The Chinese data dump yesterday arrived after Xi the Terrible dropped his objections. It’s miracle growth! Pantheon wraps the data.

China: GDP rose 3.9% y/y in Q3, up from 0.4% in Q2. Consensus was 3.3%.

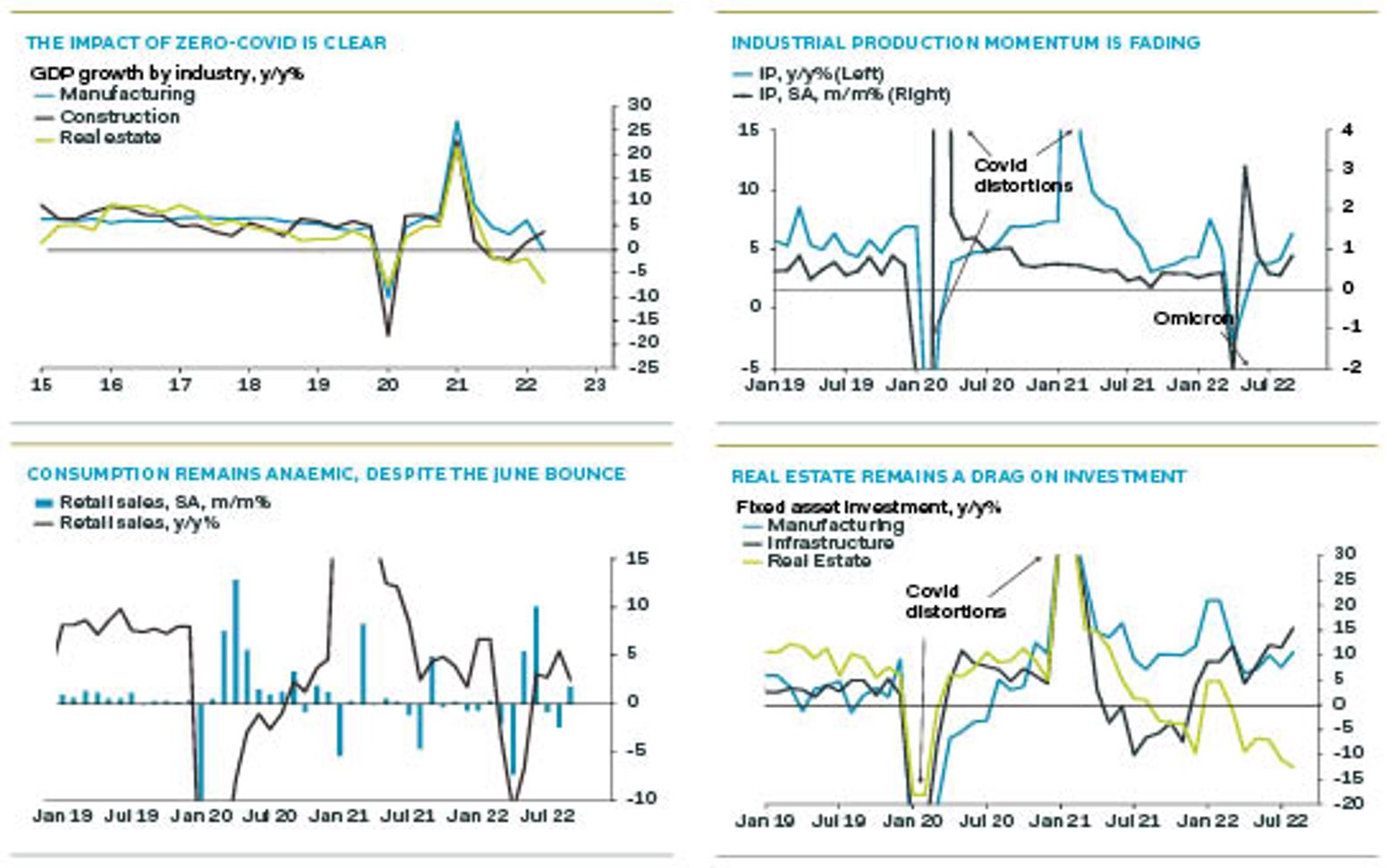

China: Industrial production increased 6.3% in September, up from 4.2% in August. Consensus was 4.8%.

China: Fixed asset investment grew 5.9% in September, up from 5.8% in August. Consensus was 6.0%.

China: Retail sales rose 2.5% in September, down from 5.4% in August. Consensus was 3.0%.

China: New home prices fell 0.28% m/m in September, after 0.29% fall in August. Bloomberg reports no consensus.

China: The trade balance rose to $84.7B in September, from $79.4B in August. Consensus was $80.3B.

China: Exports rose to 5.7% in September, down from 7.1% in August. Consensus was 4.0%.

China: Imports rose 0.3% in September, unchanged from August. Consensus was 0.0%.

China’s GDP rebound stronger than expected

China’s economy enjoyed a reopening bounce in Q3, led by industrial production, construction and services. The industrial sector grew 4.6% in Q3, up from 0.4% in Q2, while services increased 3.2% in Q3, up from -0.4% in Q2. The property sector remained the main drag, falling 4.2% in Q3, moderating from -7.0% decline in Q2.

