Chris Joye has cross-referenced the looming fixed-rate mortgage reset with RMBS data on discretionary spending budgets and the outcome is shocking. Joy finds that:

More than half of all borrowers will see their discretionary budgets fall 20-100%.

23% of all borrowers will see discretionary budgets plunge 60-100% and around one-third by 40-100%

15% will have negative discretionary cash flow and be in danger of default.

I know I’m going to be one of those with a huge hole in discretionary spending.

Here is how the RBA put it:

Advertisement

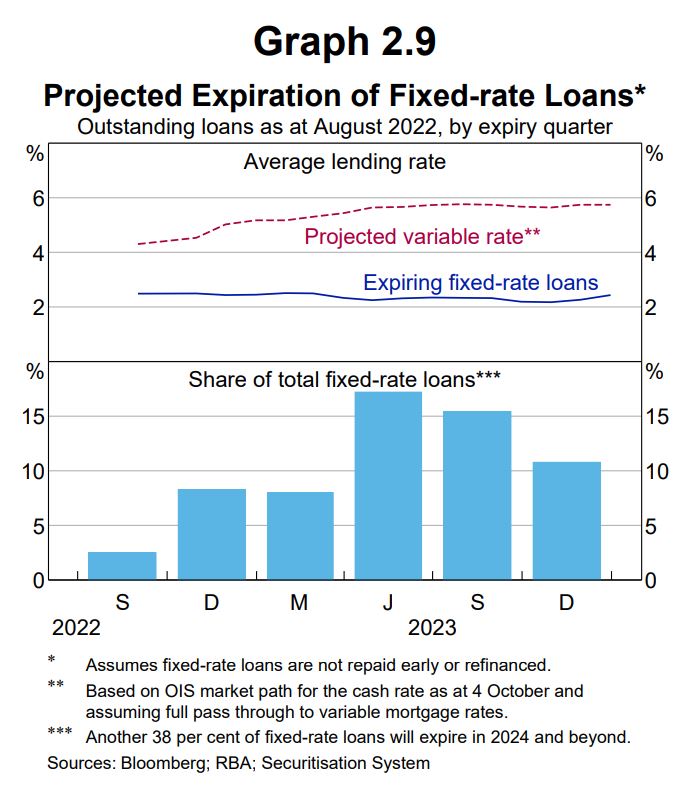

Many fixed-rate borrowers will face a large increase in their payments when their fixed terms expire

Around 35 per cent of outstanding housing credit is on fixed-rate terms (including the fixed component of split loans, which have become increasingly popular in recent years). Around two-thirds of these loans are due to expire by the end of 2023 (Graph 2.9). Based on current grown forward to the September 2022 quarter using WPI (including forecasts). Excludes split loans. ** Relative to the start of the monetary policy tightening cycle. *** As at April 2022 (prior to tightening cycle). Sources: ABS; RBA; Securitisation System market pricing for the cash rate and assuming full pass-through to variable mortgage rates, most fixed-rate borrowers with loans expiring in 2023 will face discrete increases in their interest rates of 3–4 percentage points when they roll over to variable rates, depending on their current rate and the timing of their fixed loan term expiry.

If interest rates were to rise by a cumulative 3½ percentage points from the beginning of the current tightening cycle to the end of 2023, almost 60 per cent of borrowers with fixed-rate loans would face an increase in their minimum payments of at least 40 per cent when they expire (Graph 2.10). In this situation, just over one-third of fixed-rate borrowers will not experience any increases in their minimum payments by the end of 2023, mostly because they have loans that are due to expire in 2024 and beyond.

It is important to note that this is not necessarily a house prices issue unless Joye’s 15% of folks with negative cash flow begin to default. That’s a wagyu and shiraz question.

But, it is clearly a large economic shock given the consumer is 55% of the economy and half will retrench meaningfully in 2023.

Household expenditure is typically a 55-45% staples vs discretionary split. So, if we make the conservative estimate that affected mortgage holders will cut discretionary budgets by an average of 20% then the blow to consumption for 2023 is in the realms of 2.5% of GDP. If the cut in spending is 30% then it is 4% of GDP.

Advertisement

This is why the RBA is not going to hike for much longer.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.