The Market Ear kicks us off.

Summer squeeze set up continues to play out

In mid October we pointed out that the set up was looking very similar to the summer squeeze set up (here and here). We have followed the trajectory well. We are still waiting for SPX to touch the 200 day moving average and make the classical overshoot that forced people in. If we are to “replicate” the squeeze move from summer lows to highs, then the overshoot would play out perfectly (3500*17% = around 4100).

Refinitiv

Can CTAs help us overshoot?

Goldman writes that medium term CTA momentum is back in positive as we are above the 3965 level. They projected “$6b of S&P to buy in flat tape over next 5 trading sessions,l but that number will grow meaningfully post today’s close”. Longer term momentum flips at 4054. They also write: “Another key technical level to keep up on your screens in 200dma of 4062. Would not be surprised if mkt make a run towards 200dma tomorrow but will be difficult to break through it.”

Another 6-7% for SPX?

DB’s excellent Binky Chadha and team were bullish in early October arguing for a bear market rally to occur stating positioning, flow and buybacks as the main drivers. We have come a long way, but Binky writes: “Positioning returning to neutral should see the S&P 500 up by 6 to 7%.”

More support for the squeeze

Binky points out that:

1. Flows have been resilient and that we are entering strong seasonality for flows

2. Buybacks remains very strong

3. Macro has been positive

4. Inflation surprises have been huge positives “Looking ahead, implied vol for CPI and FOMC days in December is significantly lower than over the last 2 months, but rising.

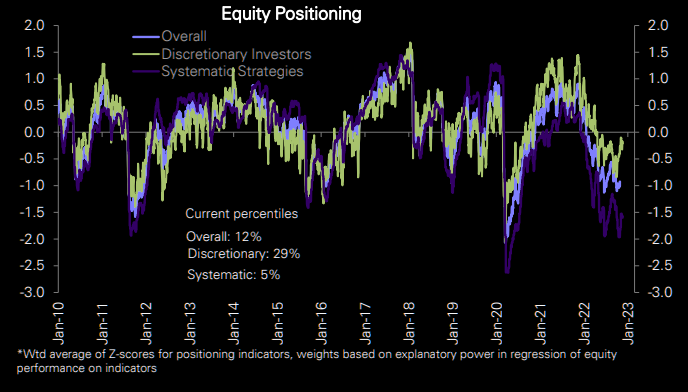

Chart shows that there are still a lot of strategies running “depressed” equity exposure.

