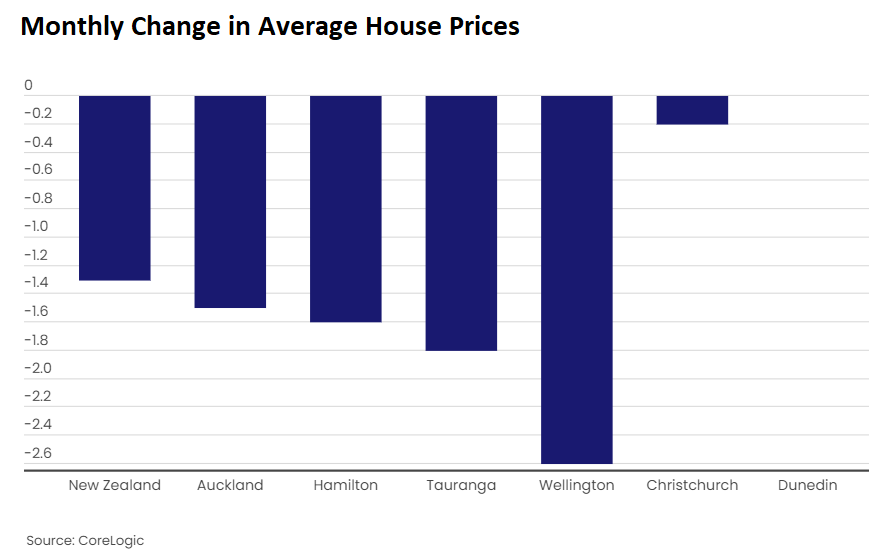

CoreLogic New Zealand has released its price results for October, with average values nationally declining 1.3% over the month with all six major regions declining:

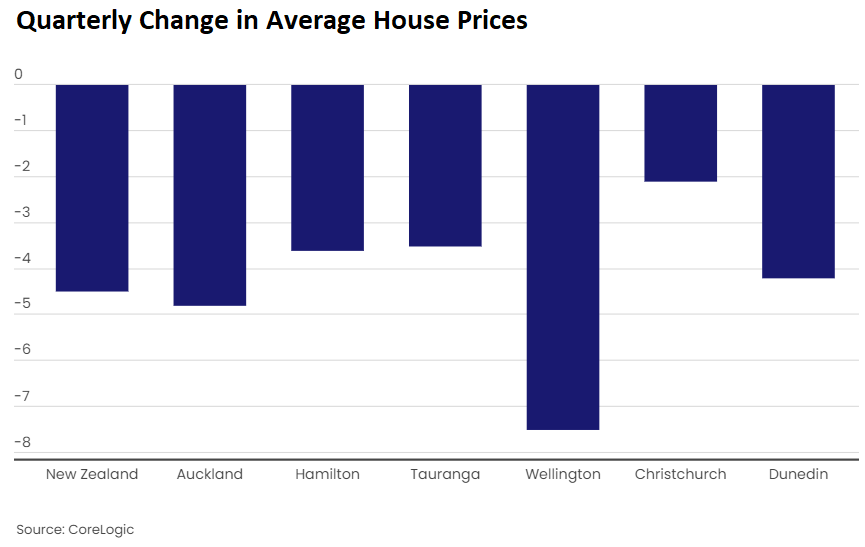

Over the October quarter, values nationally plunged 4.5%, again with all major regions falling:

Advertisement

CoreLogic NZ Head of Research, Nick Goodall, noted that broad expectations are for New Zealand house prices to fall sharply peak-to-trough; although not by enough to take values back to pre-pandemic levels:

“All banks have revised their house price forecasts down in the wake of the latest data and if we assume an -18% fall from peak-to-trough, that would take the average price to $855,000, still a lot higher than March 2020. The average value prior to the pandemic hitting our shores in Feb 2020 was $723,000. To get back to that value would necessitate a -31% fall – not something anyone is forecasting, yet”.

