By Gareth Aird, head of Australian economics at CBA:

Key Points:

- We expect the RBA to raise the cash rate at the December Board meeting by 25bp to 3.10%.

- The risks sits with no change, but we consider that risk to be low (~20%).

- We expect a shift in forward guidance that would see the RBA retain a tightening bias but also pave the way for a potential pause in the tightening cycle in February 2023.

- Specifically, we anticipate the Governor will soften the line from the November Statement that “the Board expects to increase interest rates further over the period ahead”.

- We think the key forward guidance statement will be changed to “the Board is likely to increase interest rates further over the period ahead” or “the Board is willing to increase interest rates further over the period ahead”.

Another 25bp hike in December, but forward guidance to shift

The coming week is another big one for Australian financial market participants. There is the RBA December Board meeting on Tuesday. And a stack of domestic data will also be published, which includes the September quarter 2022 national accounts on Wednesday.

The RBA’s rhetoric continues to evolve and the notion of pausing in the tightening cycle has now appeared in every piece of RBA communication since the Governor’s remarks at the Reserve Bank Board dinner on 1 November.

This communication comprises the Board dinner, the November Statement on Monetary Policy, Deputy Governor Michele Bullock’s 9 November appearance at the Australian Business Economists dinner (Q&A session), her appearance before the Senate Economics Legislation Committee (Budget Estimates) the following day, the November Board Minutes and Governor Lowe’s speech at the annual CEDA dinner.

At the September, October and November Board meetings the case was debated to either raise the cash rate by 25bp or 50bp (recall the RBA increased the cash rate by 50bp in September and 25bp at both the October and November Board meetings). We expect that at the December Board meeting the discussion will be between raising the cash rate by 25bp or leaving policy on hold. We do not anticipate that the Board will discuss the case to raise the cash rate by 50bp.

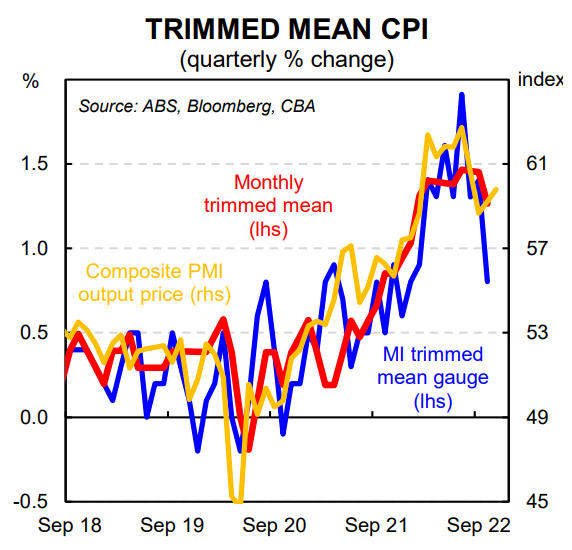

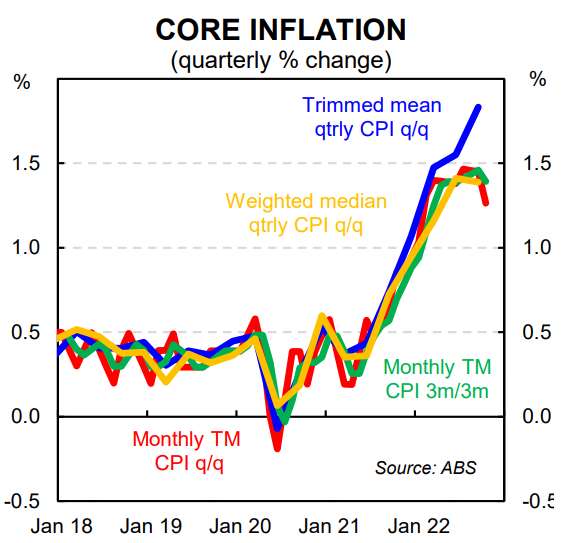

Since the November Board meeting the economic data has been mixed. Key lagging data on wages and consumer prices were firm. That said, the monthly CPI indicator surprised to the downside in October on both the headline and core measure. Labour market data was strong and the unemployment rate sat at a very low 3.4% in October.