DB

The gap to discuss over the long weekend

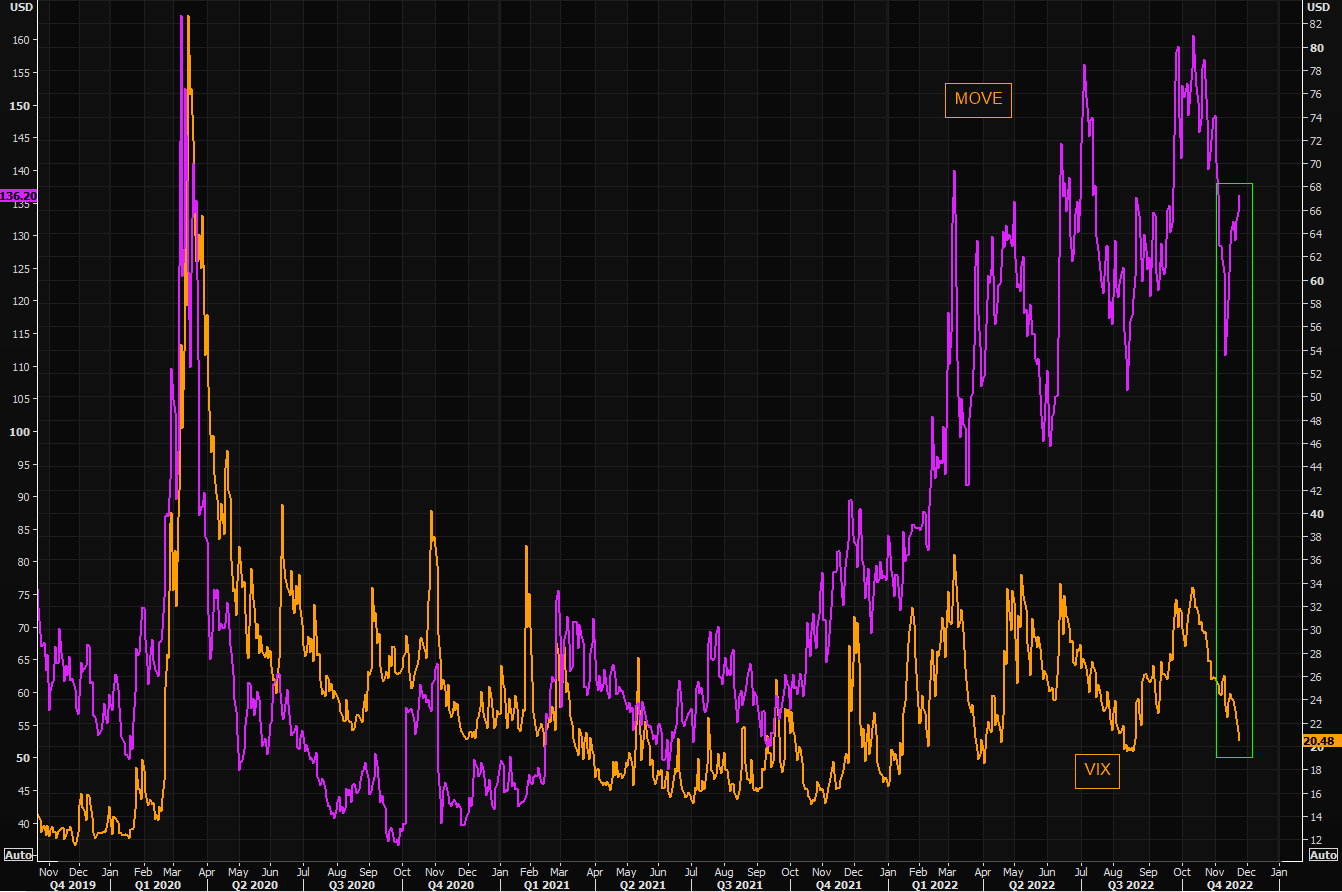

Bond volatility, MOVE, vs VIX is very wide (again)…

Refinitiv

Buybacks bonanza coming to an end…

Sort of at least. Corporate buybacks have been the largest and most consistent source of demand for shares for more than 10 years but Goldman has been saying that demand will soften in 2023. GS: “Repurchases are primarily a function of EPS growth and authorizations. Year/year growth in S&P 500 buyback completions has decelerated from +100% in 4Q 2021 to just +7% in 2Q 2022 and registered -10% in 3Q. In our baseline soft landing scenario, we forecast S&P 500 firms in 2023 will spend $869 billion on repurchasing shares, a year/year decline of 10%.” (Goldman)

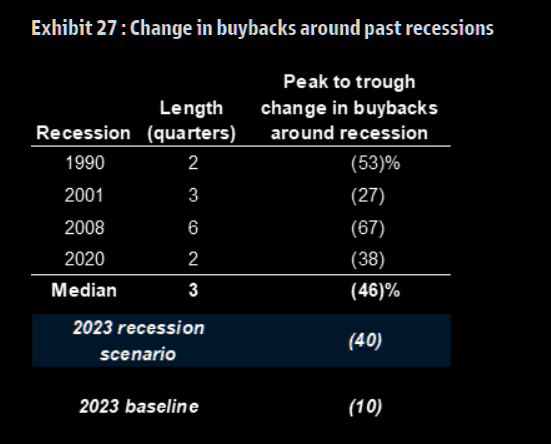

Buybacks in a recession

“While the prospect of a recession will likely weigh on cash spending, a realized recession poses even greater downside risk to our estimates. Our forecast for an 11% decline in earnings in a recession would lead to a broad-based slowdown in cash spending. In the four recessions since 1990, buybacks typically fell by 46%. In a hard landing scenario we expect cash spend on buybacks would drop by 40%” (GS). Now what about in a depression….?

