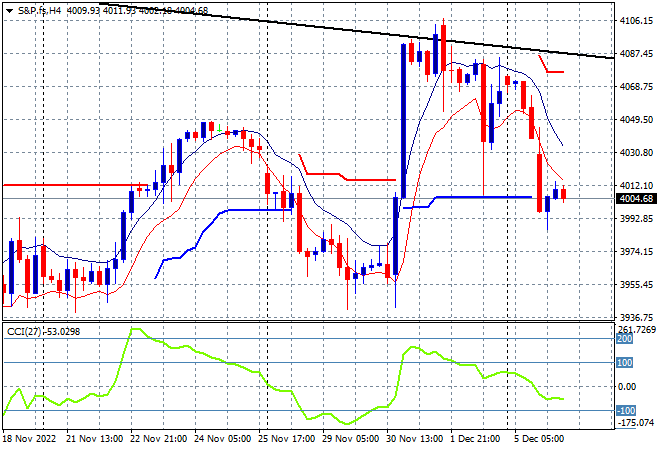

Eurostoxx and US futures are just holding on to last night session lows’ as hesitation builds going into the London open with the S&P500 four hourly chart showing price action still under retreat and wanting to cross below the 4000 point level:

The economic calendar is relatively quiet tonight with US balance of trade figures.