Terry McCrann has penned another article deriding the Reserve Bank of Australia (RBA) for being too timid with interest rate hikes, claiming it should follow the Reserve Bank of New Zealand’s (RBNZ) bold increase in its official cash rate (OCR) to 4.25%.

McCrann claims that allowing inflation to remain above the target range for too long would heighten the risk of a wage-price spiral. And increasing wages in line with the inflation rate would inevitably result in large-scale job losses and further boost inflation.

He also claims that current interest rate settings in Australia are “highly stimulatory”.

From the Herald-Sun:

Lowe’s warning was all about future wage rises; cautioning against the disaster that would unfold if workers and unions now chased – and got – the 7-8 per cent wage rises that would ‘catch-up’ with current inflation.

That was the disastrous devastating lesson of the 1970s and 1980s… the biggest losers, the real victims, of a ’successful’ wages-chasing-inflation spiral, would be the very workers who might seem to win by getting those wages rises…

The longer Lowe ‘allows’ inflation to stay in the 4-6 per cent range – or, far, far worse, in the 6-8 per cent range, if not indeed even higher – the greater the risk of unleashing a 6 per cent generalised wages surge across the economy…

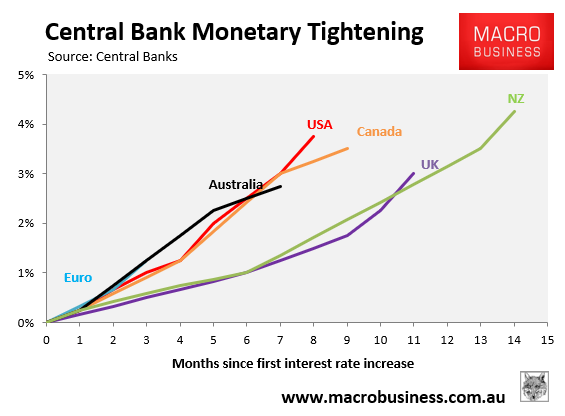

Inflation in NZ is almost exactly the same as Australia -7.2 per cent there, 7.3 per cent here.

The RBNZ has already got its official rate up to, now, 4.25 per cent…

We clearly have a different perception of necessity.

In my judgment 50 points was necessary in both November and December.

That would still have left the RBA’s rate finishing the year at only 3.6 per cent – compared with the RBNZ’s current 4.25 per cent…

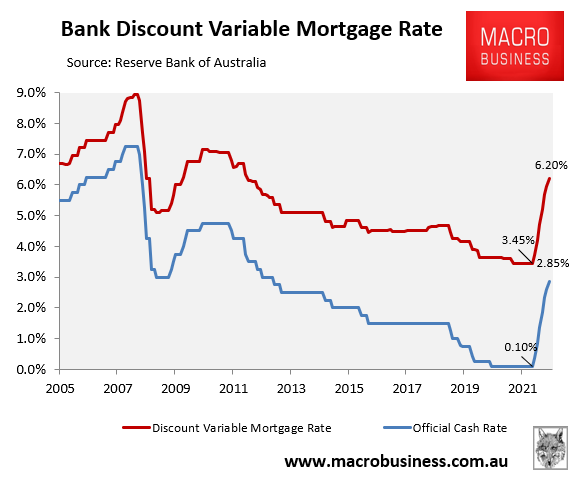

At a negative 4.45 per cent (inflation of 7.3 per cent less the 2.85 per cent) it is still actually highly stimulatory.

Terry McCrann’s analysis misses two fundamental differences between Australia and New Zealand.

First, wage growth in Australia (3.1% in the year to September) is way below inflation (7.3%). Whereas wages are growing faster in New Zealand than inflation (see here).

Second, the overwhelming majority of mortgage holders in Australia are on variable rate mortgages, whereas the opposite is the case in New Zealand where fixed rates dominate. Accordingly, Australians are far more sensitive to interest rate increases.

The claim that Australia’s OCR is “highly stimulatory” is also asinine when the average discount variable mortgage rate (6.2%) is currently double wage growth (3.1%).

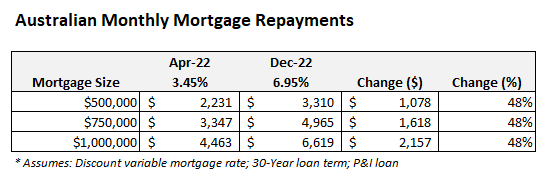

If Australia’s OCR finished the year at 3.6%, as demanded by McCrann, then average mortgage repayments would balloon to 48% above their pre-tightening level, adding $1,078 per month ($13,000 a year) to a $500,000 mortgage:

Terry McCrann is dreaming if he believes households could weather such an extreme lift in mortgage repayments in such a short period of time.

Household consumption would necessarily crash, plunging the economy into a consumer-led recession.

This isn’t the 1970s Terry. Reference to the “negative real rate” without consideration of wage growth and mortgage repayments is insane.