Goldman

Oil’s disinflation

The “smart” crowd are still only talking bullish narratives in oil, despite black gold being down some 33% from highs in Q2 this year, but these people do not trade. Anyway, let’s see where we go from here, but the US 10 year breakven connection remains intact…

Refinitiv

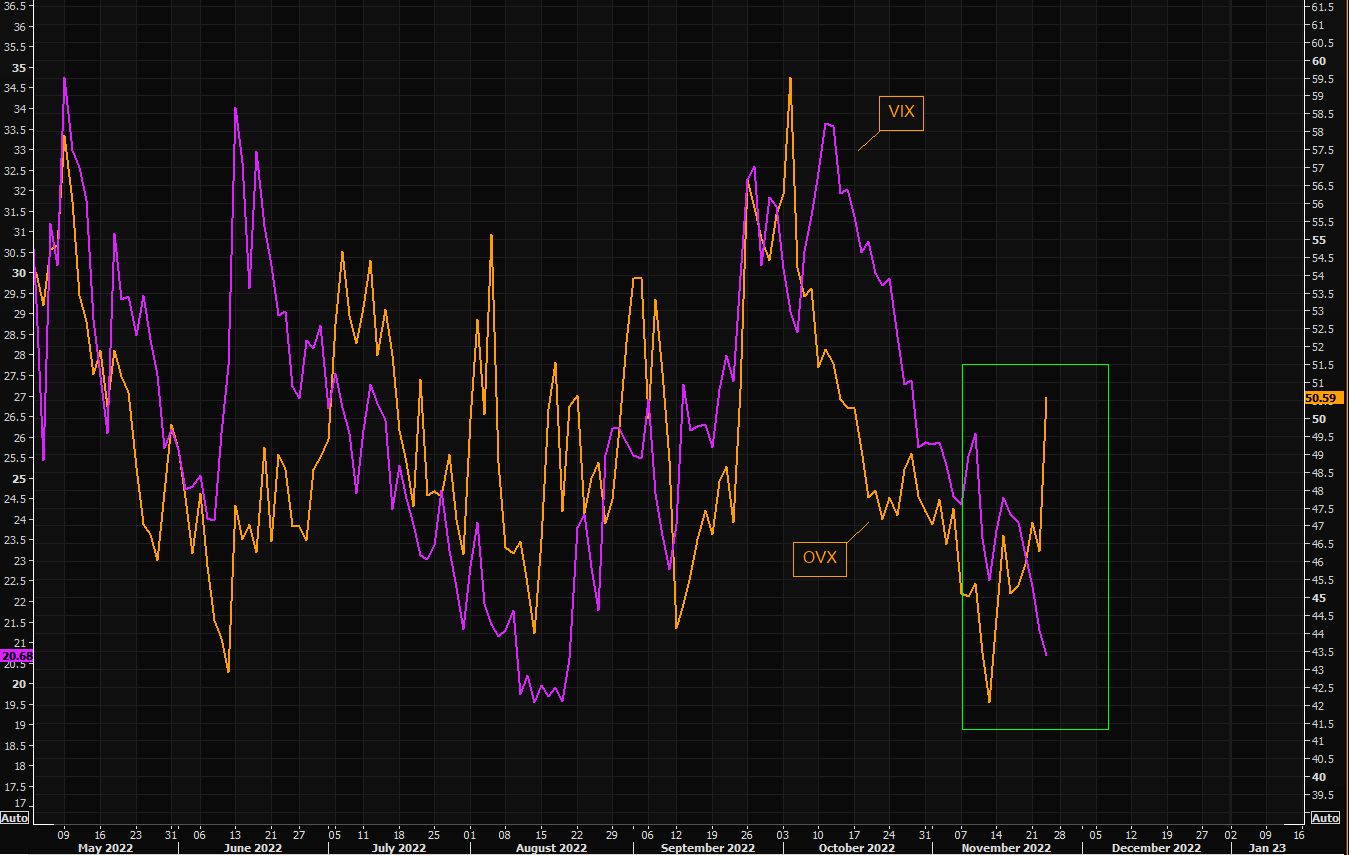

Oil’s VIX not overly chilled

OVX is moving sharply to the upside, trading at levels not seen since mid October. Back then VIX was at 32/33. We are not saying VIX must trade to that level just because OVX is spiking, but oil is a big part of the global puzzle, so watch oil volatility closely.

