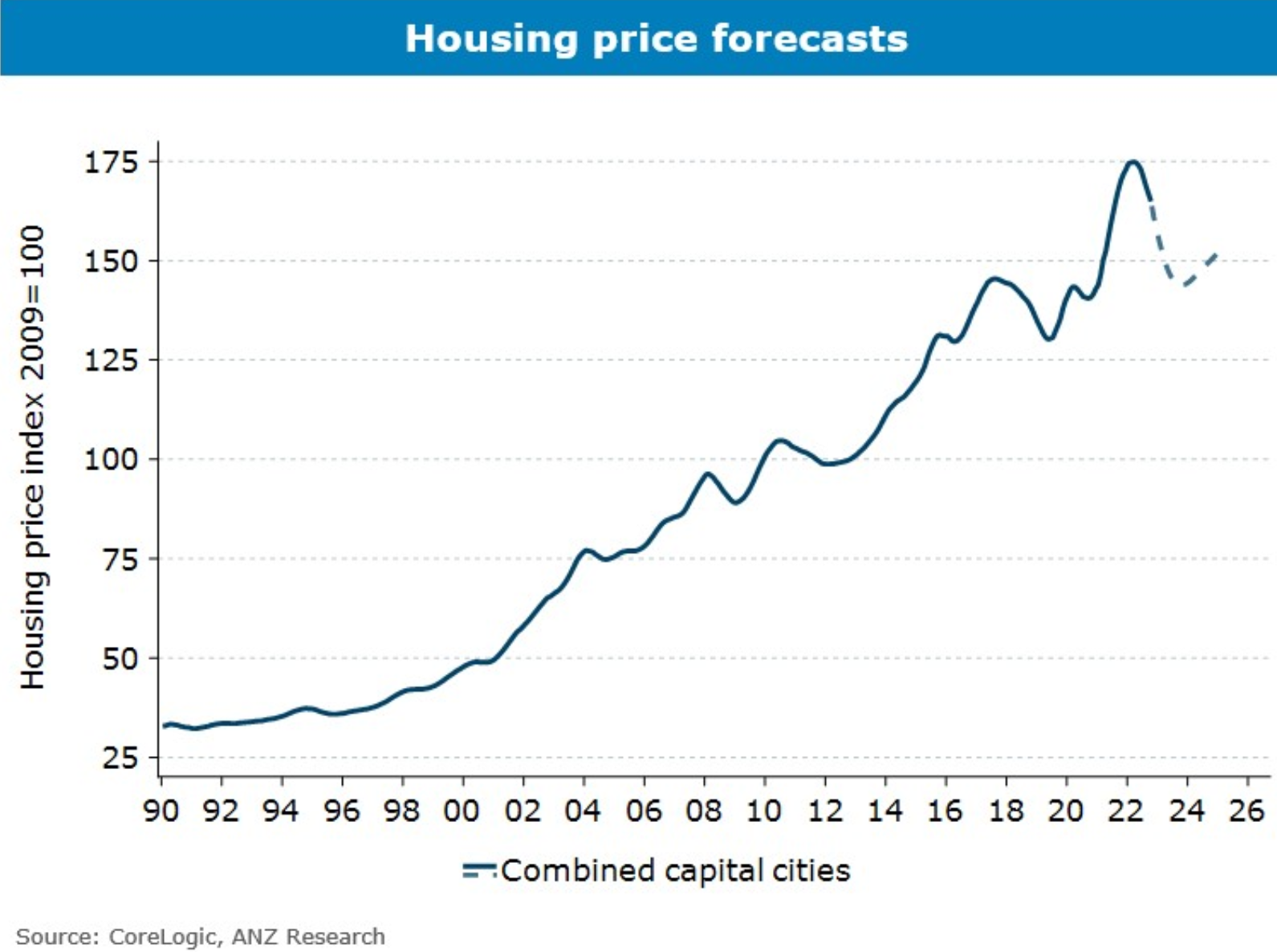

Earlier this week, ANZ Economics updated its Australian house price forecasts, tipping an 18% peak-to-trough decline in values through to the end of 2023:

ANZ: Australian house prices to fall 18%.

