Provided by the perpetually bullish Goldman.

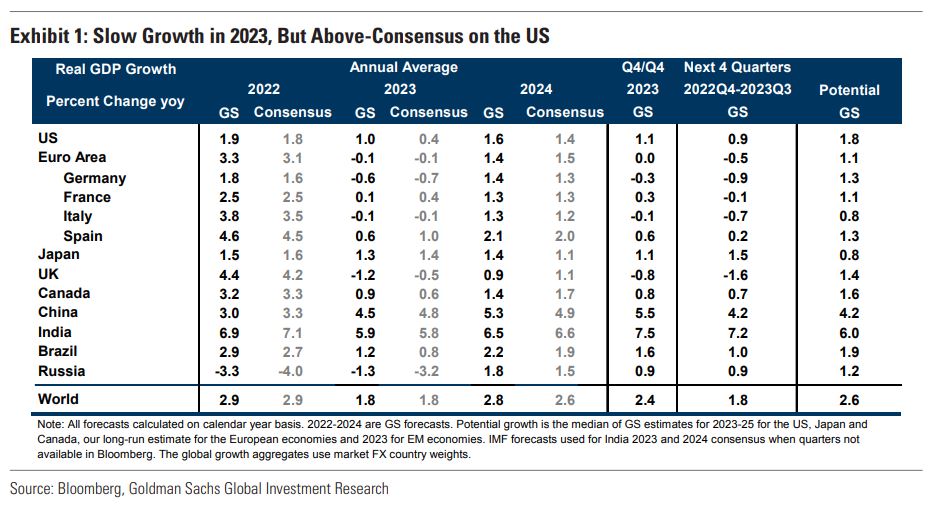

Global growth slowed through 2022 on a diminishing reopening boost, fiscal and monetary tightening, China’s Covid restrictions and property slump, and the Russia-Ukraine war. We expect global growth of just 1.8% in 2023, as US resilience contrasts with a European recession and a bumpy reopening in China.

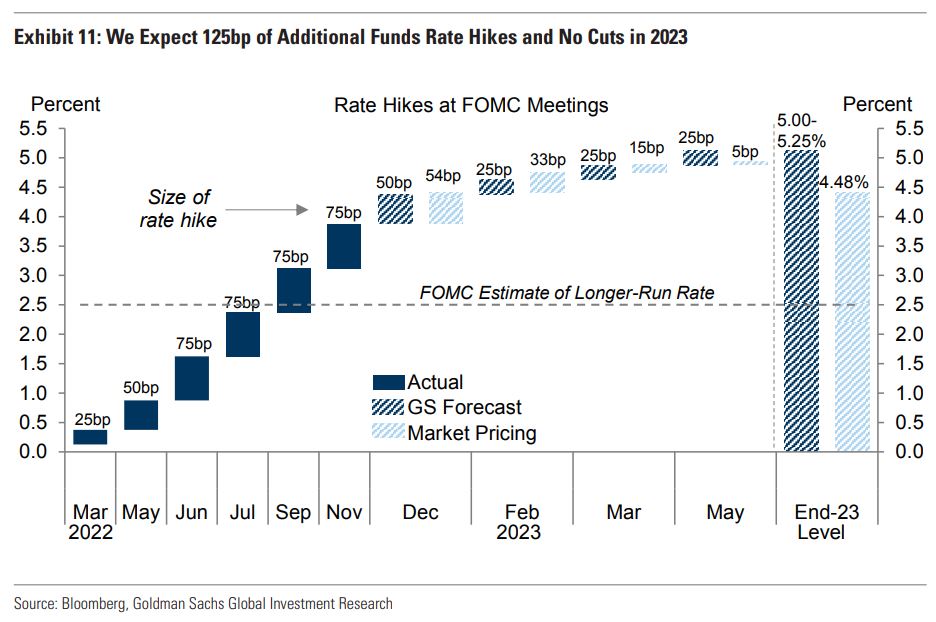

The US should narrowly avoid recession as core PCE inflation slows from 5% now to 3% in late 2023 with a ½pp rise in the unemployment rate. To keep growth below potential amidst stronger real income growth, we now see the Fed hiking another 125bp to a peak of 5-5.25%. We don’t expect cuts in 2023.

Advertisement