Refinitiv

Nomura’s excellent Charlie McElligott sums it up well.

The bottom-line—both in Fixed-Income as well as Equities—is that discretionary Macro – types who have done exceptionally well playing “FCI Tightening” trend trades throughout 2022, are now in process of unwinding those positions and pivoting into “reversal” trades for next year, particularly on said Fed policy inflection views.

…Ultimately, this building “stability” can and will breed “instability,” as excess surge in $Delta and / or unemotional & uneconomical Mechanical positioning becomes crowded and can then poses asymmetrical risk of “tipping over” into fresh macro catalysts (new hawkish CB catalyst, upside surprises in inflation / growth data,energy price escalation, external shock)….but we are not there yet.

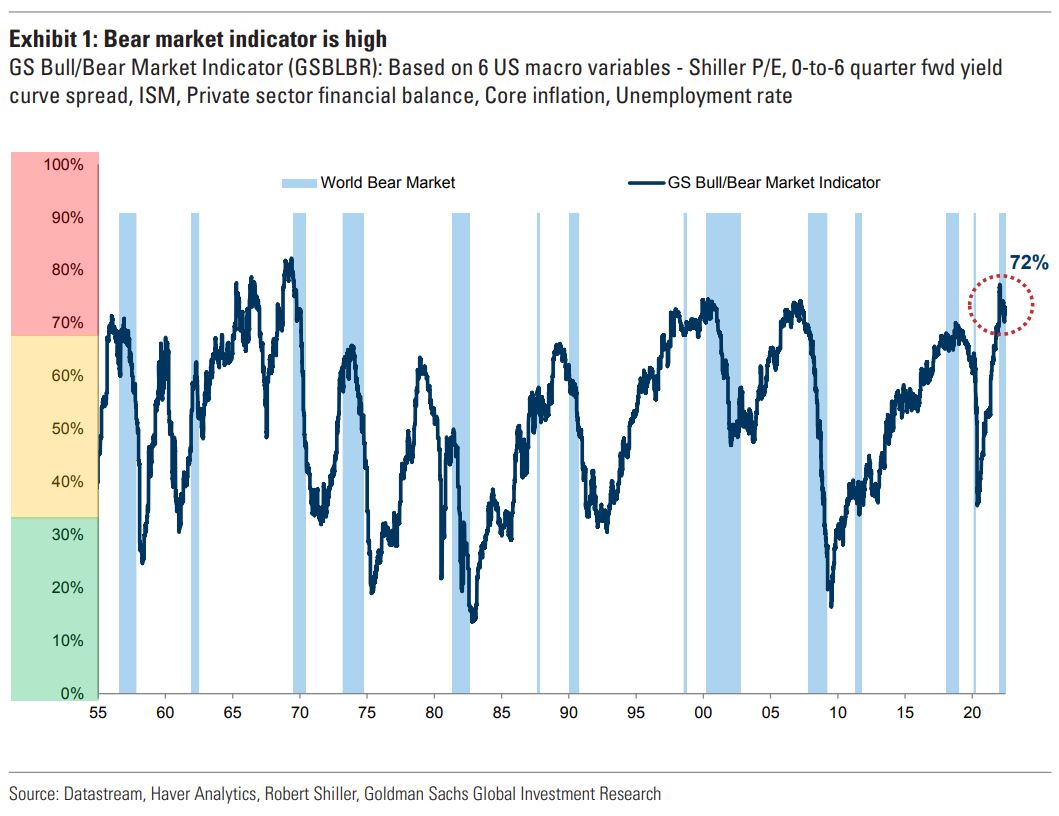

Finally, Goldman chimes in with some uncharacteristically realistic analysis of bear markets.

