The thing is, Australia has a very basic economic model.

We earn income by digging dirt and shipping it offshore. We leverage that income in global markets and our banks tip that borrowing into huge mortgages. The resulting asset inflation supports overspending in a giant edifice of service industry fluff.

The whole mechanism is highly leveraged but surprisingly robust so long as:

- Dirt income keeps flowing.

- Government guarantees the offshore borrowing.

- Mass immigration controls wages.

- Interest rates keep falling ad infinitum.

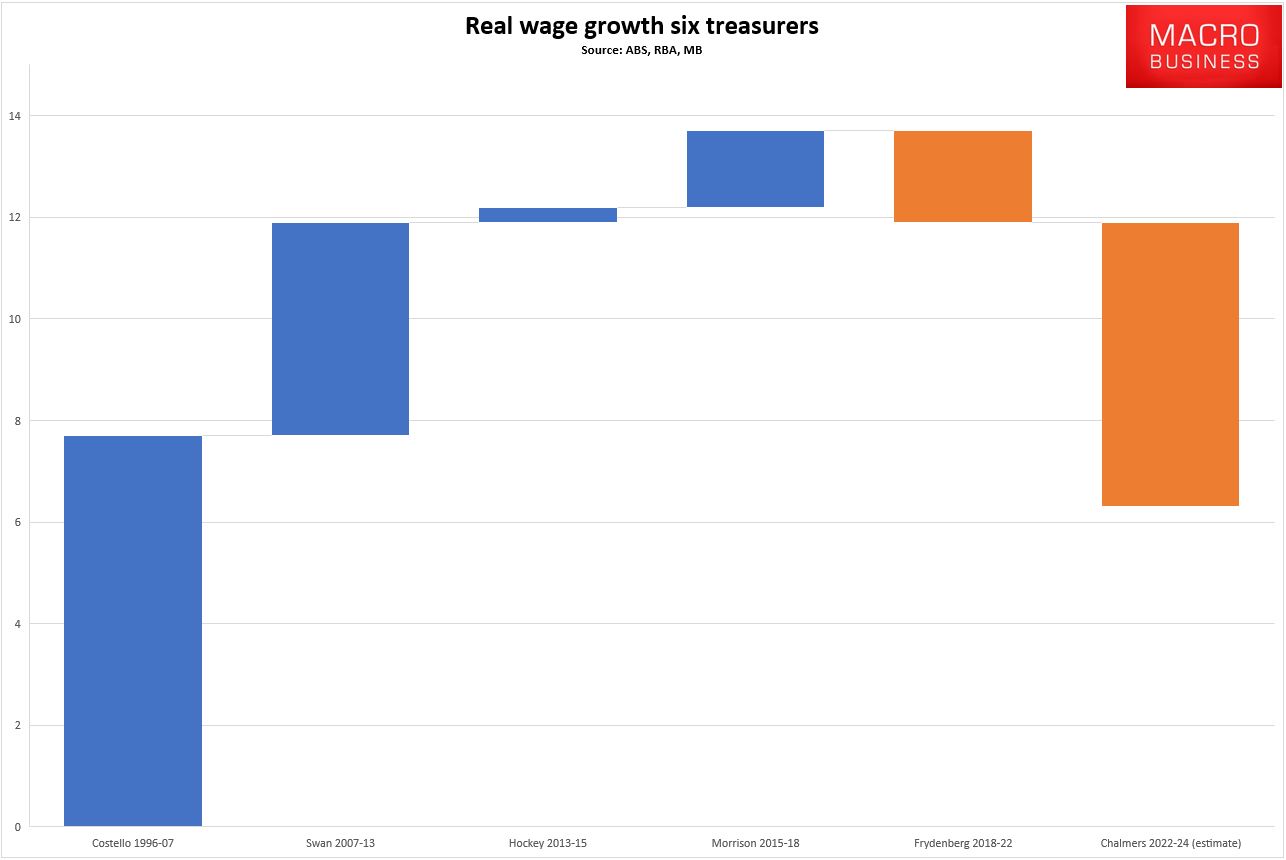

We all know that the RBA is a little challenged right now, but the third leg of the stool, mass immigration, will destroy wages again in due course.

What is less understood is what happens to the mechanism when dirt income flow reverses. As rapacious foreign energy cartels siphon off economic rents, they are taken directly out of the budget (higher taxes), investment and bill shock (lower real wages) and stocks (lower wealth).

Leading to this:

Potential home buyers have had their budgets cut by as much as $100,000 as banks reassess their rising cost of living.

Families are the hardest hit as they have more essential costs, which account for the majority of inflation pressures, and fewer ways of cutting back on non-discretionary spending.

That’s because the Household Expenditure Measure, a tool used by lenders to estimate a borrower’s living expenses as a benchmark against their reported spending, has been increased twice this year. Lenders may reduce the amount of money they offer to borrowers who have higher expenses compared to their income.

It is expected to rise again this year as it is closely tied to the Consumer Price Index, which reached 7.3 per cent in the year to September, Australian Bureau of Statistics figures show.

Albo’s energy shock means that the HEM (which is really just the poverty line) is rising fast as real incomes fall at an astonishing rate:

And that means much lower borrowing capacity, lower house prices, and retrenching services spending. One can see the outlines of Michael Pettis’ “inverted balance sheet” economy here.

One of two things needs to happen to restart the Australian economic engine. Either the inflation that is killing household income is cut off through regulation, or the RBA must crash interest rates again as soon as it is able. And probably both.

Otherwise, the mechanism grinds to a halt.