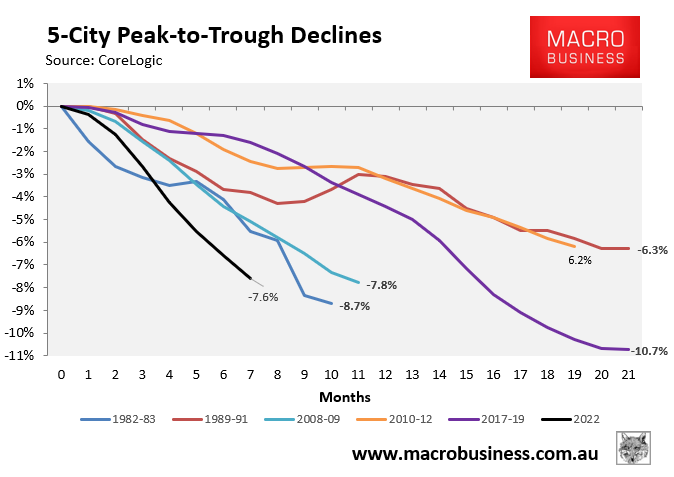

I noted on Friday that Australian house prices were falling at the fastest pace on record, falling 7.6% in only seven months across the five major capital cities:

This countered the emerging narrative from some corners that Australia’s housing correction was nearing a bottom.

Over the weekend, Coolabah Capital’s Chris Joye argued there is “no evidence of a housing market bottom”, with the “harsh reality” that “the pain is set to continue for many more months to come unless the RBA swings 180 degrees and starts cutting interest rates, which nobody expects in the very near-term”.

Joye noted that “the previous record for Aussie house price losses was between 10% per cent and 11% from 2017 to 2019”, which is shown in the above chart. He believes the 2017-19 correction will be surpassed “in about March” next year.

Joye also does not expect a material housing rebound to emerge once the RBA finishes hiking. Rather, “it will really depend on when it cuts rates, and by how much”.

In the absence of rate cuts, a rebound “will be driven by income growth, which tends to be a slowly moving beast”.

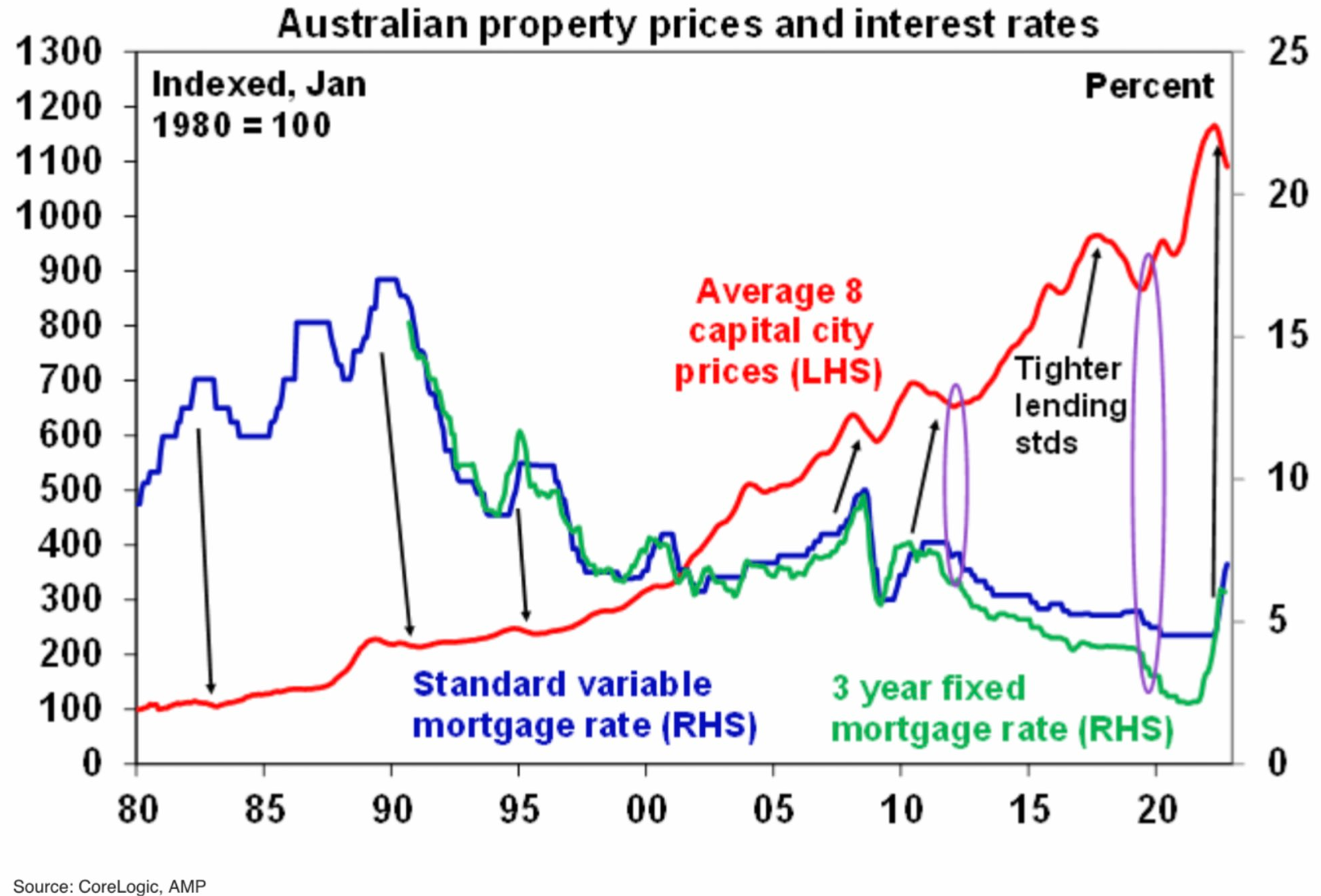

AMP Capital chief economist Shane Oliver last month posted the below chart on Twitter supporting Joye’s view. It shows how the “2012 and 2019 housing upswings did not start until rates fell”:

My best guess is that the RBA will start cutting rates in the second half of 2023 in response to the world entering into recession, Australia’s growth slowing materially, and rising unemployment. At that point, the RBA will have realised that it has gone too far in its monetary tightening and will slash rates to fight off recession.

House prices will then commence the next growth phase, with the strength of the rebound depending on how aggressively the RBA cuts.

In my view, the consensus forecast of a 15% peak-to-trough decline in Aussie house prices is looking about right.