Sydney (-20%) and Melbourne (-17%) are tipped by ANZ to lead the declines.

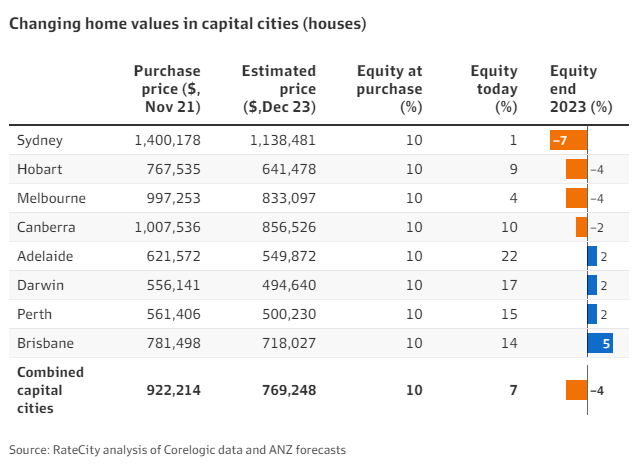

RateCity has estimated the degree to which first home buyers that purchased a median priced home in November 2021 with a 10% deposit would be in negative equity if the ANZ’s price forecasts come to fruition.

A median house buyer in Sydney would be in negative equity by 7% in Sydney by the end of 2023, whereas Hobart (-4%), Melbourne (-4%) and Canberra (-2%) would also be underwater:

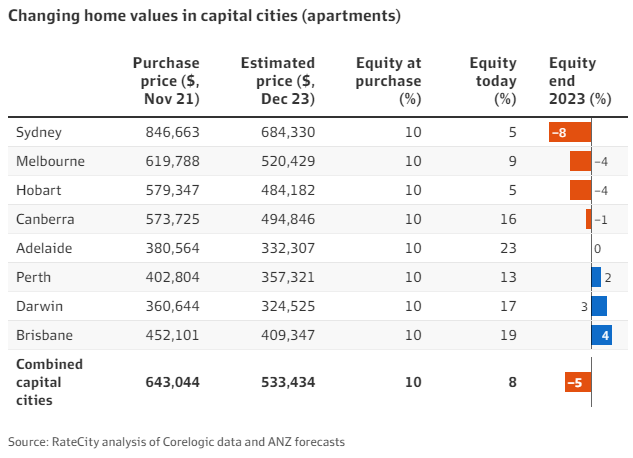

The situation is similar for unit buyers, with the median Sydney first home buyer facing 8% negative equity, and buyers across Melbourne (-4%), Hobart (-4%) and Canberra (-1%) also underwater:

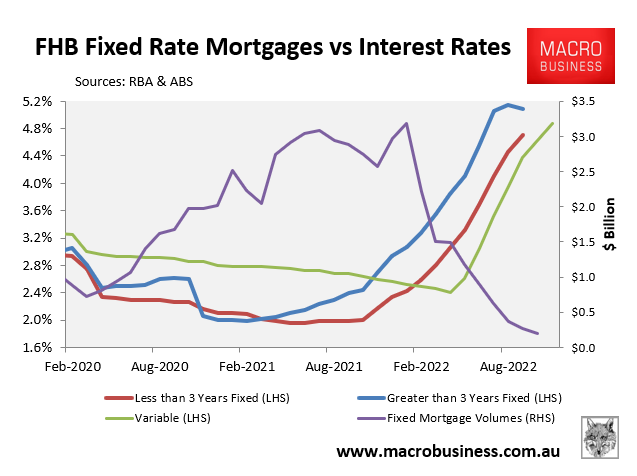

The situation is worst for those first home buyers that borrowed to the max on a cheap fixed rate of around 2%:

First home buyers face fixed rate mortgage time bomb.

The bulk of these fixed mortgages will expire in 2023 and will reset to rates that are at least double what they are currently paying.

Many recent first home buyers will then face a poisonous combination of negative equity and extreme mortgage stress.