Independent economist Tony Alexander has released a report explaining how “the recent round of mortgage interest rate rises” has seen New Zealand first home buyers “hit the pause button” and investors “run right back into the hills”.

However, Alexander still believes that we are approaching the “endgame” of falling property prices in New Zealand and that a modest rebound will emerge from mid-2024.

_________________________________________________________________________________

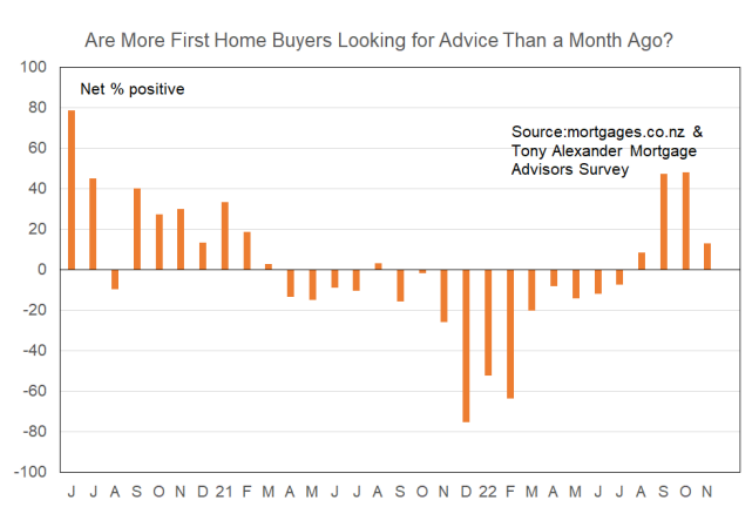

On Tuesday I released the results of my latest monthly survey of mortgage advisers undertaken with mortgages.co.nz. The key results are that first home buyers remain in the market but have hit the pause button on their speed of purchasing to see what happens with interest rates.

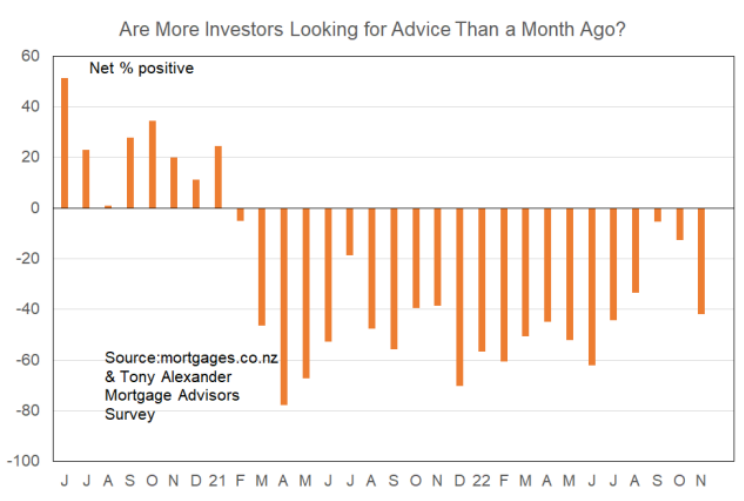

Investors have however run right back into the hills. A net 42% of advisers say that they are seeing fewer investors compared with a net 13% a month earlier.

Investors packed up their purchase bags and left town at the start of 2021 as first the LVRs returned and then the tax rules changed from March 27. In the financial year starting April 1, 2023, investors will only be able to deduct 75% of their interest costs from rental income to get taxable income.

The year after that the proportion falls to 50%, then 25%, and come the year starting April 2026 they will not be able to deduct anything – unless they have purchased a newly built property and no, do not even think about emailing me asking what the new purchase rules are.

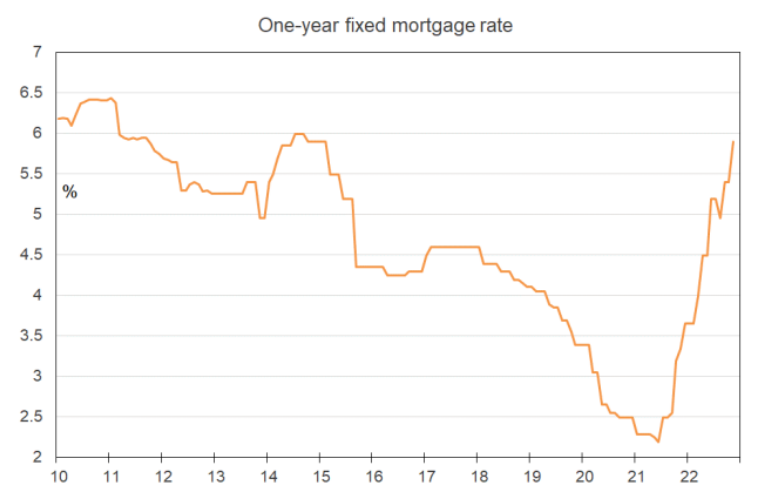

Clearly, the factor in play which accounts for the new stepping back of home buyers is the recent round of mortgage interest rate rises. That means if we are to gauge where things are to head from here and if you are still thinking in terms of picking the bottom of the market for your purchase (good luck) then we need to pay close attention to where borrowing costs are going.

Maybe more accurately, we need to give thought to when people lose their fears of interest rates going higher and expect declines. With a very strong labour market in place and only a slight rise in the unemployment rate expected in the coming 1-2 years it is initial and expected borrowing costs which look like mattering the most for purchase decisions rather than uncertainty about income.

So, can we pick when interest rates will peak? All of us economists can give you a view, but we have all been wrong in the past year both here and overseas. So, don’t look for certainty and do expect whatever forecast you receive to change as new information comes in.