Most major equity markets have now moved into official bear market territory. The damage beneath the surface has reflected the shift higher in the cost of capital (with long duration stocks being hit most) and recession risks (with many cyclicals underperforming defensives).

There are now two critical issues for investors; First, how much further can equities adjust before the trough and second what kind of characteristics will the new cycle exhibit.

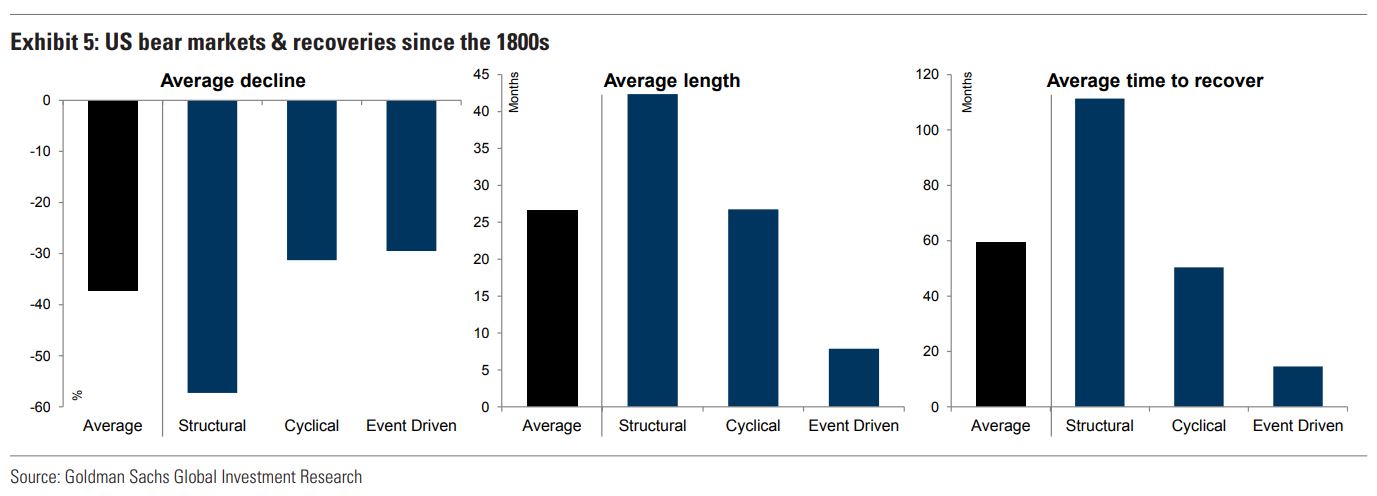

We looked at Bear markets back to the 1900s and divided them into three types – Structural, Cyclical and Event-driven – we look at the average performance and duration for each Bear market. We view this as a ‘cyclical’ bear market with stronger private sector balance sheets and negative real interest rates cushioning against many of the systemic risks associated with the longer and deeper ‘structural’ bear markets.

On average cyclical bear markets are down 30% peak to trough and last two years – in terms of performance we are getting close to this kind of sell-off but the duration is so far shorter.

