By Gareth Aird, head of Australian economics at CBA:

Key Points:

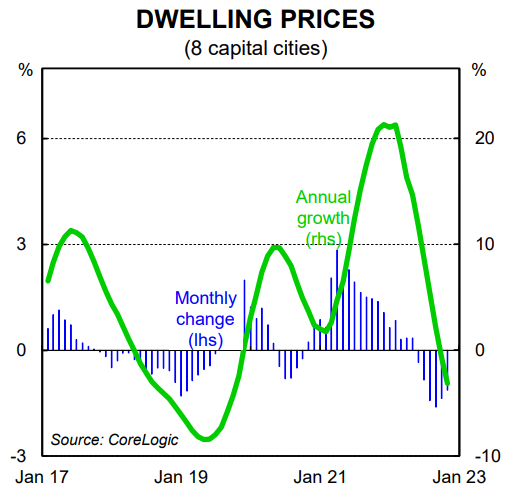

- Dwelling prices fell by 1.1% across the eight capital cities in October. Prices are down by 6.5% from their April 2022 peak.

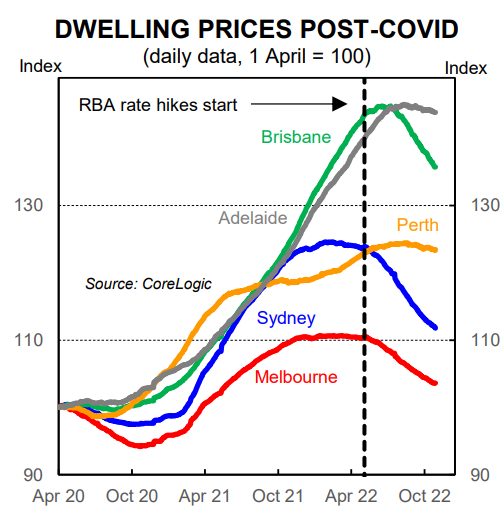

- Prices fell solidly in Sydney, Melbourne and Brisbane. More modest declines were recorded in Adelaide and Perth.

- We continue to expect a national decline in home prices from peak to trough of ~15% (conditional on a 3.10% terminal cash rate, reached in December 2022). But if the RBA continues to hike the cash rate in 2023 a bigger fall would be anticipated.

Home continue to slide quickly across the country

According to CoreLogic, Australian property prices fell for the sixth consecutive month across the eight capital cities in October. The 1.1% decline in the 8 capital city benchmark index over the month followed a 1.4% fall in September. Home prices across the 8 capital cities are now down by 6.5% from their April peak.

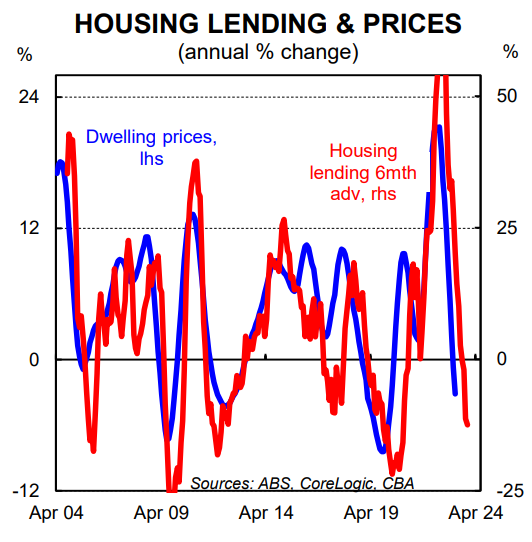

The RBA’s rapid tightening cycle lies at the heart of the fall in home prices. Borrowing power has been greatly reduced by the sharp increase in interest rates. For context, the RBA’s 250bp of already delivered rate hikes has reduced borrowing capacity by ~20%.

Price outcomes are still divergent across the country. But all markets are in contractionary territory, albeit to differing degrees. Dwelling prices fell by 1.3% in Sydney, our largest capital city, in October. Sydney home prices have fallen the most across the capital cities. The cumulative fall since the peak in January 2022 sits at 10.2%. Sydney house prices (as opposed to units) have fallen by 11.3% since

January, which can only be described as a collapse in prices. Some recent borrowers may now be in negative equity.

Large monthly falls in dwelling prices were also posted in Melbourne (-0.8%), Brisbane (-2.0%), Canberra (-1.0%), Hobart (-1.1%) and Darwin (-0.8%). More modest falls were recorded in Adelaide (-0.3%) and Perth (-0.2%).

