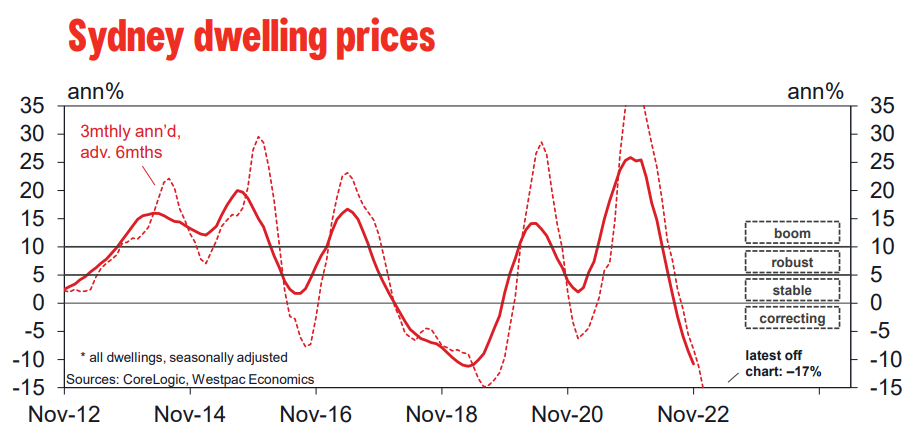

Below is Westpac’s latest analysis on Sydney’s housing correction, where values have fallen by more than 11% from peak, according to CoreLogic’s daily dwelling values index.

“Top tier” suburbs are leading the decline, with more weakness expected near term.

_____________________________________________________________________________________________

The housing correction is more advanced in NSW, having started earlier in the piece and run at a faster pace. Sales are down 35%yr with Sydney prices down 10% for the year. Our sentiment–based indicators point to more weakness near term. About the only ‘positive’ in the mix looks to be an even sharper pull-back in listings. But while the absence of a large overhang of unsold stock will limit some of the downside on prices, its unlikely to stabilise things given momentum and how it is becoming entrenched in expectations.

To be fair, the tone from recent data has been less dire. Auction clearance rates have lifted, Sydney’s clearance rates nudging back above 60% – seen as the ‘gain line’ for prices. Price declines have also slowed, to 1.1%mth from 1.5%mth through Q3. That said, both shifts likely reflect the pull-back in sellers. Auction volumes remain low and withdrawals high. This time of year is also prone to seasonal quirks.

The price detail shows more abrupt turnarounds for houses and ‘top tier’ segments in Sydney. Prices are reversing more quickly in the Eastern Suburbs, Northern Beaches and North Sydney – which outperformed during the boom – but holding up better in the outer western suburbs which lagged on the upturn. Byron Bay is the stand-out weak spot regionally.

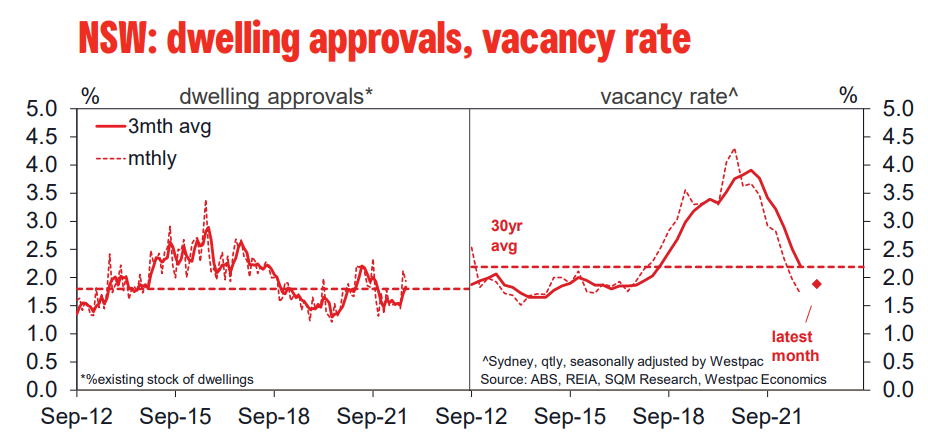

As noted, new listings are now running more in line with weak sales, by about 8% although the total stock of listings is still a touch above long run averages. Rental vacancy rates have continued to tighten and are now below long run averages.

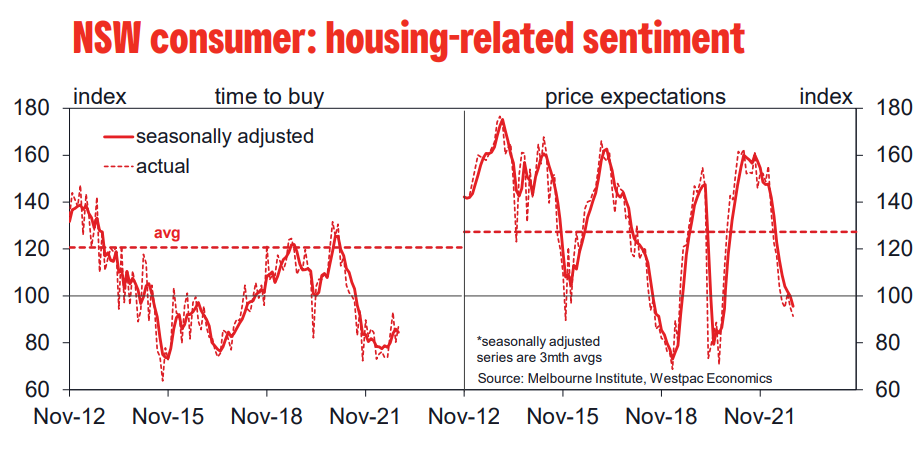

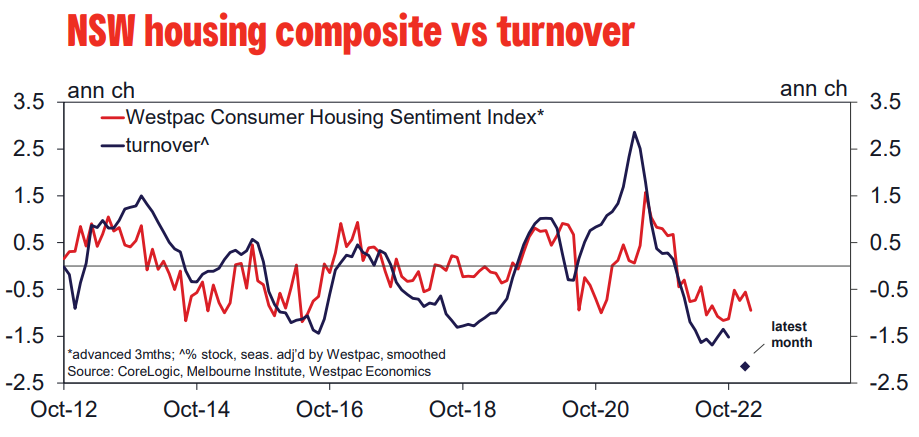

The NSW Consumer Housing Sentiment index points to a further significant decline in turnover near term. Any traction around affordability is being negated by deteriorating expectations for prices and labour markets.