Below is Westpac’s latest analysis on Victoria’s (Melbourne’s) housing correction, which looks “firmly locked in” and “still has some way to run”.

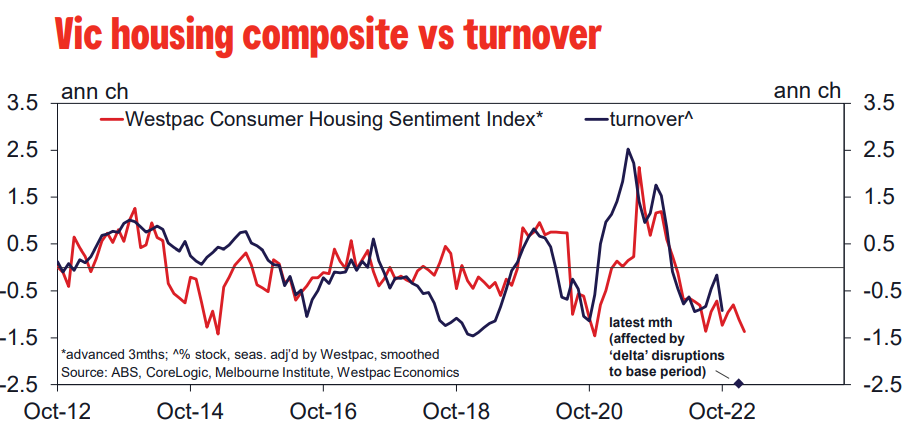

Vic remains firmly locked in a material housing market correction. Turnover is down 30% from its 2021 high (albeit with declines exaggerated by last year’s delta disruptions).

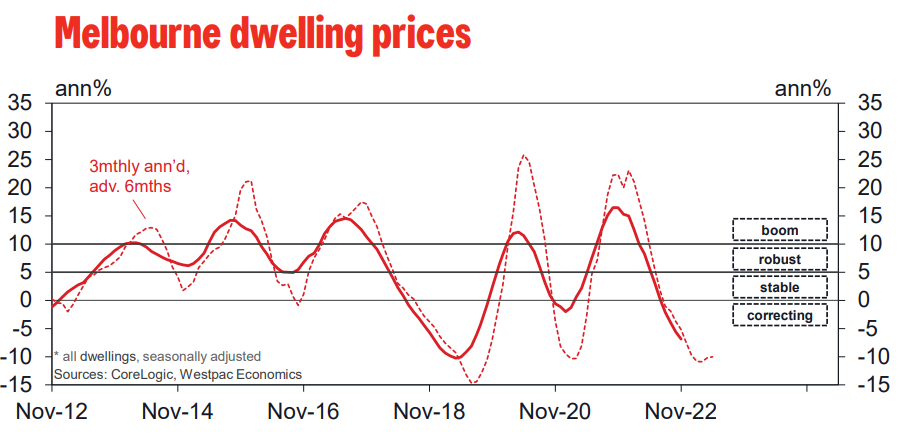

Melbourne dwelling prices are down just 7% from their 2022 peak, monthly declines running at a steady pace despite a moderation since mid-year. Sentiment points to more of the same in early 2023. Affordability and the supply–demand balance remain less supportive than in most other markets although the latter is shifting, the physical demand for housing set to get a big boost as migration inflows return.

Auction markets have firmed in recent months, Melbourne clearance rates nudging back above 60% and pre-auction withdrawals easing. That said, volumes remain relatively low.

The price detail continues to show a fairly uniform picture across tiers and sub–regions, the size of price corrections generally mirroring the strength of preceding gains. This is seeing bigger declines for houses vs units and for ‘top tier’ segments compared to lower tiers. Across sub-regions, Melbourne’s North East and Outer East are leading declines, again with both having outperformed during the upturn. Price growth has also turned down sharply in regional areas, Mornington Peninsula and Geelong now seeing big falls.

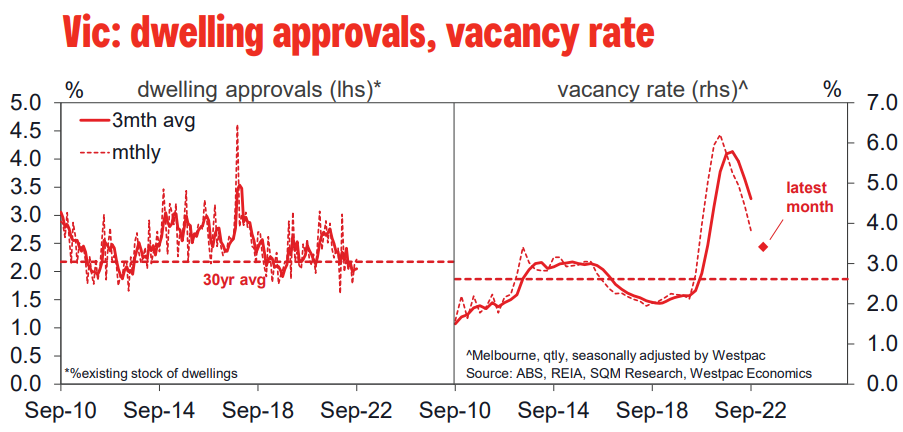

The on–market supply–demand balance is looking more evenly poised following a sharp drop-back in new listings. While low, sales are running slightly ahead of new listings meaning the stock on market is holding steady, near long run averages in the case of houses. Melbourne’s rental vacancy rate continues to drop but is still above historical averages.

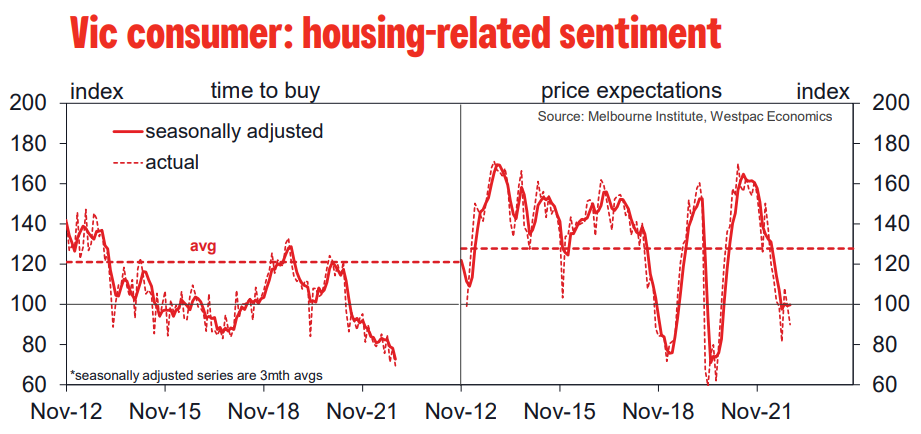

The Vic Consumer Housing Sentiment index points to further declines in turnover heading into 2023. The correction clearly still has some way to run.