Goldman with the note. Next comes goods deflation. Then the breaking of wages and services to follow. Assuming the Fed doesn’t pike it and Albo’s mass immigration gambit lands. It also looks like the inventory rundown has begun, if not yet in earnest.

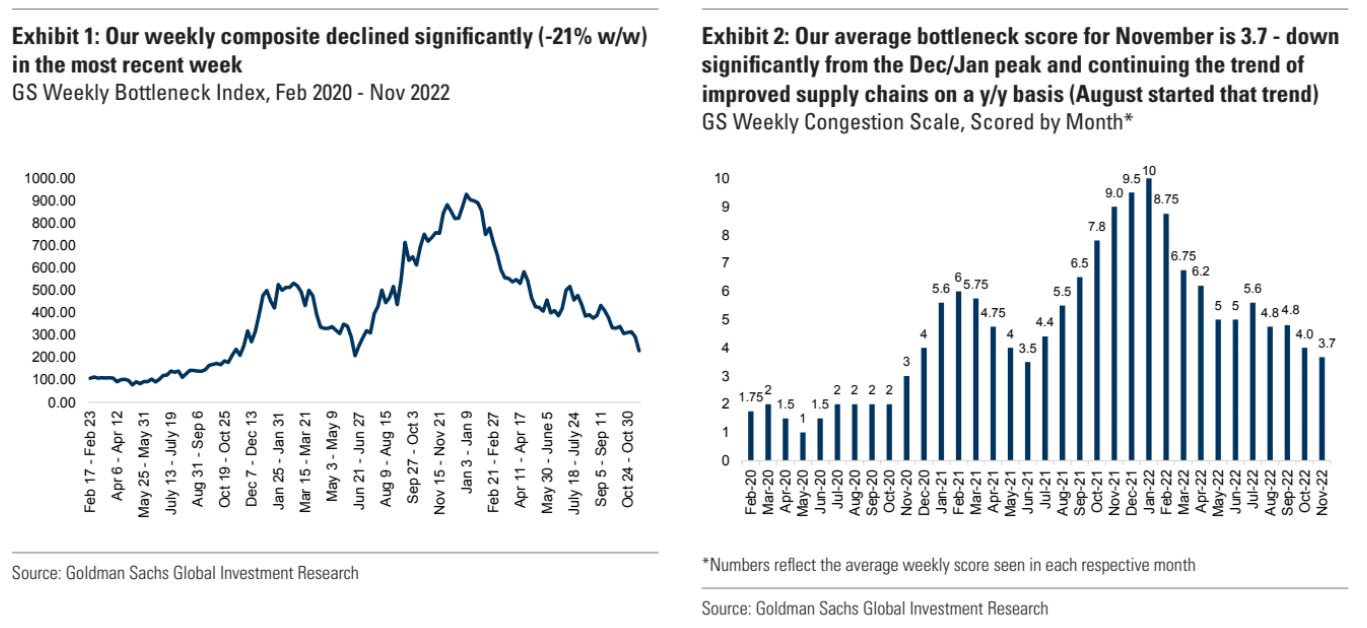

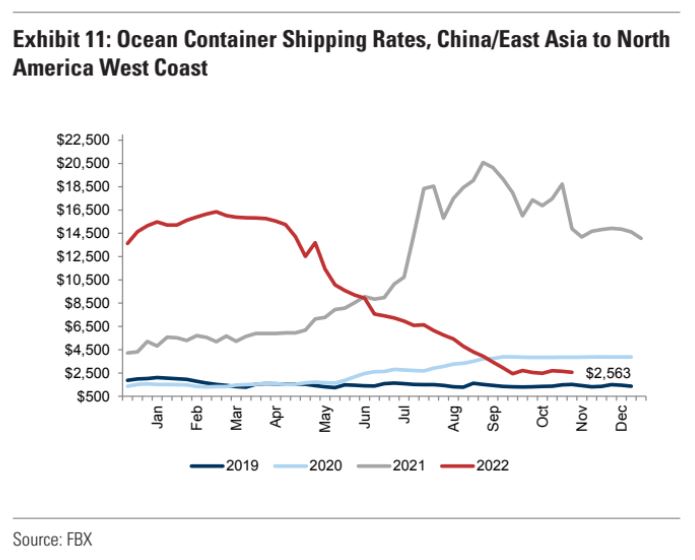

Our weekly bottleneck scale dropped to ‘3’ from ‘4’ this week as the absolute level of our congestion index moved significantly lower (-21% w/w; Exhibit 1); we are now 19% below ‘4’ and 20% above ‘2’ territory. The number of container ships waiting to dock and unload goods along the West Coast was cut in half (5 ships vs. 10 last week), while East Coast backlogs decreased significantly (42 ships vs. 52 last week); the combined backlog decline was ~24% w/w, or the single largest week of relief seen for all of 2022 (Exhibit 7). Chassis dwell times also improved sequentially (-13% w/w on average), though West Coast rail performance was somewhat mixed again (UNP intermodal train speed/dwell deteriorated; BNSF dwell improved, but speed deteriorated) as combined West Coast intermodal traffic levels declined w/w (Exhibit 8). Ocean container shipping rates (China to US West Coast) remained down more than 80% YoY, and the rate of decline was essentially unchanged versus the prior week (Exhibit 11).

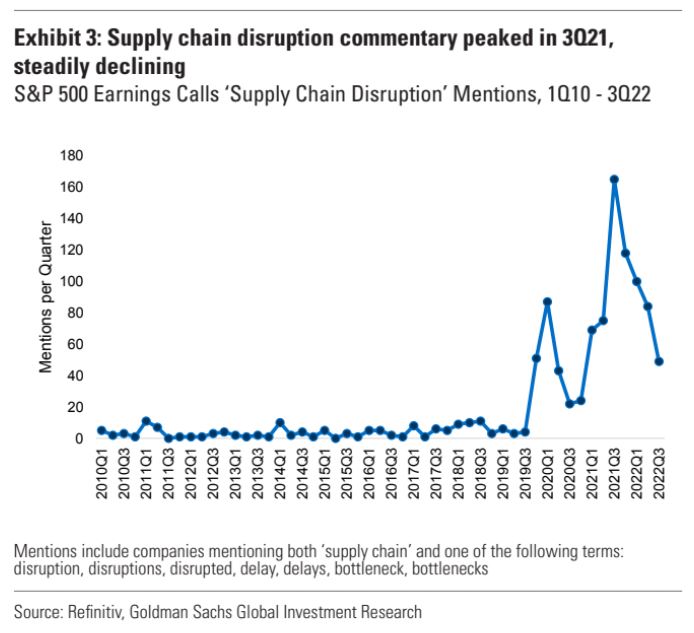

Overall, November’s bottleneck scale is tracking at around 59% YoY improvement on average (3.7 vs. ~9.1) — which is an accelerated pace compared to ~49/25/13% YoY scale improvement in October/September/August (Exhibit 2). Staying at current levels would imply even more improvement in December (~60% YoY), albeit still slightly elevated versus pre-Covid levels; we still expect the pace of bottleneck relief, and hence our path to ‘1’ on our overall scale, to remain lumpy at times – reflecting inventories working their way through the supply chain, short-term rail dislocations and network recovery, and/or start/stops in China. That said, we reiterate our view that we have far passed the worst of the congestion — and recent improvements to container ship backlogs screens as encouraging if further sequential improvements arise in the coming weeks. Notably, mentions of supply chain disruptions via company earnings calls continue to decline – providing additional anecdotal corroboration to our index as to the easing of overall congestion (Exhibit 3).