Goldman has a crack at it.

- China reopening in focus: A slew of headlines put China reopening front and center and have buoyed Chinese asset markets. In this note, we summarize our reading of recent developments, obtain relevant parameters based on HongKong and Taiwan’s reopening experience in thinking about the potential policy and mobility path forward for China, and construct four scenarios using these parameters.

- Three readings from recent events: Although there have been quite a few local changes to Covid policies lately, we do not interpret them as China abandoning zero-Covid policy (ZCP) just yet. Rather, we see them as clear evidence of the Chinese government preparing for an exit, and trying to minimize the economic and social cost of Covid control in the meantime. The preparations may last a few months and there are likely to be challenges along the way.

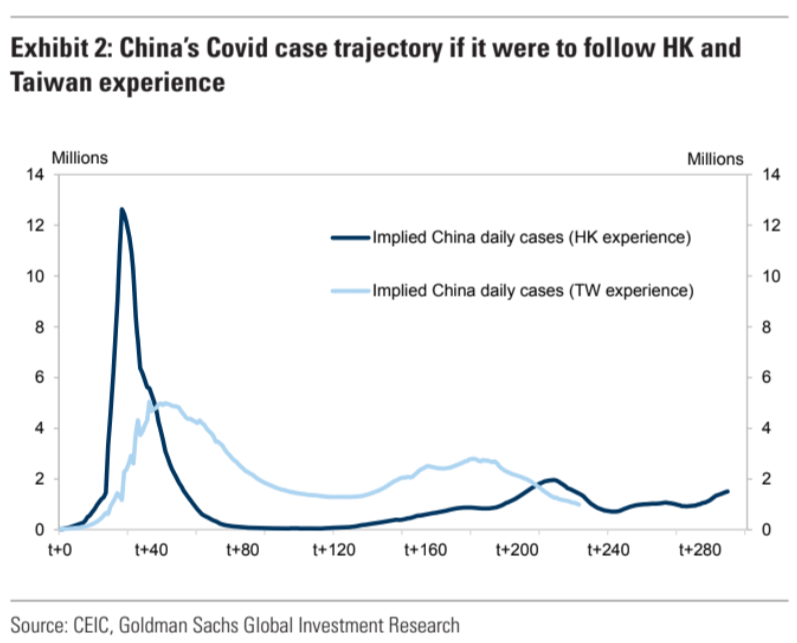

- Three lessons from Hong Kong and Taiwan experience: With most of the population uninfected before reopening, lower elderly vaccination rates than many other economies, and cultural similarities, we think Hong Kong and Taiwan’s reopenings are most relevant for Mainland China. Their experience ssuggest that cases are likely to skyrocket upon reopening and linger for a while, a high elderly vaccination rate is key to a safe reopening, and mobility declines sharply as cases rise.

- Four scenarios of China reopening: We construct scenarios along two dimensions: timing (immediate or delayed reopening) and style (whether managed/prolonged). Our base case remains ZCP stays in the near term followed by an April reopening. This scenario allows time for medical preparations which help improve health outcome significantly with only moderate incremental economic costs next year (0.3pp lower 2023 GDPgrowth).

In “effective reopening with little control” (Scenario 1) we would see immediate reopening with little policy restrictions despite rapidly rising Covid cases. In this scenario we could see the most rapid decline of the Covid control policy index, but the largest hit to mobility at the initial stage of reopening because with little policy control, case numbers would spike, and the health care system might also be under severe pressures. Mobility could rebound sharply after the initial stage of infections. As a result, 2023 full year GDP growth under this scenario would be higher than our baseline (ZCP for the short term) by 1.1pp, while 2024 full year GDP growth would be lower than our baseline commensurately (since more of the recovery/reopening would already have taken place in 2023).