Modelling by BetaShares shows that Australia’s mortgage payments to income ratio has risen to 42.8%, which is its highest level since the September 1990 quarter. This compares with a ratio of just 42.1% at the height of the global financial crisis.

Borrowers were paying double-digit mortgage interest rates in the 1990s, but the median national house price was just 3.1 times the average household income. In contrast, this metric is now 6.2 times the average income.

The mortgage payments to income ratio is much higher than the national average in Sydney (57.8%), reflecting its status as the nation’s most expensive property market. Mortgage affordability in Sydney is also at its lowest level since 1990 (63.9%):

Melbourne’s mortgage payments to income ratio (41.8%) is slightly lower than the national average, but is also at its highest ever level, reflecting its stronger price growth since 1990:

BetaShares chief economist David Bassanese said that “people trying to buy today are facing close to the worst conditions we’ve seen in 30 years”. He also noted that the national mortgage payments to income ratio would likely exceed 1990 level if the Reserve Bank of Australia (RBA) increased interest rates another 1%.

Shane Oliver of AMP Capital also warned that mortgage affordability may become the worst on record if interest rates keep rising.

“You’ve got the worst of both worlds: high house prices relative to incomes and high rates”, Oliver said.

“If interest rates keep going up and go up as much as the money markets are talking about we might end up with the worst mortgage affordability on record.”

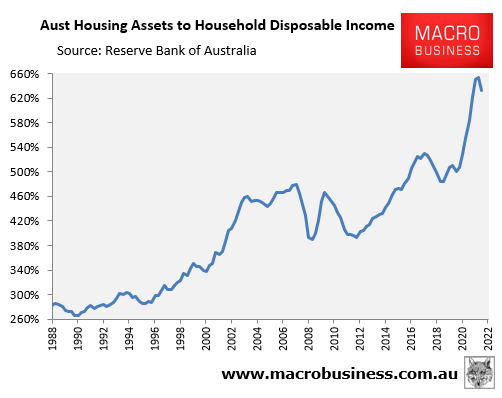

I’d argue that buying and then paying off a home is already harder than in 1990. While initial mortgage repayments are a bit lower, the deposit required is much higher reflecting the doubling of the dwelling price to income ratio:

The above also helps to explain why Australian house prices will continue to fall. In addition to the reduced borrowing capacity, housing is simply unaffordable at current (or higher) interest rates.

Prices will rebound when the RBA starts cutting interest rates.