This time TSLombard.

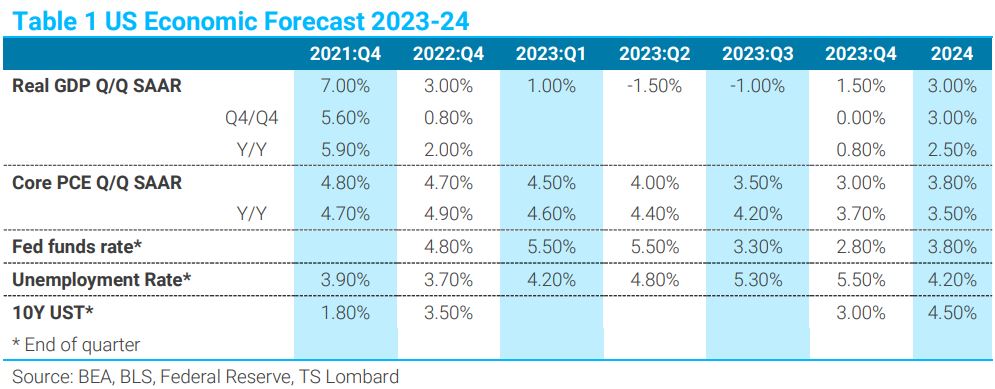

Most things that economists consider as talismans to foretell the cycle now point to the economy sliding into a recession by mid-23. I expect the same. My forecast is 0% real growth in 2023, Q4/Q4 (0.8% Y/Y), core PCE inflation drops to 3.0% Q/Q SAAR by Q4 next year from 4.7% Q/Q in the current quarter, and the unemployment rate peaks at 5.5% in a year’s time (See Table 1). Once recession does hit and unemployment rises, the Fed will be a lot quicker to ease than what the market has priced. If my economic forecast is right, the funds rate will be back below 3% in a year’s time. While my forecast is, in my view, the high probability outcome, the probability is not as high as it was, the risk, in my view, lies to the upside (no recession, higher inflation) and therein lies the tale.

In forecasting a 2023 recession a year ago, I thought getting to a 4.0% funds rate would be enough to damage equities and the tradable goods sector sufficiently to put in play dynamics for a mild recession in mid-23. Inflation, however, stayed higher for longer that I had thought, and this undercut the negative impact of a 4% funds rate — the economy looks to be reaccelerating to above trend growth (3.0% in the current quarter, Q/Q SAAR). All those who have spent the year focusing on what would break, including the FOMC doves, now with r** codified into their thinking as they wait for “cumulative effects” to emerge, are ignoring a critical fact– money is still cheap, and this underpins the economy’s resilience.