Poor risk sentiment is dominating the start of the new trading week with Wall Street putting in a quite negative session overnight on more Fed hawkishness and the developing COVID situation in China. European shares also took a hit despite falling energy prices as it heads into a worrisome winter. The USD came back hard against the major currencies with Euro slammed back to the 1.03 level as the Australian dollar almost made a new weekly low at the mid 66 level. Action on bond markets saw 10 year Treasury yields pushed back above the 3.7% level while the commodity complex was just that with machinations over Venezuelan sanctions and the unrest in China seeing oil prices whipsaw but eventually finishing where they started as Brent crude hovered near its recent monthly low at the $84USD per barrel level while gold fell back in line with undollars to the $1740USD per ounce level.

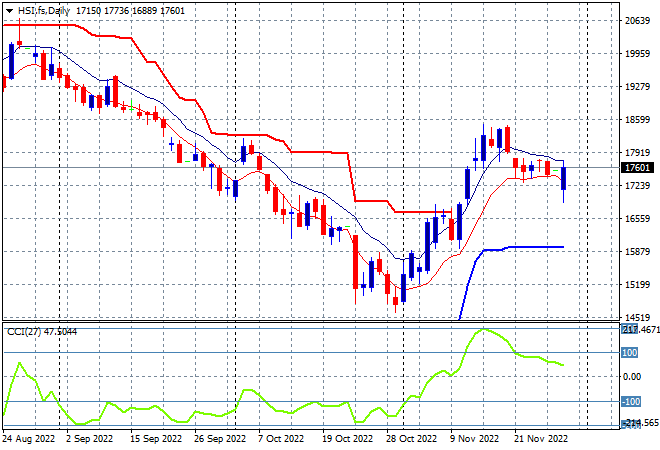

Looking at share markets in Asia from yesterday’s session where Chinese share markets started poorly but managed to fill some losses going into the close with the Shanghai Composite finishing down 0.7% at 3078 points while the Hang Seng Index pulled back even more so, closing nearly 2% lower at 17297 points. The daily chart was showing a small slowdown after having gained nearly 4000 points since testing the 2008 lows with a further retracement now slowly growing as price is not properly defended well at the low moving average area. Its pretty obvious that daily momentum was getting ahead of itself before reaching the magical 20000 point level so watch this retracement to continue to test the recent daily lows below the 18000 point level:

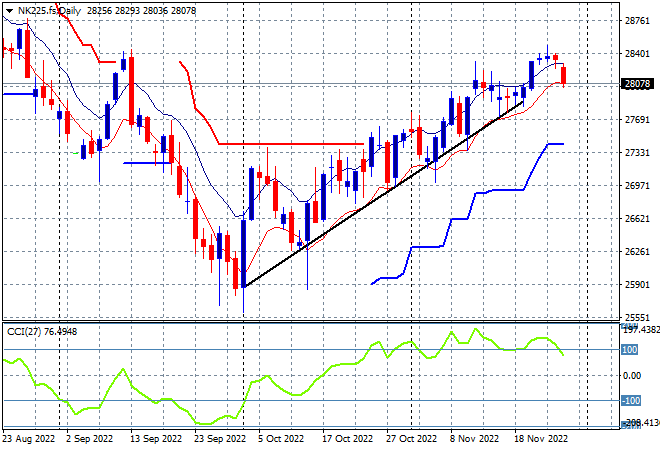

Japanese stock markets are faltering again as we start another trading week with the Nikkei 225 closing 0.4% lower at 28162 points. As I suggested last week a further breakout was brewing here as overhead resistance at the 27500 level is now cleared but the lack of a clear lead from Wall Street will hamper further gains as we start another trading week. Price action is only just above the trendline and looking “toppy” as daily momentum retraces from overbought where support at the 27500 point level must hold to save this uptrend: