TSLombard with the note.

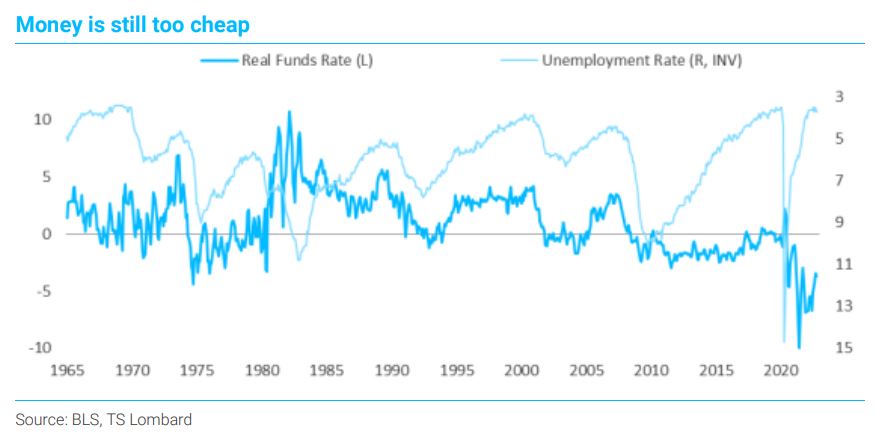

The sustained strong pace of job growth well above neutral (100,000/month, or thereabouts), the high diffusion index of 61.7, the low unemployment rate and the still high pace of wage hikes, all add up to continued strong demand for labor. More to the point, money is still priced too cheap against this reality (see chart below).

As for the household survey, the data paint a much weaker story. Comparing the change in total employment (using the payroll definition for household survey) since March, the payroll survey shows 2.5 million jobs added versus 600,000 in the household survey. Which is right? History has generally proven out the establishment survey to be the more accurate off of which to forecast spending – and establishment data today coincide with the continued low numbers for initial claims for unemployment insurance. The recent run of jobs data support my expectation that Q4 real GDP growth will be close to 3% Q/Q SAAR, this time built on renewed consumption rather than imports falling off faster than inventory. A recession is coming – but it arrives next year.