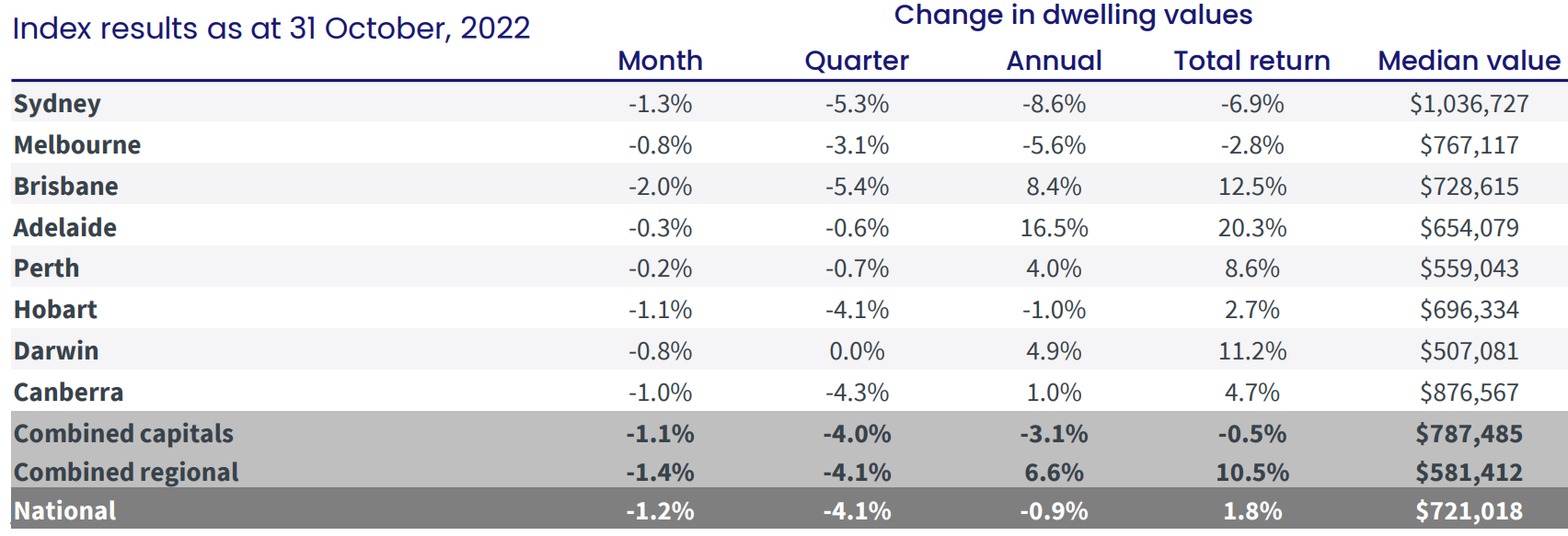

CoreLogic’s dwelling values index fell another 1.2% in October – the sixth consecutive monthly decline:

As shown above, losses were broad based with every capital city and the combined regions experiencing value losses in October, and every region other than Darwin (no change) also losing value over the quarter.

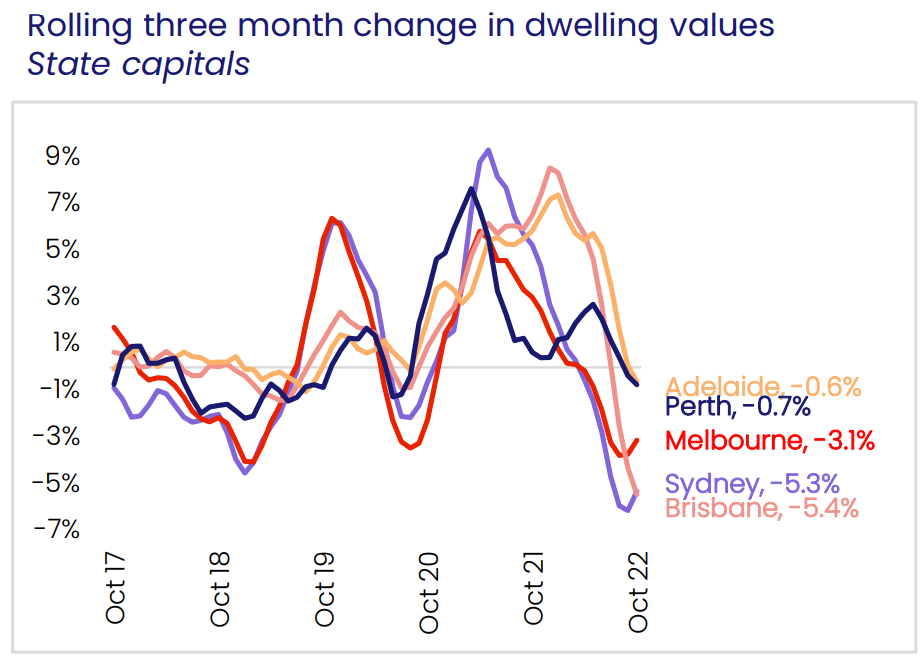

The next chart plots quarterly growth across the five major capital cities. As you can see, the rate of decline has bottomed in Melbourne and Sydney but has accelerated across the other capitals. Brisbane has also taken the mantle of fastest falling housing market:

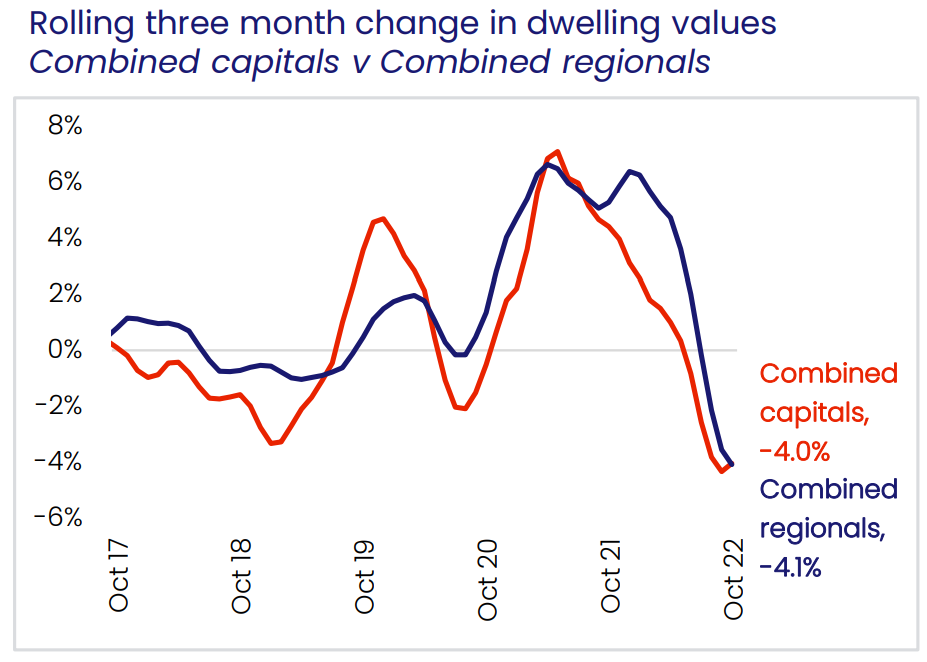

The combined regions are now also falling faster than the combined capital cities:

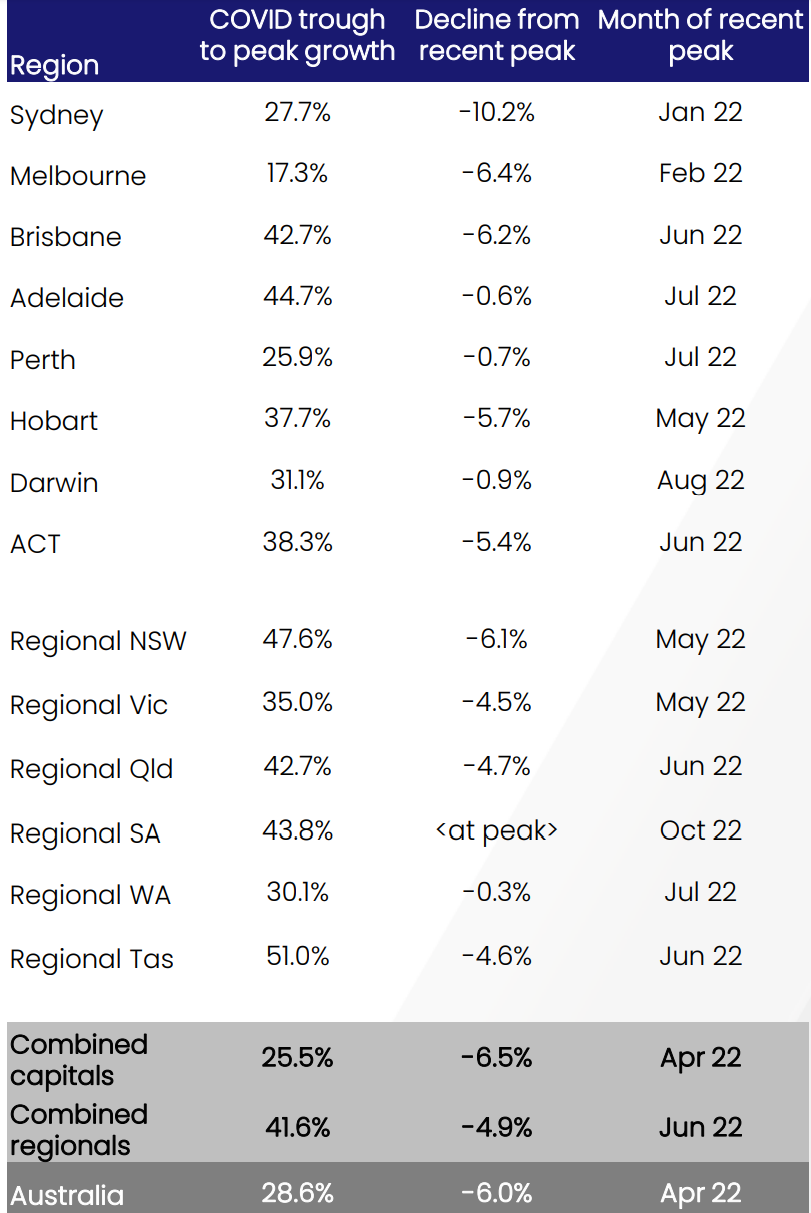

The declines from peak are presented below. As you can see, the ‘big three’ – Sydney (-10.2%), Melbourne (-6.4%) and Brisbane (-6.2%) – are leading the downturn, whereas South Australia, Western Australia and the Northern Territory are holding up well:

Commenting on the results, CoreLogic Research Director Tim Lawless noted that further price falls are likely due to the “double whammy” of rising inflation and interest rates:

Despite the easing in the pace of decline, with Australian borrowers facing the double whammy of further interest rate hikes along with persistently high and rising inflation, there is a genuine risk we could see the rate of decline re-accelerate as interest rates rise further and household balance sheets become more thinly stretched…

Housing values are likely to continue trending lower until interest rates find a ceiling. The bad news for home owners is most economists have recently revised their cash rate forecasts upwards due to higher than expected inflation outcomes. Mainstream forecasts for the terminal cash rate range from 3.1% to 3.85%, while financial markets are pricing in a peak cash rate closer to 4%.

At the low end of these forecasts, a 3.1% cash rate implies an average variable owner occupier mortgage rate of around 5.21% for new borrowers and 5.69% for existing borrowers, adding approximately $1,195 to $1,420 a month to mortgage repayments relative to pre-rate hike mortgage costs on a $750,000 principal and interest loan on a 30-year term.

Later today, the Reserve Bank of Australia is widely expected to lift the official cash rate by at least 0.25%, with further rate rises likely.

As long as the RBA keeps hiking rates, dwelling values will continue to fall.