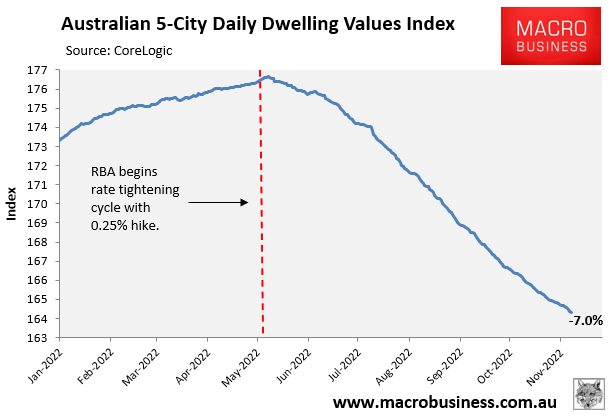

As we know, Australian dwelling values are falling at their fastest pace on record, down 7.0% across the five major capitals according to CoreLogic’s daily dwelling values index:

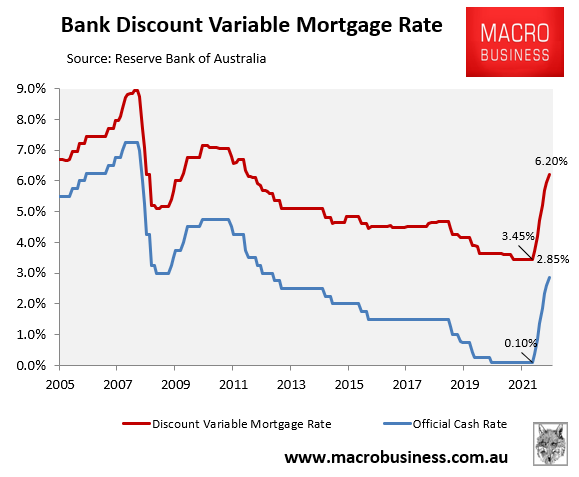

The reason for this price decline is shown clearly by the red line in the chart above: the Reserve Bank of Australia’s (RBA) aggressive monetary tightening, which has seen the official cash rate (OCR) soar 2.75% since May.

In turn, average discount variable mortgage rates have soared to 6.20%, up from 3.45% in April – representing the sharpest increase in mortgage rates on record:

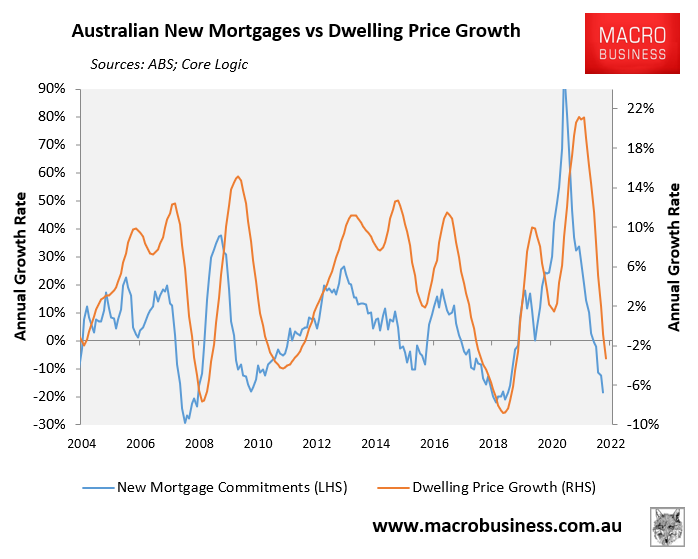

This increase in mortgage rates means less borrowing capacity. Accordingly, the growth in the value of new mortgage commitments – the key driver of house prices – has turned negative, sending home values sharply lower:

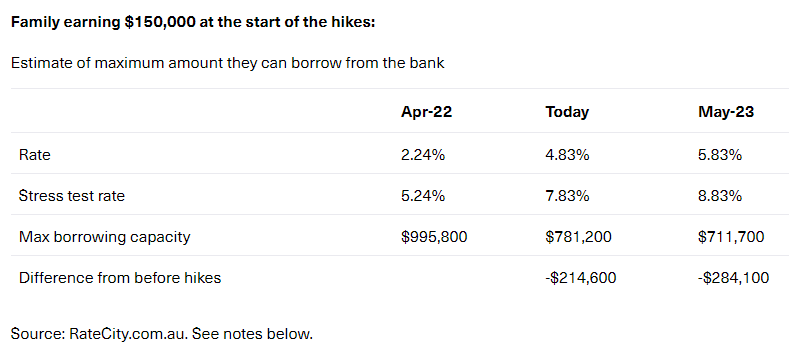

In fact, new analysis from Finder shows that typical homebuyer budgets have been slashed by 22% following the RBA’s cumulative 2.75% of monetary tightening, equating to $214,000 less buying power for the typical family:

Finder also estimates that if the OCR was to rise to 3.85%, as forecast by Westpac, then buying power would fall by 29% (-$284,100) for the same representative household.

RateCity.com.au research director, Sally Tindall, explained that “the average family earning $150,000 a year will have seen the maximum amount they can borrow from the bank shrink by around $214,600 across the last seven hikes”.

In turn, “ABS data shows the value of new lending has dropped to its lowest value in almost two years – a trend that’s likely to continue as both sellers and buyers put their plans on ice”.

The above analysis explains why Australian house prices will continue to fall as the RBA hikes rates. They also won’t recover until the RBA changes track and begins the next rate cutting cycle, which will increase borrowing capacity and homebuyer budgets.