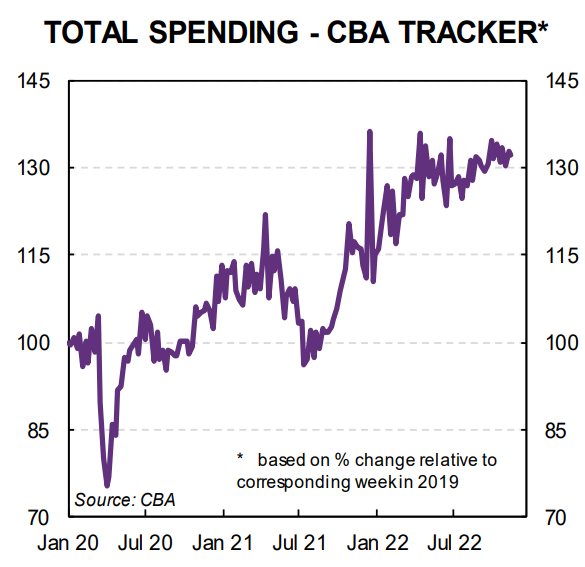

Working the other way was a 0.2% contraction in retail trade over October, another large decline in home prices in November and further falls in business and consumer confidence over October and November respectively. In addition the ‘flash’ composite PMI pointed to a contraction in the private economy over November.

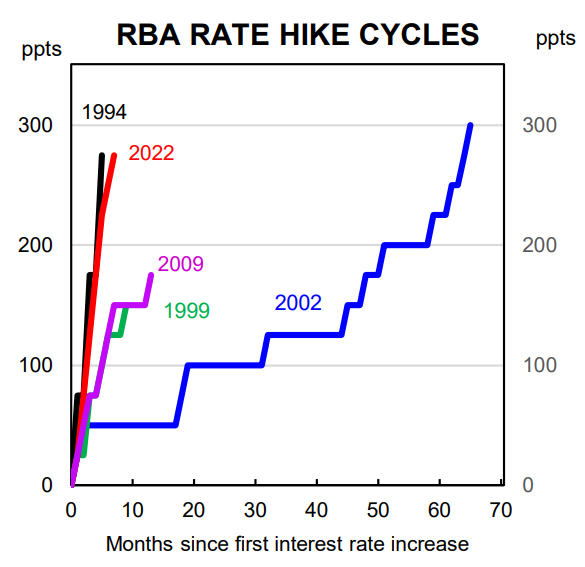

There is a strong case to leave the cash rate on hold in December given the RBA has already delivered an incredible 275bp of tightening over just seven meetings (six months). It takes time for this tightening to impact the demand for goods and services and by extension prices. A further 25bp hike in December would mean an unprecedented 300bp of rate hikes over just seven months.

The RBA is still flying blind to a degree given the last few rate hikes have not yet hit home borrowers from a cash flow perspective (at CBA there is on average a three-month lag between RBA rate hikes and when a borrower on a minimum mortgage repayment schedule experiences an increase in their mortgage payment). There is also a very big expiry of fixed rate home loans over the next year which means monetary policy is operating with a greater than usual lag.

That said, we don’t expect the RBA to leave the cash rate on hold in December. The explicit forward guidance from recent communication that, “the Board expects to increase interest rates further over the period ahead” means another 25bp rate hike is the most probable outcome at the meeting next week (we assign an 80% probability to a 25bp rate hike).

We do, however, expect a shift in the RBA’s forward guidance. Such a change would be in the final paragraph of the Governor’s Statement accompanying the decision.

The final paragraph in the Governor’s Statement accompanying the November Board decision read:

“The Board has increased interest rates materially since May. This has been necessary to establish a more sustainable balance of demand and supply in the Australian economy to help return inflation to target. The Board expects to increase interest rates further over the period ahead. It is closely monitoring the global economy, household spending and wage and price-setting behaviour. The size and timing of future interest rate increases will continue to be determined by the incoming data and the Board’s assessment of the outlook for inflation and the labour market. The Board remains resolute in its determination to return inflation to target and will do what is necessary to achieve that.” (our emphasis in bold).

We think the third sentence above in bold is likely to be softened to “the Board is likely to increase interest rates further over the period ahead” or “the Board is willing to increase interest rates further over the period ahead”.

Replacing the word “expects” with “is likely” dials down the expectation a touch for further rate rises in 2023. Substituting the word “expects” with “is willing” is a more significant downward shift in rate hike expectations.

Both changes would still see the RBA retain a tightening bias. But they would indicate that further policy tightening in 2023 is not locked in. And they would set the RBA up for a potential pause in the tightening cycle in February 2023 while also giving them full flexibility to raise the cash rate again, should they wish to do that.

If such a change is not made in the Governor’s Statement accompanying the Board decision it increases the risk that the RBA also increases the cash rate by a further 25bp in early 2023 to 3.35% (on the proviso that they hike the cash rate by 25bp at the December Board meeting).

The CBA central scenario has the terminal cash rate at 3.10% and our risk case is a peak in the cash rate of 3.35%. Our RBA call will be under review if the Governor makes no changes to forward guidance at the December Board meeting.