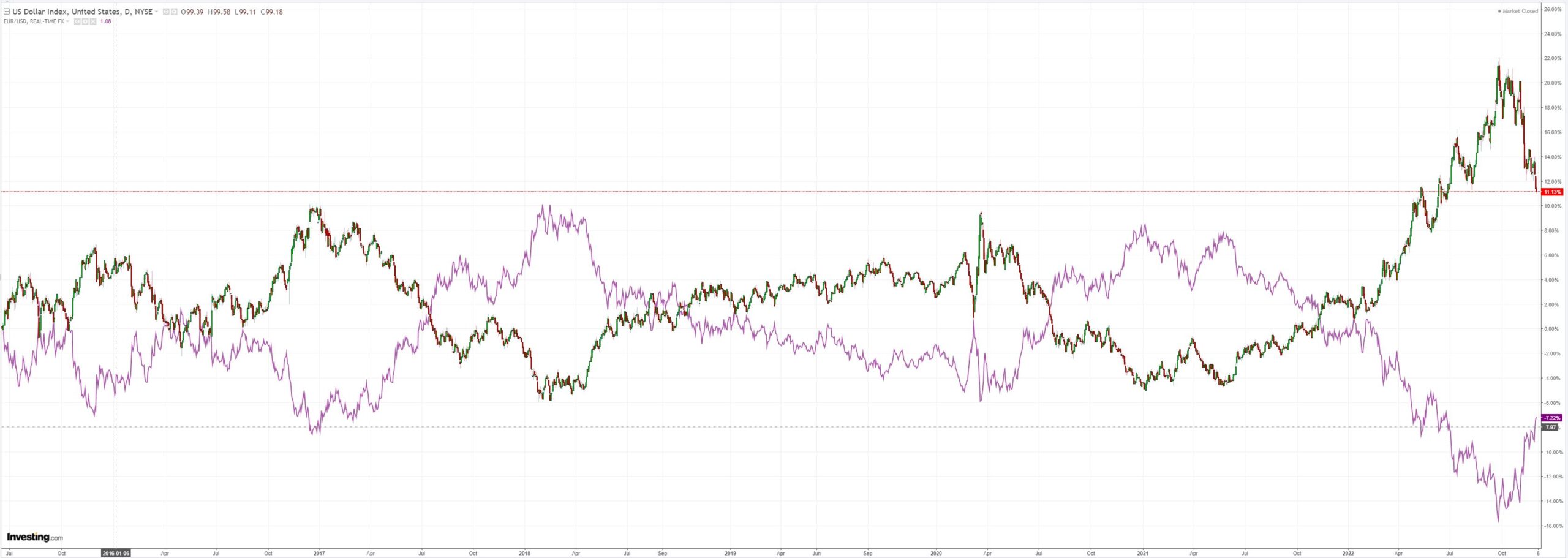

DXY kept falling Friday night and has described an almighty head and shoulders double top:

AUD held the gain. It’s now being smashed on the crosses as yesteryear’s DM laggards roar:

Advertisement

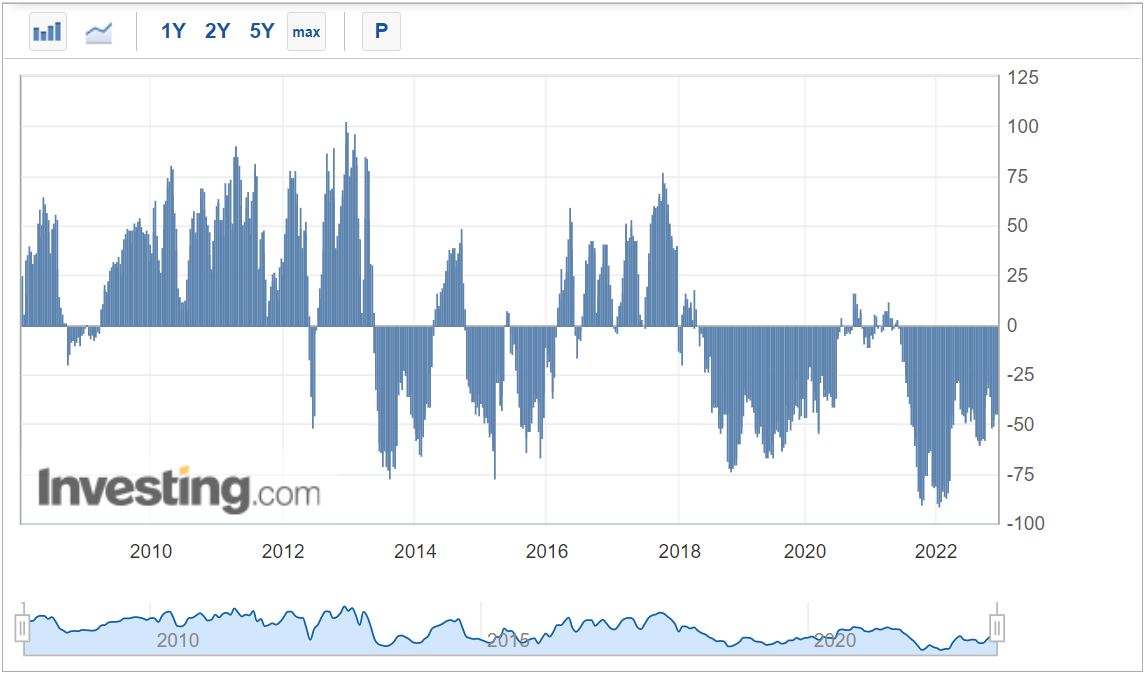

Specs are still moderately short the battler:

Oil and gold marked time:

Base metals were bid:

Advertisement

Big miners march on:

EM stocks not so lucky:

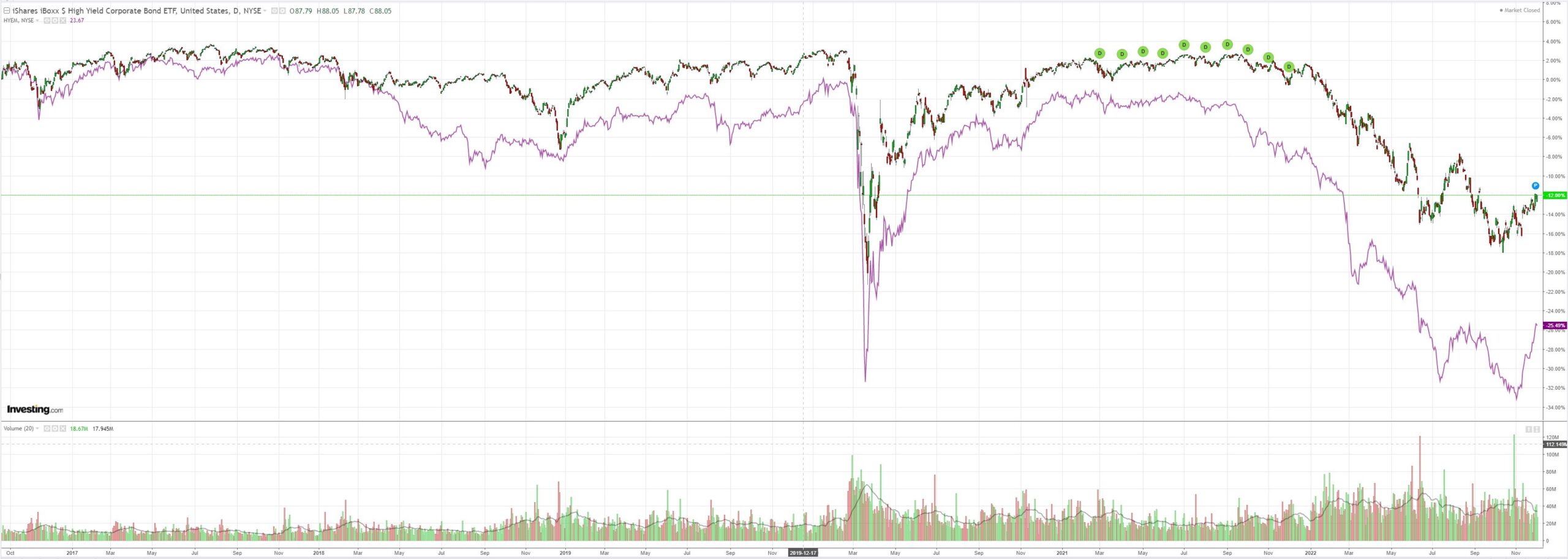

As the junk rocket sputtered:

Advertisement

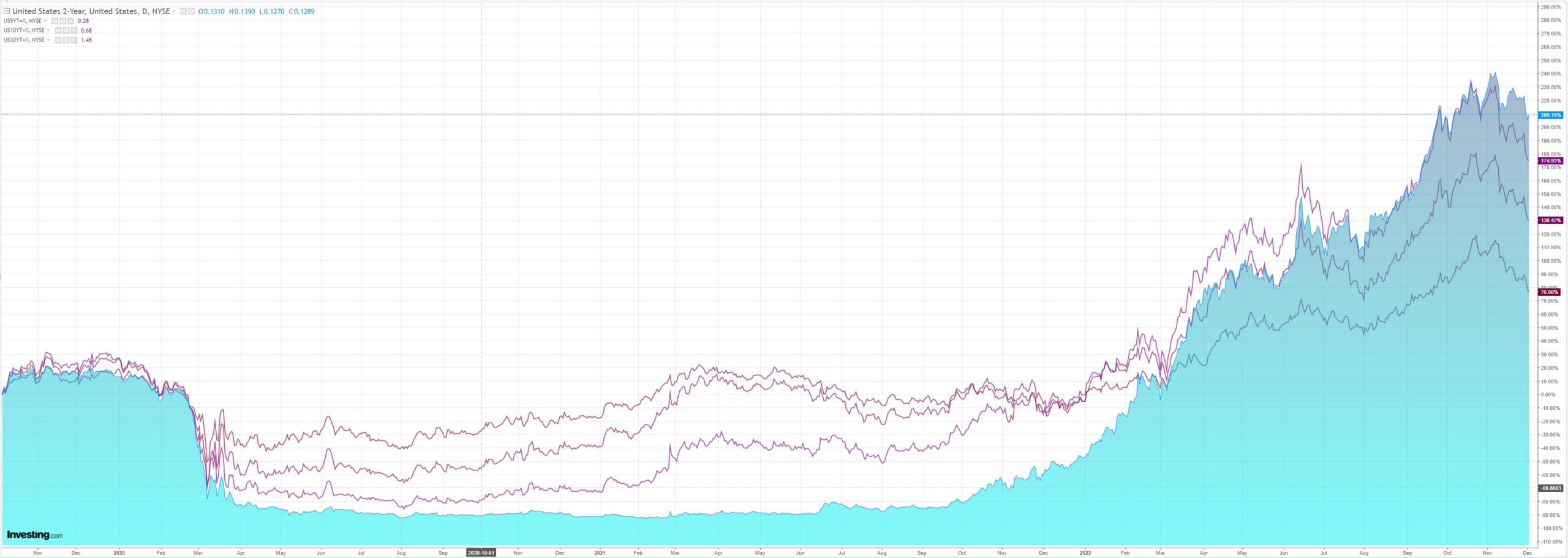

Some kind of psychopath is brutally murdering the treasury curve:

Stocks were flat:

Advertisement

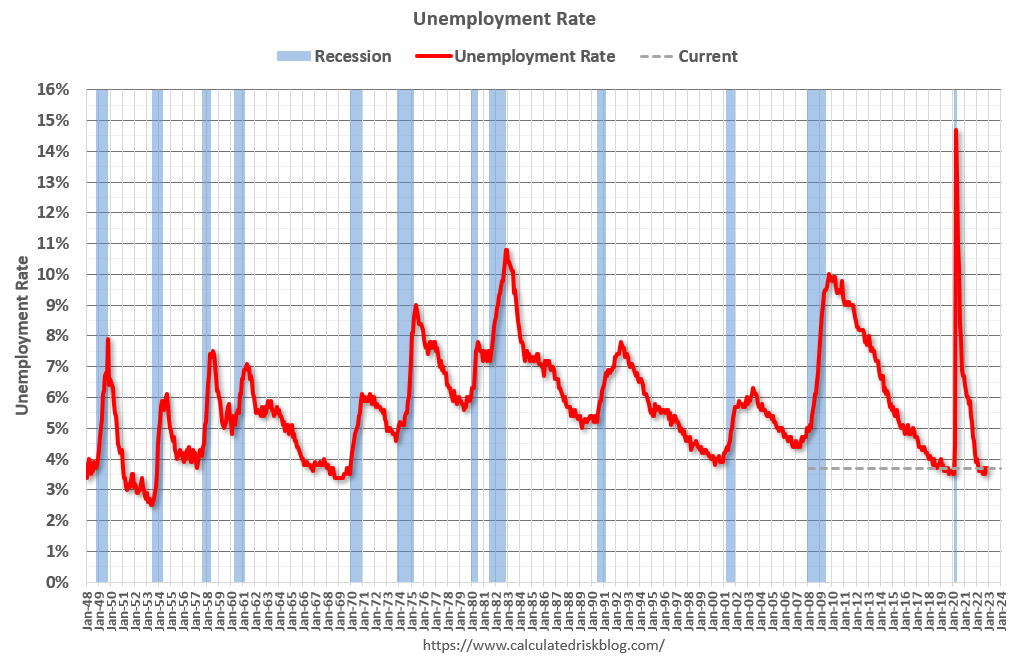

US jobs were strong again:

Total nonfarm payroll employment increased by 263,000 in November, and the unemployment rate was unchanged at 3.7 percent, the U.S. Bureau of Labor Statistics reported today. Notable job gains occurred in leisure and hospitality, health care, and government. Employment declined in retail trade and in transportation and warehousing.

…The change in total nonfarm payroll employment for September was revised down by 46,000, from +315,000 to +269,000, and the change for October was revised up by 23,000, from +261,000 to +284,000. With these revisions, employment gains in September and October combined were 23,000 lower than previously reported.

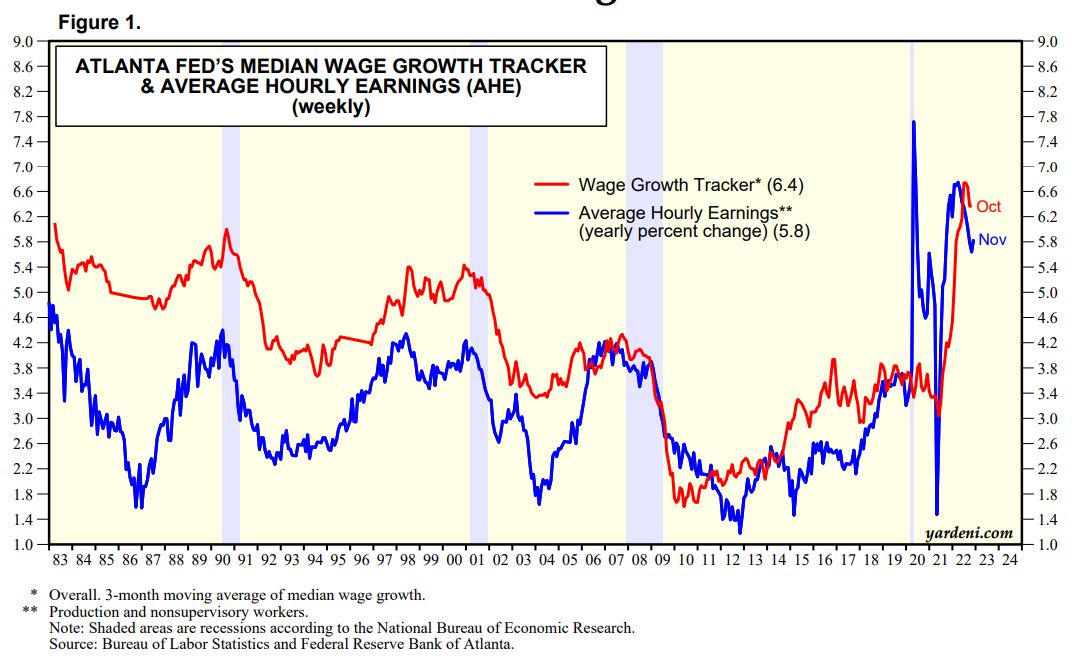

Wages are softening but it’s not convincing yet. November was the highest monthly growth all year:

Advertisement

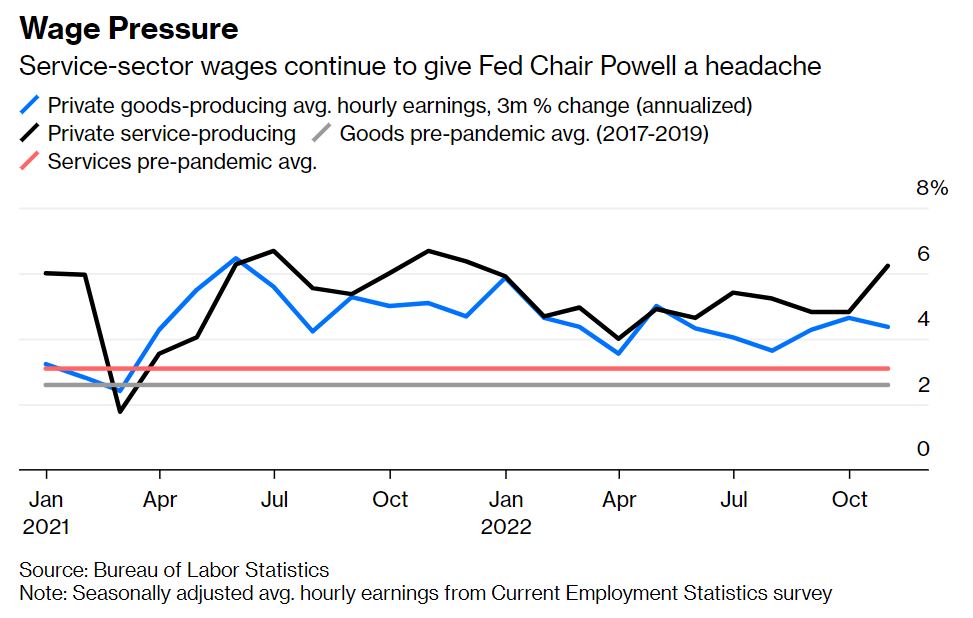

Which is a problem for the Fed as goods wages fade but services wage growth trends higher:

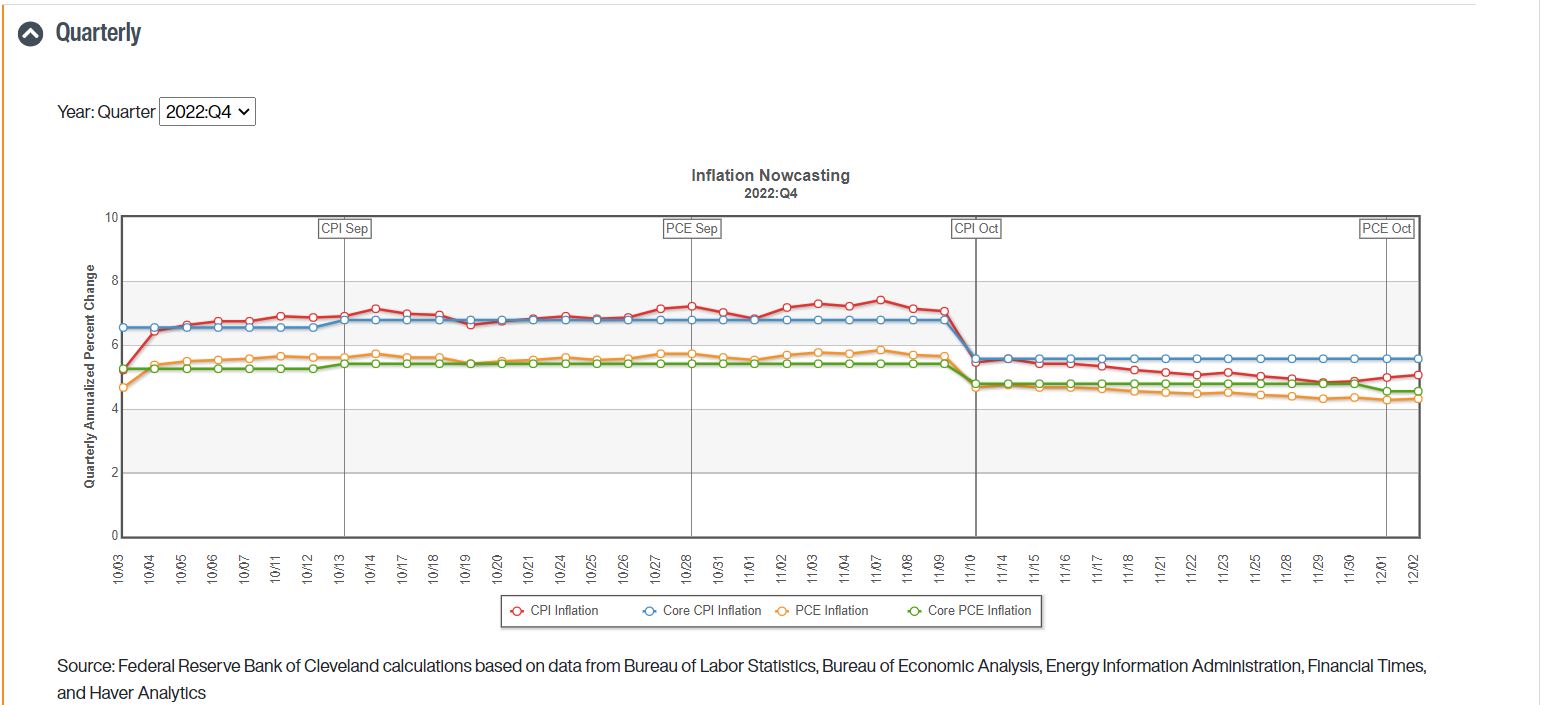

And is why the Fed CorePCE nowcast measure is so sticky:

“We have a long way to go to get inflation down” to the Fed’s target, Summers told Bloomberg Television’s “Wall Street Week” with David Westin. As for Fed policymakers, “I suspect they’re going to need more increases in interest rates than the market is now judging or than they’re now saying.”

Interest-rate futures suggest traders expect the Fed to raise rates to about 5% by May 2023, compared with the current target range of 3.75% to 4%. Economists expect a 50-basis point increase at the Dec. 13-14 policy meeting, when Fed officials are also scheduled to release fresh projections for the key rate.

“Six is certainly a scenario we can write,” Summers said with regard to the peak percentage rate for the Fed’s benchmark. “And that tells me that five is not a good best-guess.”

“For my money, the best single measure of core underlying inflation is to look at wages,” said Summers, a Harvard University professor and paid contributor to Bloomberg Television. “My sense is that inflation is going to be a little more sustained than what people are looking for.”

…While a number of US indicators have suggested limited impact so far from the Fed’s tightening campaign, Summers cautioned that change tends to occur suddenly.

“There are all these mechanisms that kick in,” he said. “At a certain point, consumers run out of their savings and then you have a Wile E. Coyote kind of moment,” he said in reference to the cartoon character that falls off a cliff.

Advertisement

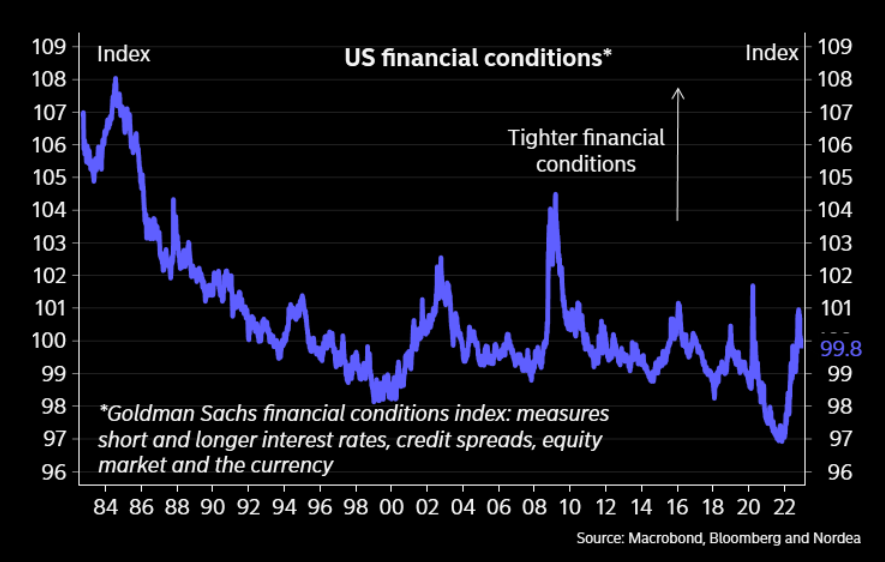

I agree with that. But not yet. After all, the Fed’s just allowed the equivalent of 200bps+ of easing back to around the average:

We’re going to see a mechanical fall in US inflation to 4-5%. The Fed may still need to tighten beyond the 5% terminal rate to finish the job.

Advertisement

It remains my view that there is one more round of AUD smash before this tightening cycle is done.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.