Independent economist Tony Alexander believes this week’s strong employment and wage data will inevitably prompt the Reserve Bank of New Zealand (RBNZ) to hike the official cash rate (OCR) by at least 0.5% and possibly by 0.75% at this month’s monetary meeting.

Alexander also notes that the “risks for inflation still seem to lie on the upside”, which will likely lead to further OCR hikes in the new year.

_______________________________________________________________________________________________

At the moment it really doesn’t matter what collection of data you look at. The risks for inflation still seem to lie on the upside even though we can see clearly that there is a strong cutback in consumer spending underway. Off importance here are the results of my monthly spending plans survey which I will release next week. Suffice to say that with most responses in consumers have gone right back into their shells again following the recent round of increases in mortgage interest rates.

Consumer spending is being crunched. The next step then is seeing a reduction in business pricing intentions and that is where the labour market data are important. If the labour market remains tight and wages growth strong there’s going to remain a natural bias for businesses to want to increase their selling prices by much more than the average inflation rate over the past three decades of 2%.

That is the space we are in at the moment, and we can only guess as to how long it’s going to take for business pricing intentions to really pull back.

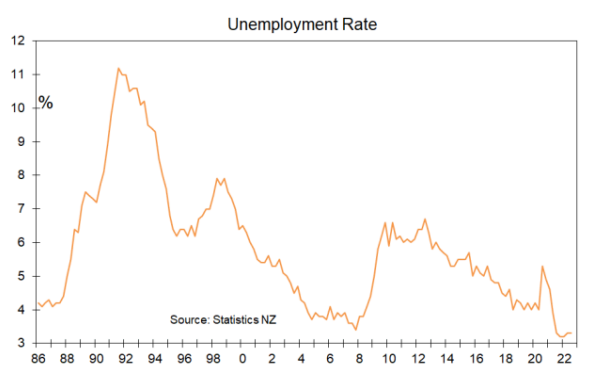

So, what did the labour market data yesterday tell us? First, the unemployment rate held steady at 3.3% which was close enough to general market expectations of a potential small decline to 3.2% or 3.1%. There result is neither here nor there and not interesting in the context of trying to gauge how inflationary pressures are changing.

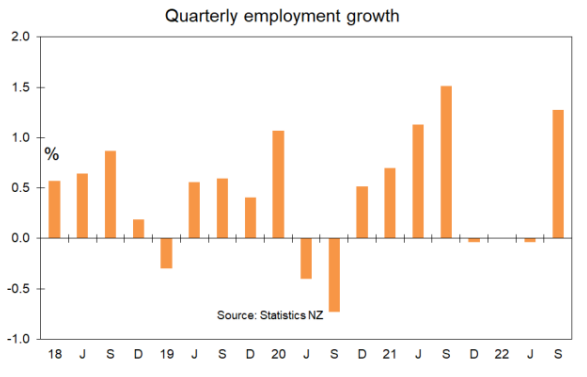

However, after three quarters in which we have seen zero growth in the number of people employed in New Zealand there was a strong jump of 1.3% during the September quarter. A lot of this will reflect the ending of the lockdowns and the opening of the borders boosting employment in the widely defined service sector.

Total job numbers have increased by 1.2% over the past year and are 5% greater than at the end of 2019 just before the pandemic struck.

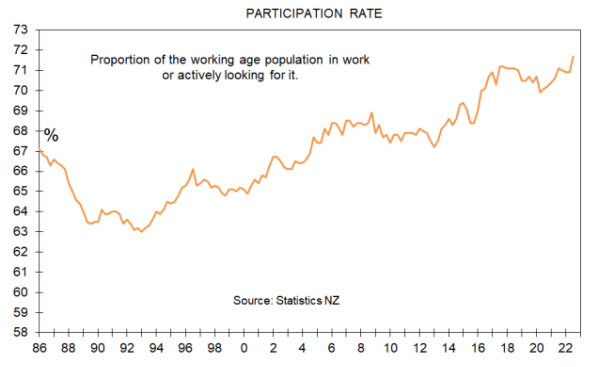

The proportion of the working age population which is in work and known as the participation rate has risen to a record high level of 71.7% from 70.9% last quarter and 71.1% a year ago.