The Reserve Bank of New Zealand (RBNZ) also released its half yearly Financial Stability Report (FSR), which noted that values have to continue falling to return to sustainable levels. It also warned that further sharp price falls “remains plausible”:

Advertisement

Our assessment is that New Zealand house prices remain above sustainable levels. A continued gradual decline in prices towards more sustainable levels remains desirable for long-term financial stability…

Given the recent fall in house prices, the gap between the current price level and our estimates of its sustainable level has narrowed. However, our assessment of the sustainable level of house prices has also declined, owing to market expectations for higher long-term interest rates and historically low levels of rental yields, both of which make residential properties relatively less attractive compared to six months ago…

In the near term, we expect prices to continue to fall towards more sustainable levels as the effects of higher mortgage rates feed through to declining demand for housing. A sharp decline from the current price level remains plausible, as the low mortgage rates that drove the recent run-up in prices reverse.

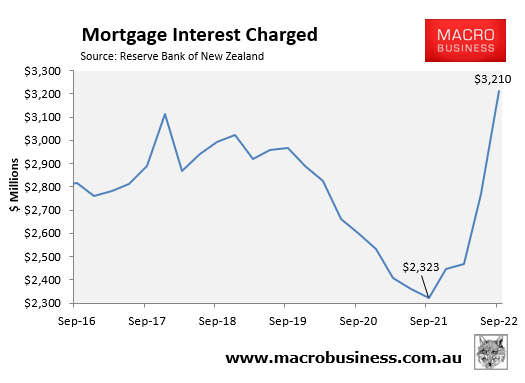

Despite the sharp fall in prices to date, the sharp rise in mortgage rates has meant that the debt servicing burden for new buyers remains at an historically high level:

Advertisement

The situation will obviously worsen as the RBNZ lifts rates further and the tidal wave of borrowers currently on one to two year fixed rates expire:

Household debt servicing costs have increased as mortgage rates have risen. Many borrowers from late 2020 to early 2021 fixed their lending at low 1-2 year rates, and are only now gradually repricing onto the much higher interest rates prevailing in the market. The value of new mortgages from 2020 and 2021 is estimated at about 40 percent of the current mortgage stock, with 10 percentage points of this being first-home buyers. Around half of the stock of mortgages on fixed rates is expected to reprice in 2022, increasing serviceability pressure on these borrowers.

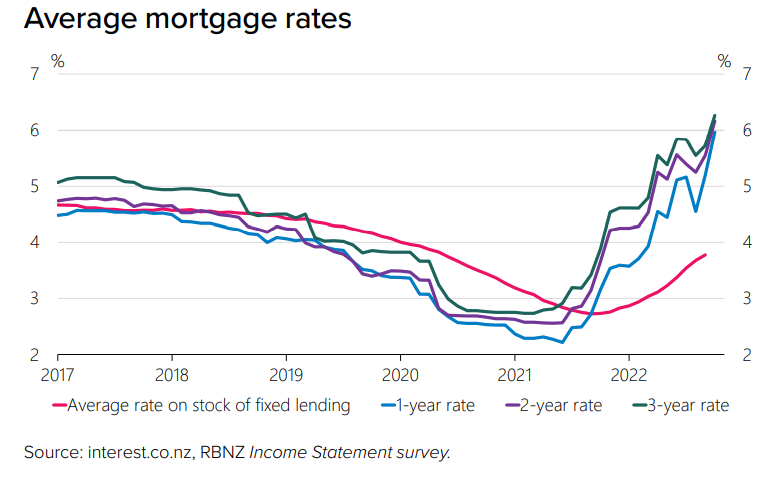

Note the pink line above showing that average rates on the stock of fixed lending is lagging way behind advertised mortgage rates.

Advertisement

As the cheap fixed mortgages taken out over the pandemic expire next year, and reprice to 6% or above, repayments will necessarily soar.

That is when the impact of the RBNZ’s aggressive rate hikes will truly be felt by Kiwi mortgage holders.

Leith van Onselen is Chief Economist at the MB Fund and MB Super. He is also a co-founder of MacroBusiness.

Leith has previously worked at the Australian Treasury, Victorian Treasury and Goldman Sachs.