The prospects of an immediate change in economic policy following the just-finished 20th Party Congress are slim. President Xi Jinping’s work report evinced satisfaction with the results of zero-Covid policy in protecting human lives. The Shanghai Party Secretary Li Qiang was promoted to Politburo Standing Committee and is likely to be the next premier, despite the economic impact of the Q2 lockdown.

Policy support will continue to be focused through infrastructure investment and manufacturing investment, especially by the state sector. The political transition continues until the National People’s Congress in March 2023, when government and state positions are announced. After the transition, officials will be in place for the next five years and more focused on policy implementation rather than promotion prospects. This should mean better policy implementation, though the drags from zero-Covid policy and the property sector will continue as headwinds in H1 2023.

Industrial output boosted by unblocking of supply chains

Manufacturing and mining performed well in September, as they continued to benefited from the reopening and unblocking of supply chains. The improvement in September from August is also owing to the power shortages in August.

Manufacturing grew 6.4% in September, up from 3.1% in August, and the highest figure since February. High-tech manufacturing rose even faster, at 9.3% in September, up from 4.6% in August. This shows the payoff from industrial upgrading policy.

Mining increased 7.2% in September, up from 5.3% in August. This sector benefits from increased construction material demand as a result of infrastructure investment, as well as high prices. Excavator sales grew, by 7.8%, in August, for the first time in 15 months.

The month-to-month seasonally adjusted figures confirm the picture of an improvement in industrial activity in September, with 0.84% m/m growth, up from 0.35% in August. This is still a far cry from 3.1% in May.

Consumption continues to struggle under zero-Covid policy

Retail sales slowed to 2.5% y/y growth in September from 5.4% in August, owing to more lockdowns triggered by further Covid outbreaks. This obvious in the retail sales for catering, which fell 1.7% in September, after rising 8.4% in August. Retail sales for goods fared better with positive, albeit slowing, growth. Goods sales rose 3.0% in September, down from 5.1% in August. Subsidies have continued to drive sales of cars, which rose 19.2% in September, barely slowing from 21.2% in August. Consumer electronics sales benefited from similar support, growing 8.9% in September, up from 0.5% in August.

We expect retail sales to come under pressure. The impact of subsidies is temporary: it brings forward purchases rather than boosting underlying demand. Therefore we expect to see a slowdown in car sale and consumer electronics by year-end at the latest.

More broadly, consumer confidence is weak because of the uncertain economic outlook, falling property prices and the impact of zero-Covid policy. Any shift in zero-Covid policy will be mid-2023 at the earliest. We do not expect any fundamental policy shift towards consumption, beyond the targeted subsidies, at least until the December Central Economic Work Conference.

Property drags down fixed asset investment

Infrastructure investment and, to a degree, manufacturing investment are the main channels of government fiscal stimulus and policy support for the economy. Infrastructure investment grew 15.4% in September, up from 11.5% in August. The State Council has topped up funding for infrastructure by recently adding RMB500B in local government special bond quota and granting policy banks additional lending quota for infrastructure. The policy banks have also creating infrastructure investment funds that can invest in project capital.

Manufacturing investment rose 10.6% in September, up from 7.5% in August. We see this as led by state-owned enterprises, which have better access to capital than private enterprises. State-owned enterprise are more prominent in the upstream commodity-processing sectors that benefit from demand from infrastructure construction. The PBOC has recently rolled out a relending facility for manufacturing equipment and has guided commercial banks to lend to the manufacturing sector.

The property sector continues to struggle. The incremental increase in policy support seen so far has been insufficient to significantly increase home sales or relieve developer liquidity issues. Real estate fixed asset investment fell 12.6% in September, accelerating from 11.0% in August.

We believe this pattern of weak property investment contrasting with strong infrastructure and manufacturing investment will continue in Q4. The State Council will top up funding by as needed, including by starting the 2023 local government special bond quota process this year. This is likely to include allowing issuance of a small part of the quota this year.

Meanwhile, we expect property sector support to be gradually increased rather than a full-scale bail out. This means a drawn out recovery process with only some large cities seeing improvement this year, and better smaller markets starting to turn around in 2023.

Home prices fall more quickly in existing home market

Second-hand home prices continued to fall faster than new prices, with the former better reflecting the underlying market adjustment. Second-hand home prices decreased 0.39% m/m in September, accelerating from 0.35% decline in August. Meanwhile, new home prices dropped 0.28% in September, slightly faster than 0.29% in August.

The impact of mortgage loosening has been more evident in the existing home market, where transactions have picked up in recent months. Homebuyers are shying away from the new housing market, because of concern over project completions. Government policy aims to restart suspended projects, but the scale of funding is relatively limited so far and local governments are expected to take the lead. The outlook is for a drawn-out home market recovery.

China trade balance remains large despite slowing export growth

Exports continued to slow in September, a second month of slower growth after three months of double-digit growth in the reopening bounce period of May to July. Exports slowed to 5.6% y/y in September, from 7.0% in August.

Imports remained very weak, owing to insipid domestic demand, coupled with the impact of zero-Covid policy. Imports fell 0.4% in September, down from -0.2% in August.

The trade balance rose slightly, month-to-month, but was still down from the record levels in June and July. This is a result of sustained export growth, albeit slightly slower, while imports fall.

We expect exports to continue to slow on the back of poorer growth in the global economy, and despite the boost to price competitiveness from renminbi depreciation. Import growth is also expected to remain slow, in the absence of a broader stimulus policy to boost consumption demand.