NSW has dropped its demand that it be compensated for about $100 million in royalties, which would be lost by a cap on black coal, and instead has convinced the Commonwealth to temporarily subsidise energy bills for households and businesses.

On the eve of Friday’s national cabinet meeting, NSW Liberal Treasurer Matt Kean, who engineered the deal that will aid his government in the run-up to the March 25 state election, said, “we are close to landing a deal”.

But Queensland, which was holding firm that it be fully compensated by Canberra for any dividend or royalty losses from the $125 cap on coal and the $13 cap on gas, was “way off” a deal, sources said.

Other less toilet paper media is reporting QLD is almost there as well.

The rebates will be channeled through energy bills so will not be inflationary.

Advertisement

Electricity futures did not ease any more yesterday but pre-Ukraine War prices well below $100MW/h should transpire in due course:

The deal is decent to the extent that it will avert the energy disaster that was bearing down on the country with 800% rises in utility bills.

Advertisement

But is it a good deal? Not really. The price caps for coal and gas are very high. Nor will it capture any of the windfall profits.

That’s a cowardly effort by the Albanese Government. Bruce Robertson of the Institute for Energy Economics and Financial Analysis has more:

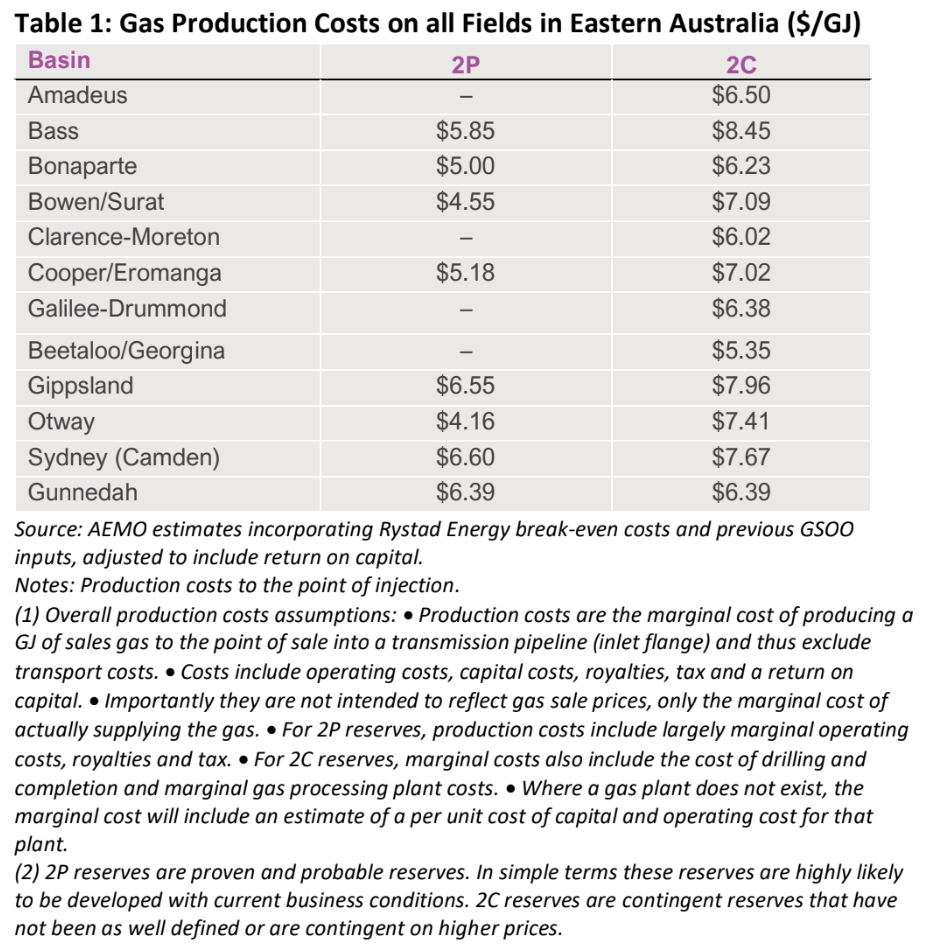

$12 Per Gigajoule Is Too High

There has been much discussion about the need for a domestic gas reservation for Australia’s east coast market, or a price cap, and prices have been widely bandied about by government, industry and commentators.

There has been little analysis done on what constitutes a fair domestic gas price for both producers and consumers. Western Australia’s domestic gas reservation policy, in operation since 2006, has delivered gas at prices in the $5-7/Gigajoule (GJ) range.

This briefing paper seeks to dimension what a fair price is and comes to the conclusion that a price cap of $7/GJ allows for substantial profits over and above a return on investment for the majority of gas produced on the east coast of Australia.

A price cap of $7/GJ would see all producing fields make a return on equity and a profit on top.

This paper also makes the case for a domestic gas reservation on the east coast of Australia for the following reasons:

The gas industry’s profitability is determined by export sales, not domestic prices, as over 70% of gas produced on the east coast of Australia is exported.

Eastern Australia is swimming in gas. There is not, nor has there ever been, a shortage of gas on the east coast of Australia.

The developed proven and probable reserves — that is, those that the gas industry could utilise in the short term — are equivalent to 8.4 years of production at the current record production rates of 2021. There is no shortage of gas, just a shortage of desire to supply it at a reasonable price.

All state governments in Australia, and the federal government, have Net Zero commitments by 2050 yet there is widespread government support for unnecessary new gas fields. The development of new gas fields is entirely inconsistent with any net zero ambition. There appears to be unwarranted exceptionalism for gas.

The Australian Competition and Consumer Commission has forensically described how the gas market on the east coast is controlled by a ‘cartel’, that controls production and fixes prices, in its never-ending gas price enquiry in operation since 2015. It unfortunately refuses to label the cartel correctly. Incorrect labelling leads to the mirage that a market for gas exists on the east coast of Australia. A market simply does not exist.

A proposed $12/GJ price for gas gifts the gas cartel super profits for the majority of their production to the detriment of Australian energy consumers.

If the government caps prices at the high price of $12/GJ, with little or no evidence for so doing, it risks continuing deindustrialisation in Australia with the unintended consequence of higher global emissions of greenhouse gases.

Advertisement

The massive dividends will continue to flow out as well, wrecking the current account.

But at least you will no longer be made massively poorer by your energy exports. And manufacturing will probably be OK given most of the rest of the world is paying more.

In the context of Australia’s vile Game of Mates, that’s a glowing outcome.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.