Below is an edited extract from Westpac’s latest Housing Pulse, which forecasts further heavy price falls for Australian property on the back of aggressive interest rate hikes from the Reserve Bank of Australia (RBA).

___________________________________________________________________________________________

Australia’s housing correction is showing no signs of letting up, prices and turnover again moving lower since our last report and declines spreading to more sub-markets…

Interest rate rises remain the dominant driver, a steep 2.75ppt increase in standard variable mortgage rates since Apr sharply curtailing the borrowing power for new buyers. While there are some tentative signs that the pace of price declines may be moderating, we are unlikely to see a stabilisation any time soon…

Housing is now hostage to the policy and economic cycle – how these play out will shape market outcomes from here. Two specific factors stand out: 1) how the inflation outlook evolves; and 2) how heavily rate rises impact the wider economy…

Heading into late 2022, the picture around current conditions and the near-term outlook remains bleak. Our Nov Housing Pulse finds the correction becoming more firmly entrenched in most markets and in buyer sentiment. Price-driven improvements in affordability are being negated by rising interest rates and deteriorating expectations for prices and labour markets…

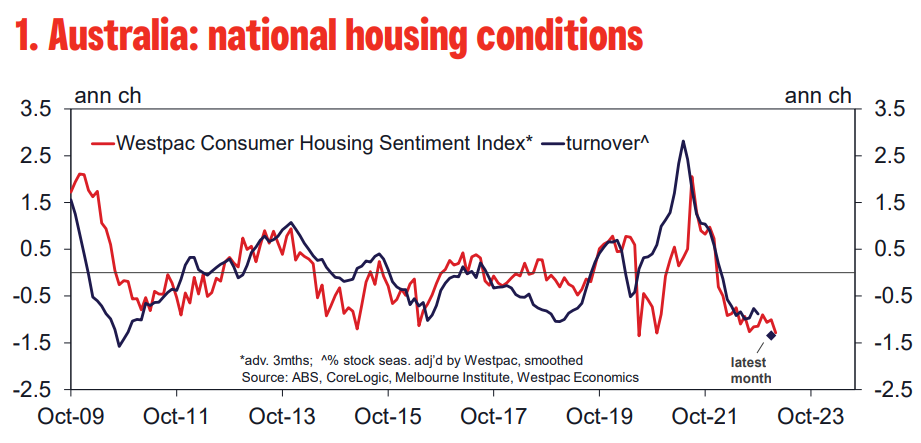

Australia’s housing markets remain in the grips of a material, correction phase that has continued to deepen over the last three months. Nationally, turnover is down 21% from its postdelta highs this time a year ago. Prices across the five major capital cities are now down 7.8% from their peak in Apr with detailed local area markets covering nearly 85% of all dwellings experiencing price declines since mid-year.

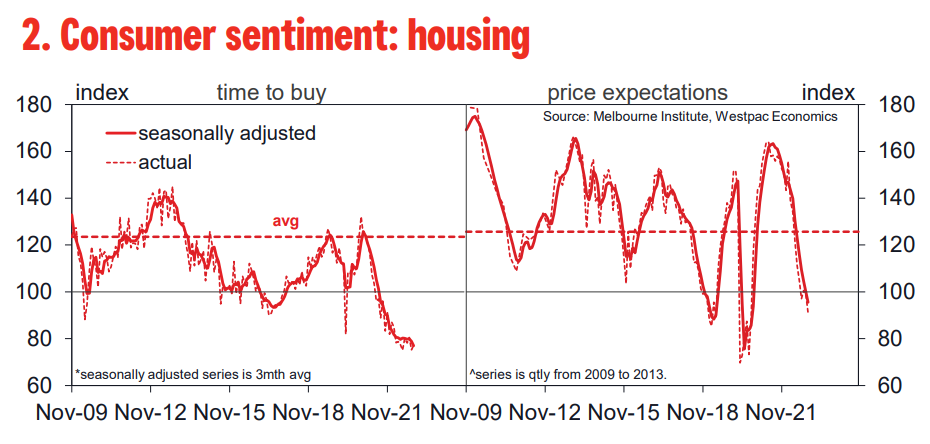

Housing–related sentiment remains extremely weak with signs that a further weakening may be on the way. Assessments of ‘time to buy’ remain near historic lows, rising interest rates over-riding any price-driven improvements in affordability. Price expectations have continued to slide sharply, the move to outright pessimism in the last few months a sign that price declines are now firmly entrenched. Also notable is what looks to be the beginning of a weakening in confidence around jobs, which had been strongly positive. If price expectations and labour markets continue to head south this could see housing-related sentiment and markets take a new leg lower…

Nationally, the Westpac Melbourne Institute ‘time to buy a dwelling’ index declined a further 1.4% over the 3mths to Nov. At 77.1, the Index continues to hold around post-GFC lows, albeit a bit above the extreme 70-75 reads in 2008. The Index has been stuck in the 75-80 range since Mar, 40-45% below the most recent peak in Nov 2020.

Price expectations continue to be scaled back dramatically and are now outright pessimistic. The Westpac–MI Consumer House Price Expectations Index fell a further 13% over the 3mths to Nov to a new cycle low of 91.1. While this is still above the weakest reads seen during the initial onset of the pandemic and during the 2018-19 market correction, it marks the first clear move into sub-100 ‘outright pessimism’ territory – consumers expecting house prices to decline now outnumber those expecting them to rise. This will entrench price weakness, with expectations of falls now likely to frame decisions by both buyers and sellers, i.e. encouraging buyers to take their time and sellers to accept low price offers now…

On balance, we expect the RBA to continue raising interest rates, with a further 1ppt in rises between now and mid-2023. Policy easing is expected to come through 2024 but only if a sustained return to 2-3% inflation appears secure.

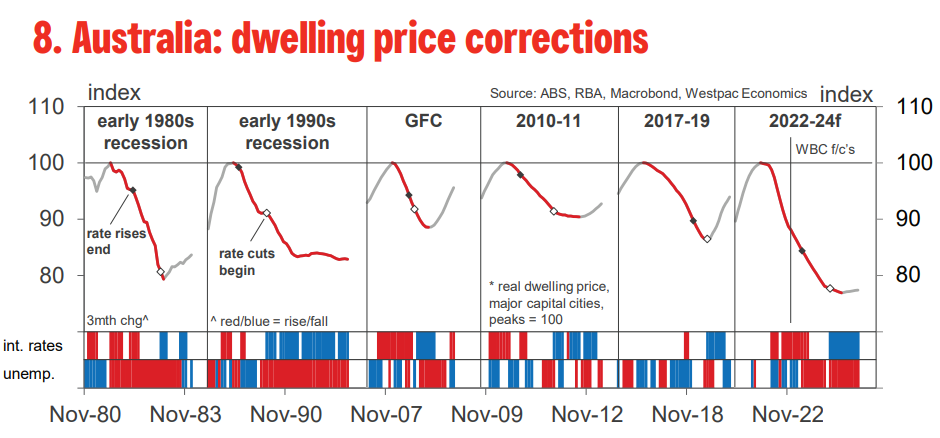

For housing, this essentially locks in a further period of correction through 2023 before a recovery in 2024. History shows corrections tend to come in three distinct phases – an initial weakening driven by rate rises; followed by a period in which rates are on hold but at high levels and a weakening economy becomes a more significant drag; and a final phase where rate cuts and stabilising economic conditions generate a recovery (see Chart 8).

The current correction will enter ‘phase 2’ in 2023. The timing of ‘phase 3’ depends on how readily the RBA can pivot to rate cuts and the extent of the tightening shock to the economy. The last three corrections have been relatively mild, thanks in part to benign inflation backdrop and mild economic contractions. The current correction faces a more difficult combination.