Sydney-based buyer’s agent, Jack Henderson, has warned that there has been a marked increase in distressed property sales, especially amongst first home buyers that purchased near the top of the market last year.

Henderson believes “seven successive interest rates are starting to scare a lot of younger recent homeowners“, and some are being forced to sell “because they bought last year and their cash buffers are starting to dwindle, so they’re now willing to take a haircut on the property as they’re worried about meeting the higher repayments”.

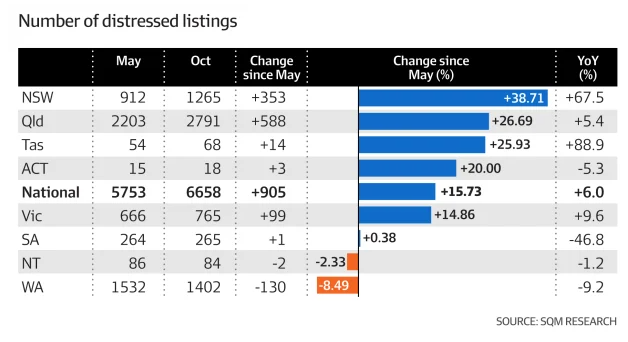

Henderson’s comments come as data from SQM Research shows that the number of distressed property listings has swollen by nearly 40% since May across New South Wales:

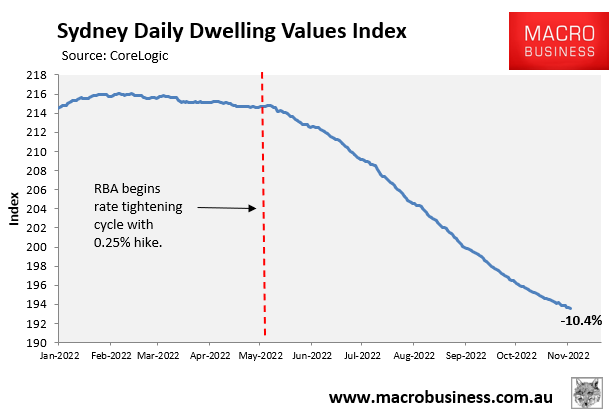

Sydney house prices have also fallen 10.4% from their peak, with almost all of this decline occurring since the Reserve Bank of Australia (RBA) first commenced its monetary tightening in May:

Distressed sales are certain to rise for two key reasons.

First, the RBA is expected to increase interest rates further over the months ahead, which will increase mortgage repayments and push house prices lower.

Second, a large chunk of Australian borrowers that took out cheap fixed rate mortgages over the pandemic are yet to feel the impacts of the RBA’s rate hikes.

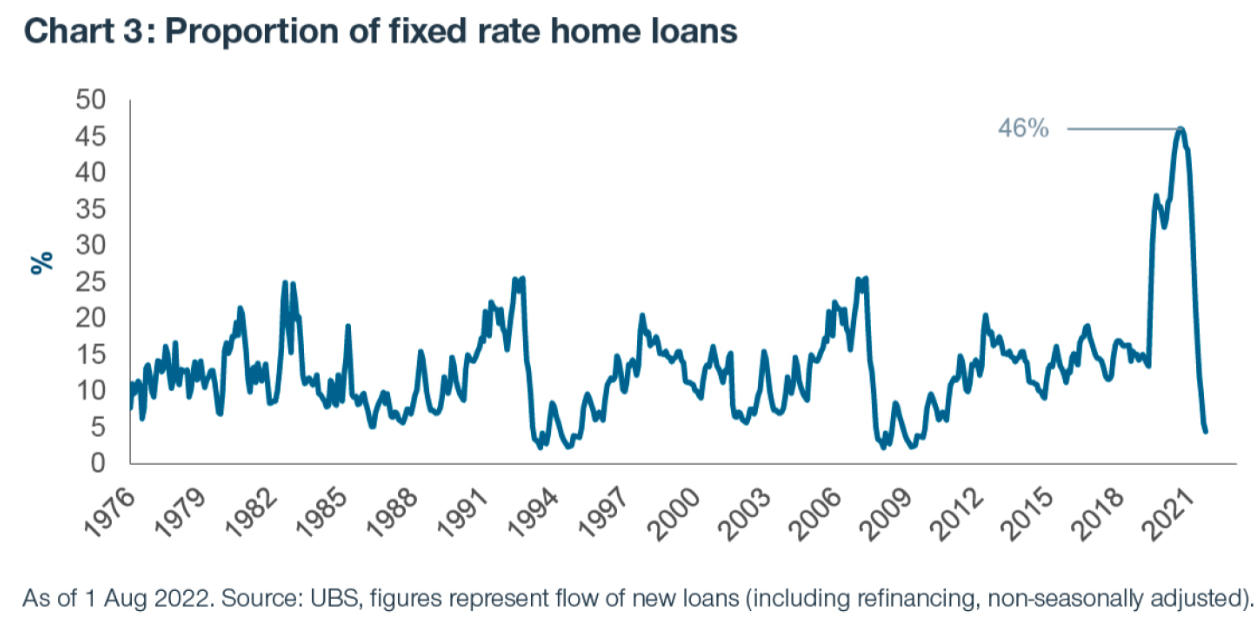

As the below chart from Randal Jenneke shows, “fixed-rate mortgages ballooned from 15% pre-COVID to 46% of new lending at its peak”:

“This translates to an enormous wave of mortgages that will transition to variable rates in 2023. The average fixed rate of roughly 2% will move to a rude variable rate of 6.5% at current forecasts”, according to Jenneke.

The impending fixed rate mortgage reset is another reason why the RBA won’t need to lift rates as hard to dampen demand. There is already significant monetary tightening in the pipeline that will hit early next year as cheap fixed rate mortgages reset.