Prices have weakened significantly across regional Australia. The CoreLogic regional benchmark index fell by 1.4% in October. Home prices in regional Australia are down 4.9% from their June peak (i.e. in just four months).

House prices have fallen by a lot more than unit prices over the past six months. This is a reversal of the trend in 2021 when the prices of detached dwellings rose at a faster pace than units. House prices are down by 7.2% since April while unit prices have fallen by 4.2% over the same period.

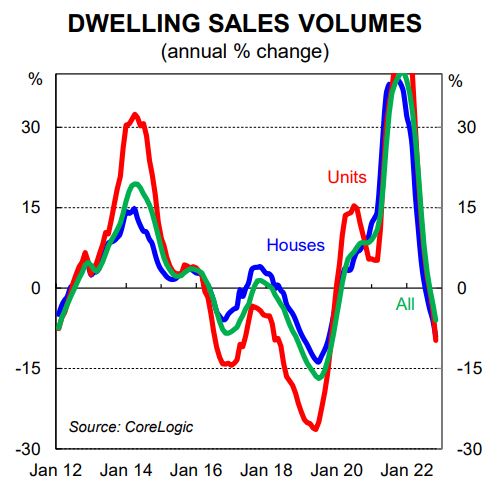

On the supply side CoreLogic notes the flow of new listings picked up in October, but the traditional spring selling season remains well below levels at the same time last year and relative to the previous five year average. Over the four weeks ending 30 October the number of newly listed capital city dwellings was 25.2% below year ago levels and almost 19% below the previous five year average.

On the demand side Corelogic calculate that modelled sales over the three months to October across the capital cities were 16.6% lower than a year ago.

The outlook

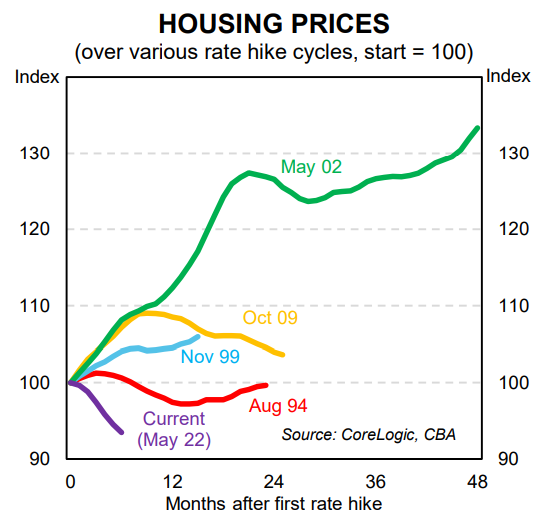

The historical lags between changes in the cash rate and the impact on home prices have shortened over the past five years. The current RBA tightening cycle is a case in point. The peak in home prices nationally was in April 2022. Dwelling prices began their descent as soon as the RBA commenced normalising the cash rate the following month in May.

The rapid pace of RBA tightening has had an almost immediate impact on the demand for credit and by extension home prices (see below chart). The upshot is that national dwelling prices are currently falling at a swift pace. That picture is not anticipated to change in the near term as the RBA continues to raise the cash rate.

The October Board Minutes discussed the impact rate rises were having on the housing market. More specifically, the Minutes noted, “the tightening of monetary policy was having a clear effect in the housing market, where prices had declined after earlier large increases, and the demand for housing loans had also fallen. Previous episodes of lower housing prices and turnover had seen a large effect on consumer spending, in part through the wealth channel of transmission.”

Regular readers will know that this comment from the October Minutes lines up with our analysis previously on the housing market. We stated back in August that, “the RBA does not target dwelling prices and they have made that explicitly clear. But home prices cannot be divorced from the broader economy and changes in home prices influence the economic outlook. Indeed they are a forward looking indicator (changes in home prices impact wealth, consumer confidence, spending decisions and employment). Housing turnover also impacts spending as turnover and consumption are positively correlated. More turnover in the housing market means more spending on household goods, all else equal. The reverse is also true. The RBA will be monitoring activity in the housing market closely for these reasons.”

It is crystal clear that the RBA is now focussed on developments in the housing market. And their tightening cycle from here will determine how much further home prices will fall.

Our central scenario sees home prices fall 15% from their April peak. This means that we expect a further fall in home prices of ~9%. And we expect the trough to be achieved in mid-2023. These forecasts are conditional on a peak in the cash rate of 3.10%, to be reached by the end of 2022. We would anticipate a bigger fall if the RBA continues to lift the cash rate in 2023.