Australia’s “unprecedented” mortgage shock

Below is an edited extract of the ‘Your Next Mortgage Move’ Report published by Aussie Home Loans and CoreLogic:

Australia’s mortgage market is moving through unprecedented change. With rates rising rapidly, record levels of household debt and the cost of living on the rise.

Before the pandemic, the cash rate target had averaged 2.55% for the previous decade. The ultra-low cash rate target was a part of a set of policy measures to get more credit flowing through the economy. By signalling an extended period of rock-bottom rates, lenders were confident in substantially dropping the price of fixed mortgages.

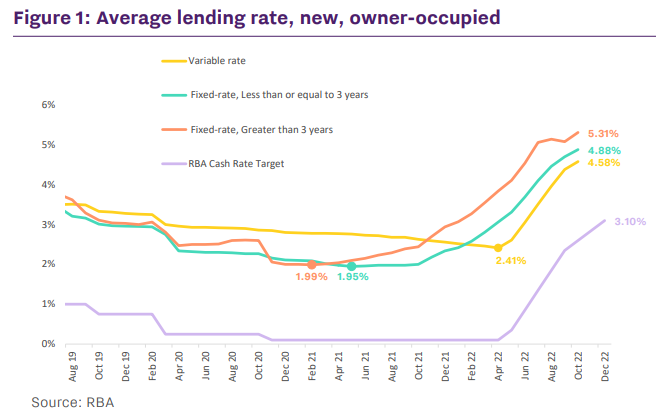

Figure 1 shows average new mortgage rates by type for owner-occupier home loans. As the cash rate hit a record low, the price of fixed mortgages soon followed. In May 2021, average fixed mortgage rates with a set rate of three years or less dipped to a low of 1.95%.

Fixed rates where the set term was greater than three years dipped as low as 1.99% in February 2021. Average variable rates bottomed out at 2.41% in April of 2022, in line with the last month of the record-low cash rate setting.

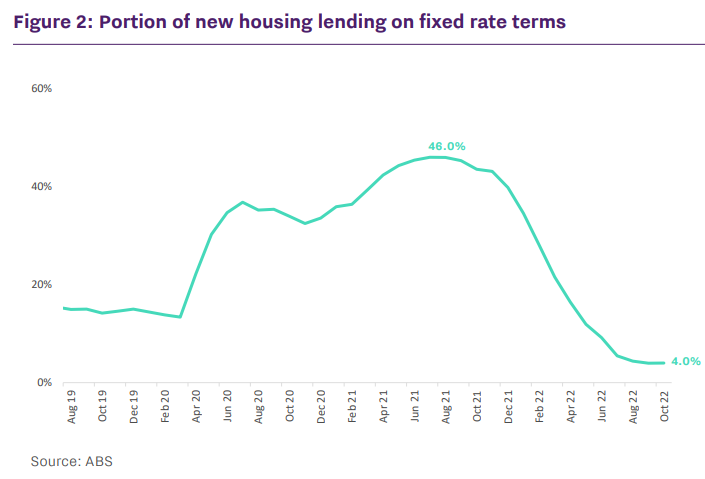

Interest rate data from the RBA suggests it is unusual for fixed rates to be low relative to variable rates. Around 20% of housing lending has been on fixed rates as a result.

But cheap rates through the pandemic created a rare period in which fixedrate borrowing ballooned, with total housing lending and refinancing on set interest rates peaking at 46% in July 2021.

This has led to the total outstanding value of housing credit in Australia sitting at around 35%, up from less than 20% at the onset of the pandemic, according to the RBA.

According to the latest Financial Stability Review from the RBA, around two-thirds of fixed-rate mortgages are set to expire through 2023.

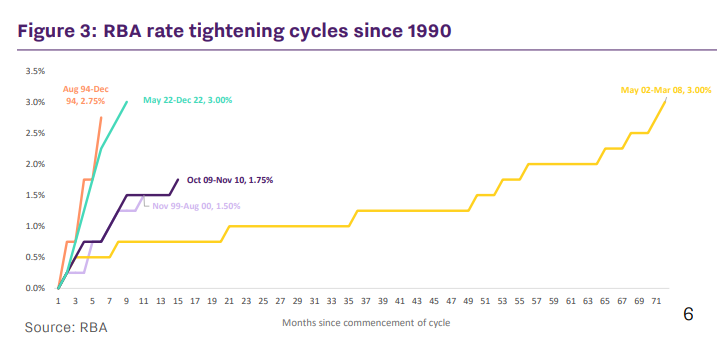

On December 6th, the RBA increased the cash rate by another 25 basis points (to 3.1%), taking the cash rate 300 basis points higher in eight months, which is highly unusual. In fact, it marks the steepest increase in the cost of debt since the 1990s, when the RBA first started setting the cash rate (Figure 3).

Assuming full cash rate rises are being passed on to mortgage rates, this would put the average new variable mortgage rate for owner occupiers at around 5.08% through December. The RBA has also estimated that fixed rate borrowers with expiring terms in 2023 will see rate increases of around 3-4 percentage points.

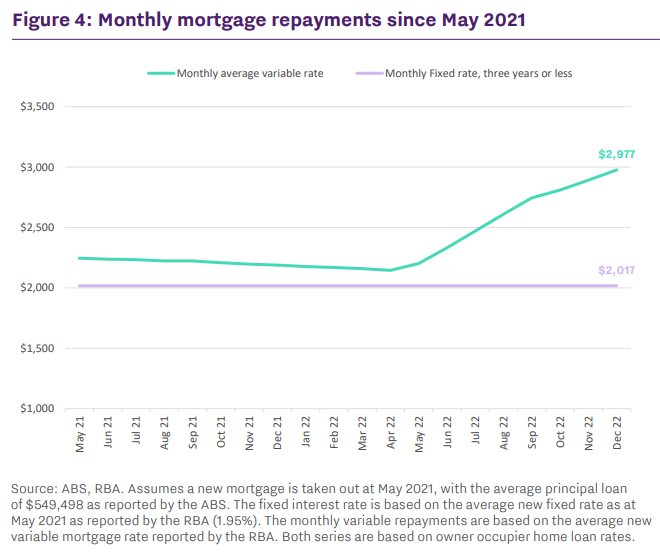

Figure 4 shows what monthly repayments look like for fixed-term borrowers versus variable-rate borrowers since May, assuming the national average home loan size over that month (which was $549,498 according to the ABS).

For those who purchased in 2021, being exposed to variable home loan rates has likely meant a big increase in repayments. In the example above, monthly home loan repayments on variable rates are estimated to be around $960 higher than at the fixed rate level.

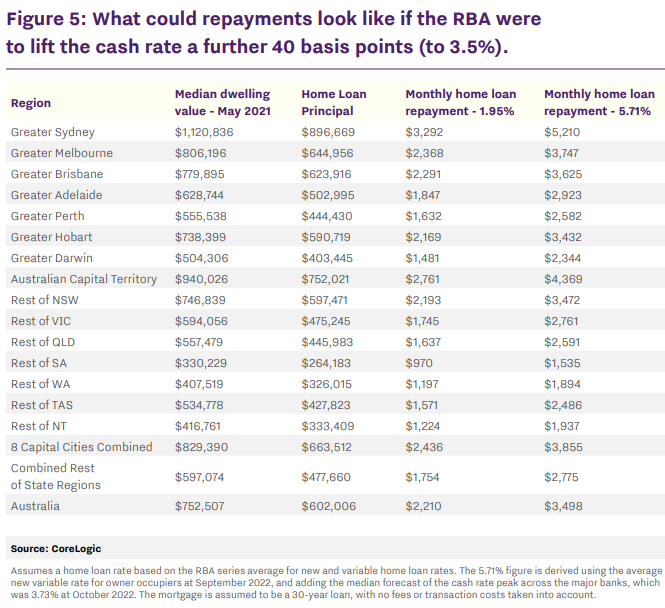

If the cash rate were to rise a further 40 basis points (to 3.5%), the RBA estimates that around 60% of fixed-rate borrowers with terms expiring in 2023 would have increases in their minimum repayments of at least 40%.

The table below shows a breakdown of how mortgage repayments could rise over time by region. For those who purchased at the lowest point of average fixed rates where the fixed term was 3 years or less (May 2021), we take the median dwelling value and assume a purchase with a 20% deposit. The table shows the difference between a low fixed rate repayment of 1.95%, versus the payment on an average new variable home loan rate (which we assume may reach 5.71% by mid-2023).

These extremes of lows and highs in mortgage rates show how dramatically home loan repayments could be subject to change in the next 6 months. The scenario in table 5 shows a 58.3% uplift in mortgage repayments across the capital cities and regions of Australia, ranging from a monthly repayment lift of $565 in regional South Australia to an increase in monthly repayments of around $1,918 in Sydney.