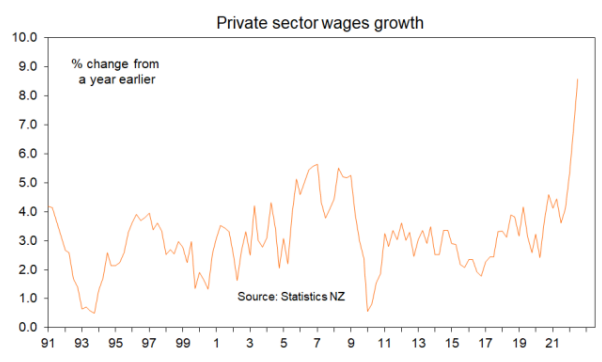

The data on wages however are the ones we are tending to pay most attention to at the moment. In that regard almost every measure showed a firm rise in the September quarter and the September year.

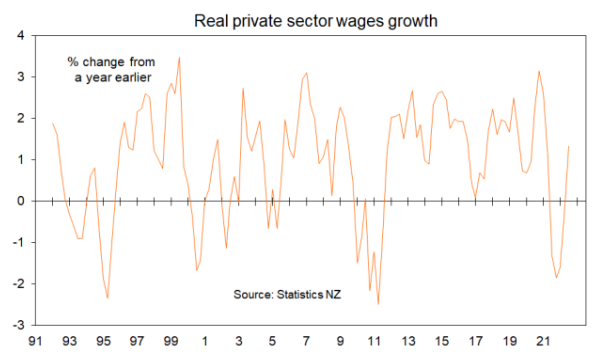

The average pace of increase in wages as measured by the change in ordinary time earnings in the private sector increased to a record 8.6% in the year to September from 7% in the year to June and 3.6% a year earlier.

Wages growth is very strong and exceeds the inflation rate of 7.2%. That is, real wages are once again increasing. On average over the past quarter of a century real wages have grown by 1.2% a year by this measure.

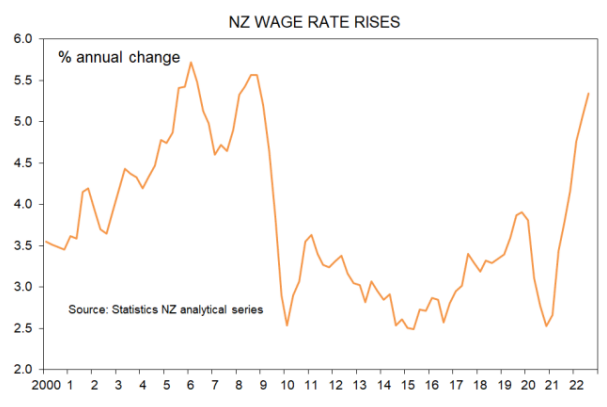

I have reported this measure because it is the most popular one discussed. However, I have long had a soft spot for an experimental labour cost index produced by statistics New Zealand which focuses more on pure wage changes for an unchanging mix of jobs.

This measure for the private sector increased by 1.6% in the September quarter which was the same pace of increase as in the June quarter. The rise from a year ago was 5.6% from 5.2% in the June quarter and 4.1% a year ago.

Case following graph shows this represents a strong lift in the price of wages growth to the highest level in over 12 years. But the pace of growth as yet is not as strong as it was during the peaks just before our 2008 recession which was then followed by the global financial crisis.

What this is telling us is that people are boosting the earnings by shifting to higher paying jobs. That is a good thing and it raises the possibility of an acceleration in the pace of productivity growth in the New Zealand economy.

What are the main implications of the labour market data? In simple terms in no way do they suggest that the New Zealand labour market is weakening off as a result of the monetary policy tightening which has happened so far. The numbers say that wages growth is likely to remain firm, that businesses will struggle even more to find the staff that they want, and that the Reserve Bank will continue to take the official cash rate higher.

Whether the peak in the official cash rate from the current 3.5% is 4.5% or the 5.5% which markets are pricing we really don’t know. There is much water to go under the bridge with regard to the extent to which the pace of growth in the economy slows, the speed with which weakness in the labour market comes along, and the speed with which inflation comes down and can be reasonably expected to go back within the target range of 1 to 3%.

And so now it’s on to the next set of data which might give new insight into where inflation is heading and then the next review of the official cash rate by the Reserve Bank on November 23. On that date they are guaranteed to raise the official cash rate by at least 0.5% and a 0.75% increase is a reasonable possibility.