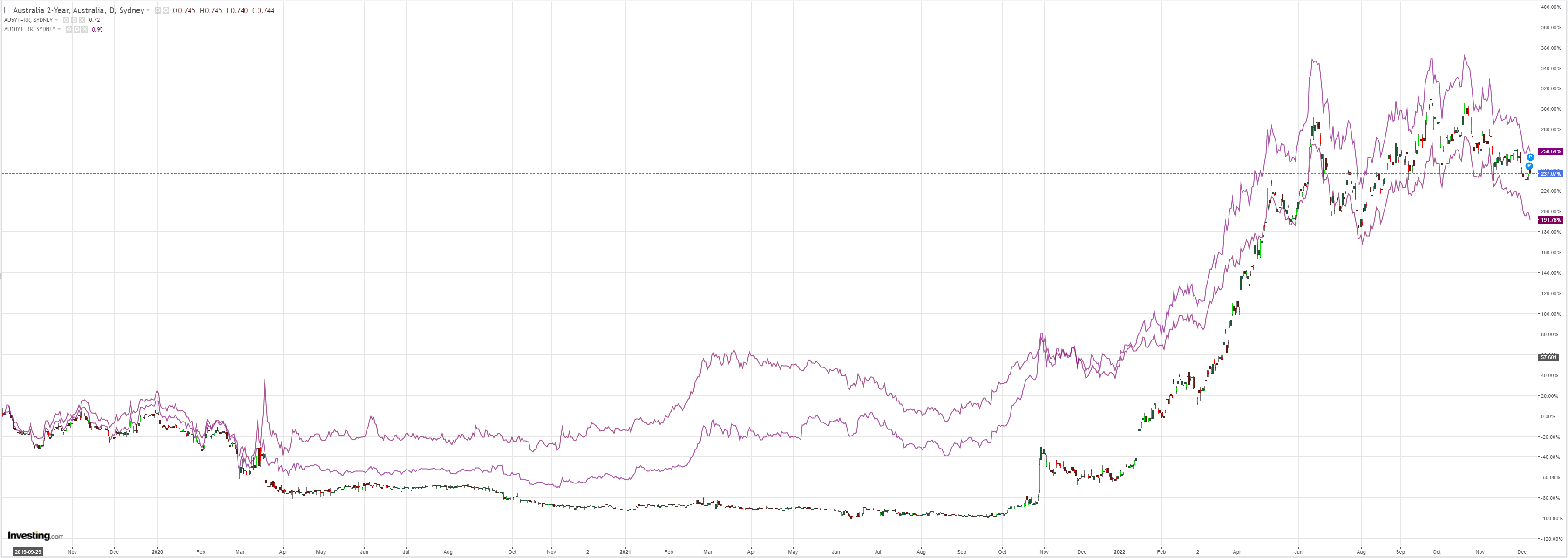

The Aussie curve smash is gaining momentum. All yields fell overnight:

The 1/3 year curve is now decisively inverted indicating rising recession risk. Further out the curve, the flattening is going under a steamroller:

Advertisement

I expect the entire Aussie curve to invert in due course. The RBA has overcooked it.

TD Securities has more:

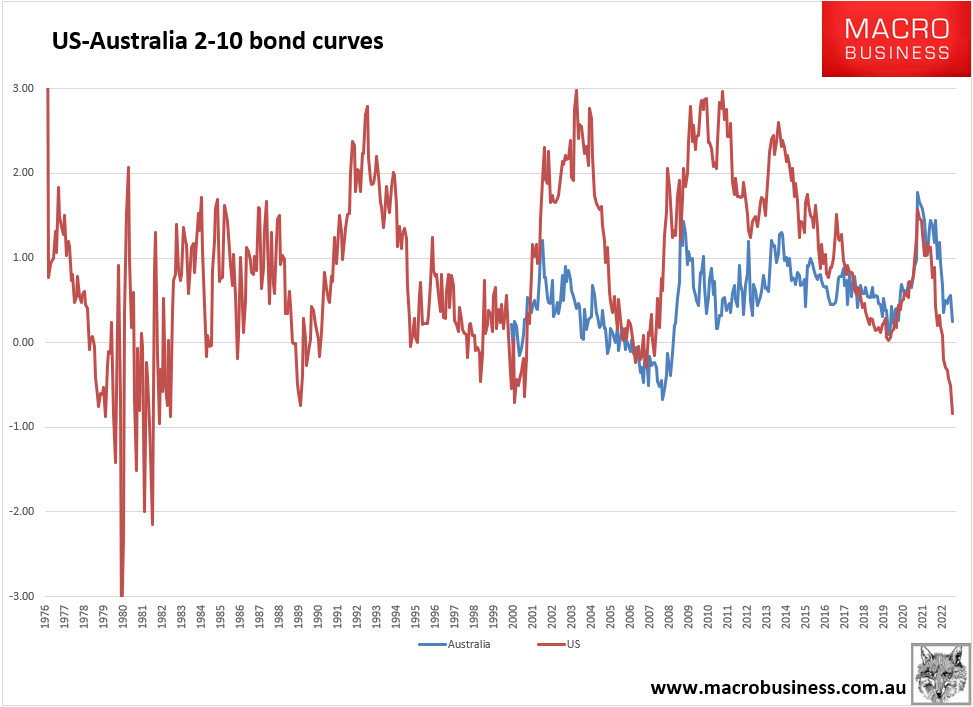

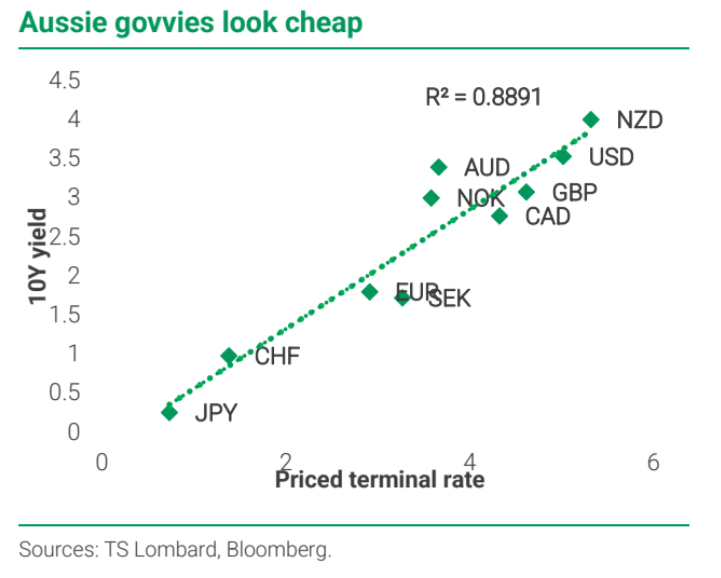

We buy Aussie govvies. The past year has seen very high correlations across regional rates marketsas central banks throughout DM have tightened in synchronization. But heading towards 2023, central banks have started to chart different courses. Australia is one of the most vulnerable economies to rising interest rates and the RBA has slowed the pace of tightening correspondingly. While we expect further tightening from the bank, the end of the tightening cycle is now in sight. Moreover, the market is pricing in a terminal rate of 3.65% in 2H23, but with the global economy heading towards recession in 2023, a lot could wrong before then–in the case of Australia, a notable stumbling block is a bumpy China reopening. Finally, the Aussie 10y already looks too high for the priced-in terminal rate (see chart below left):

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.