CoreLogic’s Eliza Owen tipped an increase in forced property sales in 2023 once hundreds of billions of dollars worth of fixed rate mortgages roll over from their current cheap emergency low interest rates (circa 2%) to 5% or 6%.

“While the majority of home owners will still be able to service their loans, we could see a bit of additional supply hitting the market as people need to sell. This would presumably put further downward pressure on prices”, Owen said.

Her view was supported by AMP Capital’s chief economist, Shane Oliver.

“I think there’s more pain ahead of us, and until the RBA cuts interest rates, and we’ve seen the worst of the fixed mortgage reset, I think there’s more downside in prices all the way up to the September quarter next year”, Oliver said.

“I think we’re going to see some pick up in distressed sales as a result of ongoing rate rises at a time when a large number of mortgage holders are coming off their record-low fixed loans”.

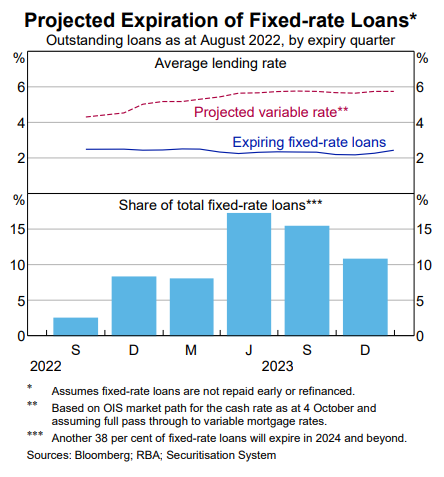

The latest Financial Stability Review (FSR) from the Reserve Bank of Australia (RBA) noted that “around 35% of outstanding housing credit is on fixed-rate terms” and “around two-thirds of these loans are due to expire by the end of 2023” (see next chart).

The RBA estimates that “most fixed-rate borrowers with loans expiring in 2023 will face discrete increases in their interest rates of 3–4 percentage points when they roll over to variable rates”, and that “almost 60% of borrowers with fixed-rate loans would face an increase in their minimum payments of at least 40% when they expire”.

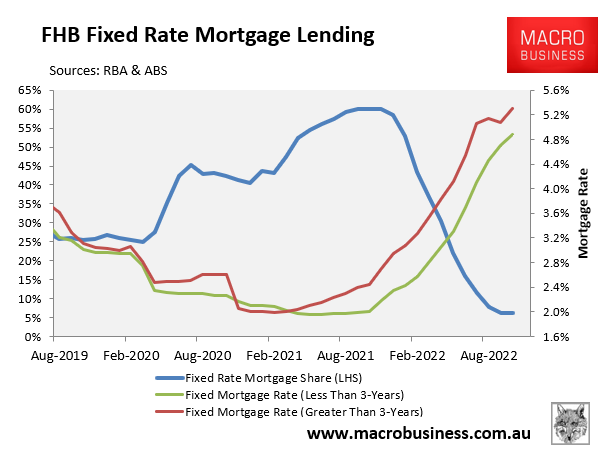

First home buyers (FHB) dominated fixed rate mortgage lending over the pandemic (see next chart) and are most exposed given they “tend to enter the housing market with relatively high initial LVRs” and “have had less time to accumulate excess payments”.

Ultimately, whether distressed sales become a major issue that exerts major downward pressure on house prices will depend on the strength of the labour market.

If unemployment spikes, then many mortgage holders will struggle to meet their repayments, driving up defaults. It’s as simple as that.