The move towards some form of energy price caps is gathering more steam:

Energy expert Bruce Mountain says a temporary windfall profits tax on the coal and gas sector would be most easily implemented if it took the form of a levy on exports.

The director of the Victoria Energy Policy Centre said the revenue raised should be redirected to consumers through a lump-sum payment, rejecting claims this would undermine the Reserve Bank’s inflation strategy.

He said the intervention would not need to be as far-reaching as Britain’s, where prices have increased five-fold since Russia’s invasion of Ukraine.

Mr Mountain said a simple levy on exports would encourage producers to sell to the local market, reducing the need for complex policies such as domestic price caps.

“They could structure it as a tax on the profits or they could structure it as a type of royalty on the volume exported,” he said.

Moreover, the levy means local prices fall in line with the price benchmark. It is not inflationary.

These ideas are not new. They were used by both the Whitlam and Fraser Governments:

The purpose of this Bill is to enact the Customs:

Tariff alterations introduced into the Parliament on 18 August 1981 by Customs Tariff (Coal Export Duty) Proposals (1981) which formally proposed, with effect from 8 PM on 18 August 1081 , an export duty of $1 per tonne on black coal previously exempt from export duty.

The Customs Tariff (Coal Export Duty) Act 1975 provides for the imposition of export duties on coal exported from Australia. The rates of export duty imposed on coal by this Act are either $3.50 per tonne or $1 per tonne depending on the quality of the coal and certain features of the mining operation.

Previously certain black coals had been exempted from export duty. Most were steaming coals, but in addition there were certain coking coals which because of particular quality aspects, principally high ash content (defined as greater than 12%), could not attract the prices normally paid for coking coals. Pricing for such coals was largely determined by movements in the steaming coal market.

The strengthening of export demand for steaming coal during 1980 and 1981 with the resultant effect on , prices, indicated that there was no longer any reason to differentiate between coking coal and steaming coal in the application of the export duty.

Let’s hope this is the way the government goes. It is clearly the best solution, cutting prices, raising revenue, and fighting inflation.

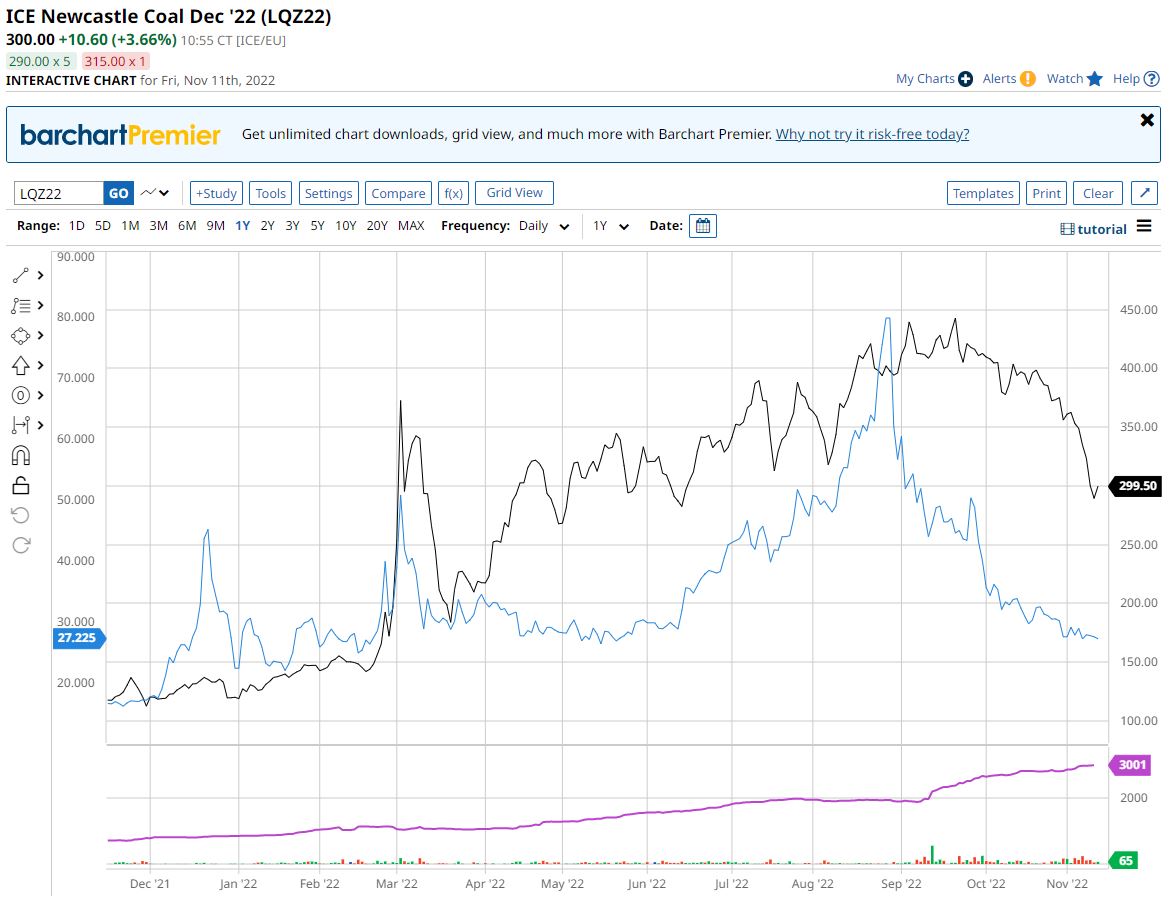

In the meantime, global coal prices bounced with the crazed broader rally but still have a long way to fall back to LNG. Aside from anything else, whatever China does with COVID, it is not going to import more thermal coal regardless as it ramps up local production:

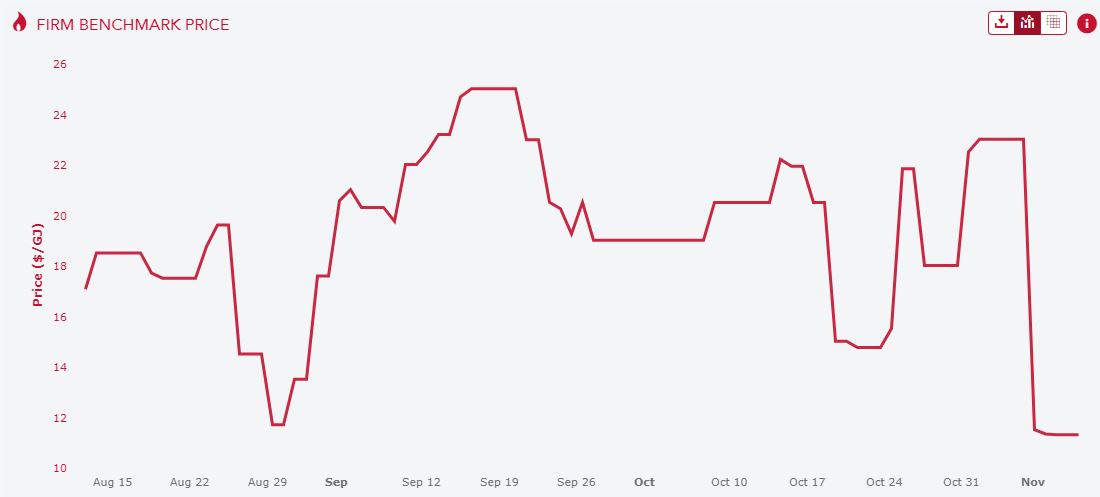

Local gas prices are still sitting much lower at $11.30Gj:

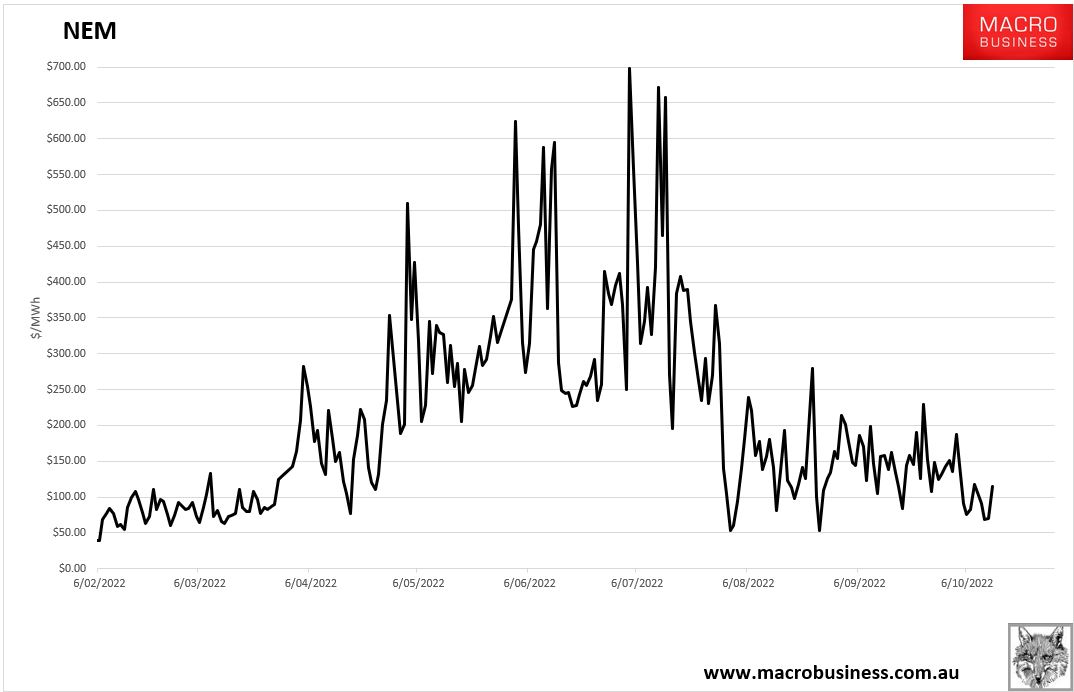

And power prices have come off materially, now running in a $100MWh range which reduces the inflation shock to roughly 30% for utility bills and 1-2% for CPI:

However, electricity futures are still much higher but falling fast (I mistook some ASX IT glitch last week for a new paywall, oops):

There’s good progress but more wood to chop which will hang on the strength of the forthcoming policy measures.

Finally, there’s no sovereign risk here:

The US private equity firm behind a joint $18.4bn takeover bid for Origin Energy expects intervention by Anthony Albanese in the domestic gas market, saying it understands the federal government is under huge pressure to deliver price relief for local users.

EIG – in line to take control of Origin’s stake in the Australia Pacific LNG plant – said it had been slugged with windfall taxes and price caps at its UK and German operations and understood why Australia was likely to follow suit.

“We understand the pressures that Australia is going under and we’re seeing it in really every other market that we operate around the world,” EIG chief executive R. Blair Thomas told The Australian.

“We’re a big producer in the UK’s North Sea, and the UK has introduced a windfall profit tax. You’ve got market intervention in Germany right now. And so this phenomenon is playing out around the world. And it obviously has our attention.”

This transaction cannot go ahead unless the new regime of regulated prices is in place and watertight.