My expectation is that as that sentiment feeds through we will see many buyers who recently stood back from the residential real estate market step forward again. But that will just be a continuation of the endgame we have been in for 3-4 months now and not the end of the downward phase in house prices.

For that to happen we will need solidity around a view on the timing of mortgage rates going down.

In the past such periods of falling interest rates have occurred alongside rapidly rising unemployment and that has meant the housing market kept weakening. But this time around, as noted above, the rise in unemployment will likely be small. That means the speed with which interest rates fall is likely to be slow when it happens – after the initial bout of cuts.

My current pick for when we revert to focusing our attention on a track of interest rate declines with a high feeling of certainty is before the middle of next year. That means I see a good chance of the house price cycle bottoming out before the middle of 2023. But I don’t expect any firm surge in prices when the falls stop.

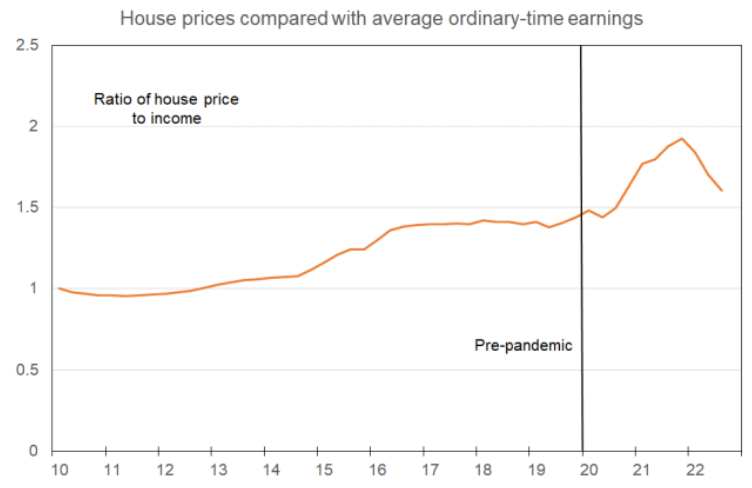

Why will prices rise at all? Many reasons. Here’s one. The ratio of average house prices nationwide to average hourly ordinary-time earnings is now only 8% above March quarter 2020 levels.

In the past year house prices have fallen by 10.9% on average nationwide and this earnings measure has risen by 7.4%. The pandemic surge in the ratio of house prices to incomes will be gone very soon. Then what will we be left with?

1) Average one-year fixed mortgage rates just over 6% from 3.5% back then.

2) An unemployment rate not too far from the 4% back at the start of 2020.

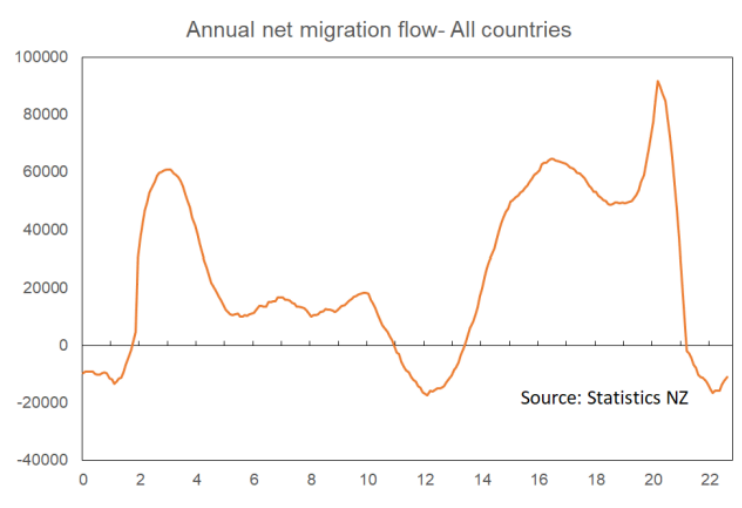

3) A small net migration outflow versus pre-pandemic gain near 60,000.

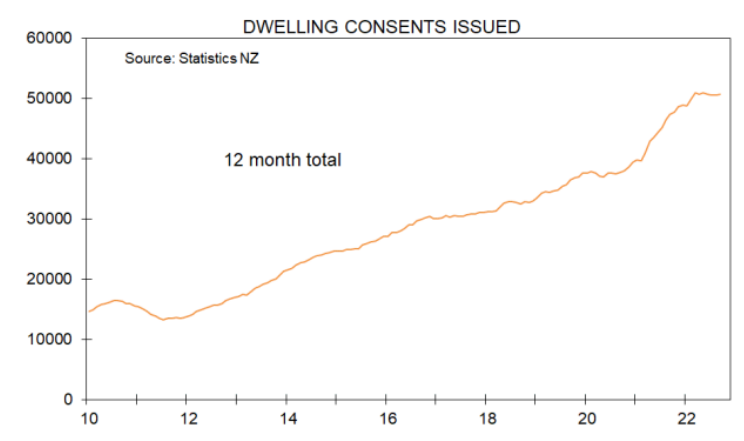

4) Dwelling consents running at 50,000 versus 39,000.

5) A ratio of household debt to income near 173% versus 169%.

6) Greater housing demand from Homes & Communities govt. department.

Note also that in the above graph of house prices versus incomes the ratio is on a rising trend. If you get a straight edge out and extrapolate that trend, you’ll see the ratio is already below it.

All of which leads me to this question. What do you think is going to happen once interest rates are seen solidly as falling, the economic growth forecasts are shifting upward, the election is out of the way, the migration numbers look better, and if National win the election the tax burden on investors is lifted?

The second half of this year is about the endgame for falling prices. Next year will be all about the housing cycle turning. But 2024? Now that will be interesting.