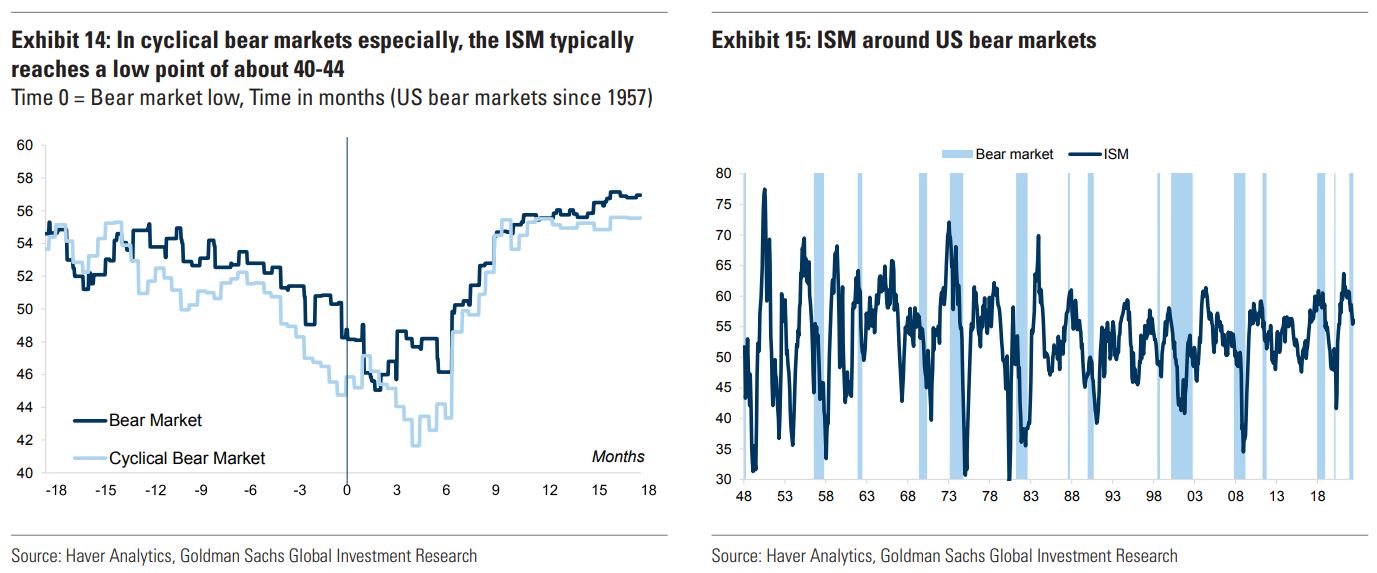

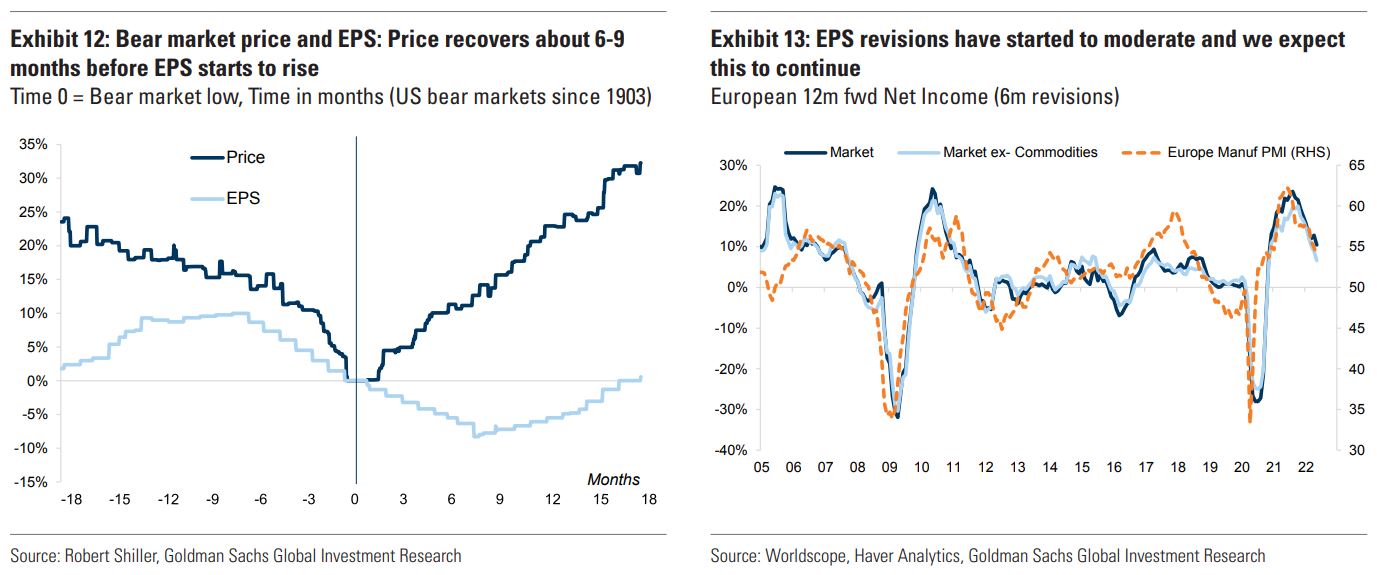

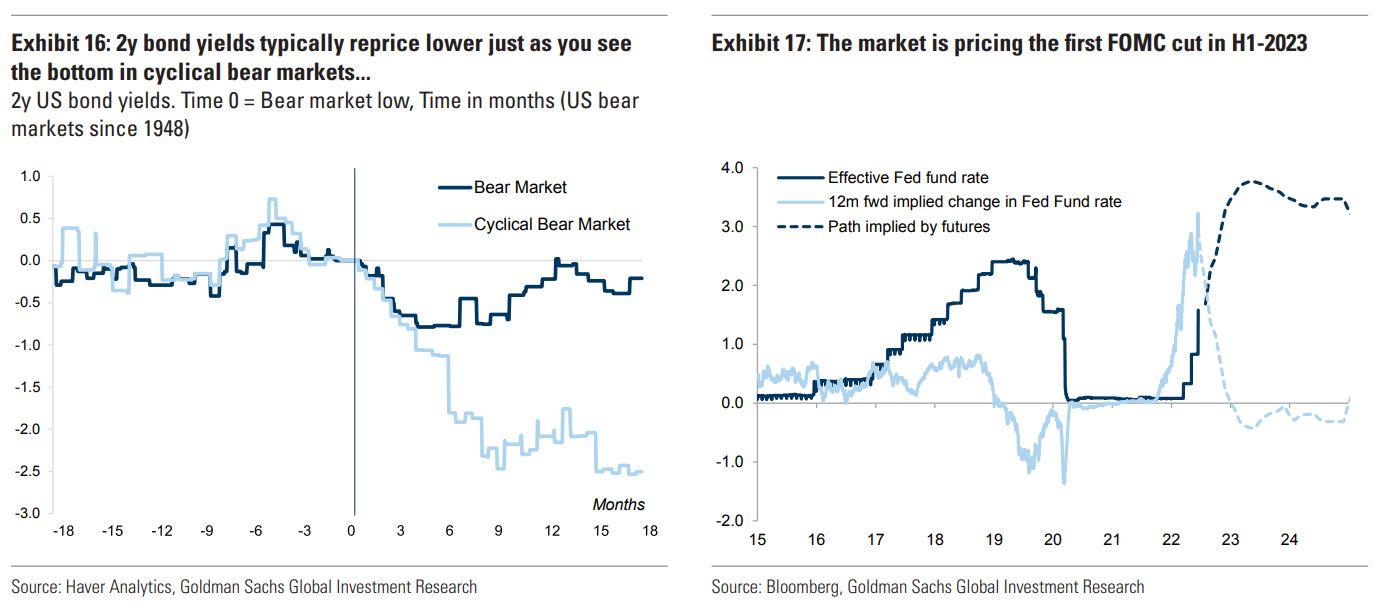

We find the trough in a cyclical bear market typically comes around 6-9 months before the trough in EPS, and 1-2 quarters before the economic nadir post the peak in inflation. The turning point is often around the period when rate expectations start to moderate.

From a valuation perspective, while there has been a considerable de-rating, and some markets are trading below average valuations, pricing is more consistent with a mild recession than an average or deep recession, leaving them exposed to a further deterioration in expectations.

In addition, virtually every recession in the last 30 years has been a function of a demand shock but this is a supply shock. This means that monetary policy is less potent, requiring more fiscal intervention, and this is especially worrisome at a time when BYs are rising and debt/GDP ratios are high.

Hint: there’s no Fed rate cuts coming in H1 or H2, 2023 unless there’s a recession that is not yet priced into equities…