OPEC cut 2mb/d of output last night. More than half of this is the unfilled quota. JPM says oil is going back to $100. Given we’re already at $93.40 this is hardly a stretch. But, given such an event is delf-defeating versus the tightening Fed I can’t see it lasting.

Global oil consumption only rarely falls and it takes worse than usual recessions to do it. But we can still see large swings in inventory on slowdowns and regional mixes which means prices can still fall significantly.

The just-concluded third quarter closed with Brent crude price averaging $4/bbl below our forecast of $102/bbl from March. For our long-standing 4Q22 price of $100/bbl to realize five key forecasted conditions need to play out:

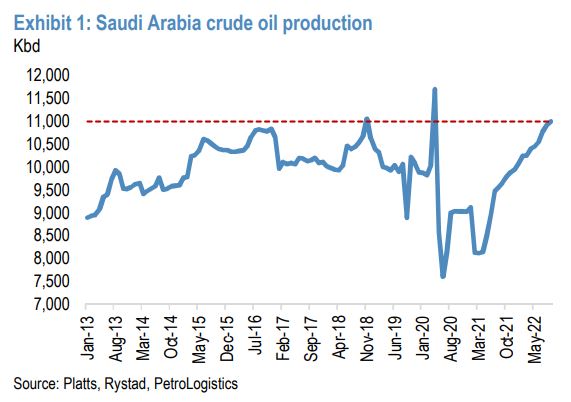

1) demand needs to bounce 0.9 mbd yoy in 4Q, most of that from gas to oil substitution; 2) sanctions on Russia need to constrain supply by 600 kbd; 3) Saudi Arabia production needs to normalize from 11 mbd in September to a sustainable 10.6-10.7 mbd pace; 4) US SPR releases need to end in October or sooner; and 5) the US dollar needs to stabilize. Fundamentally, if four of the above supply-demand conditions materialize, our balances continue to suggest a return to deficits in 4Q22.

As we await final confirmation on OPEC+ production levels, our balance has always implicitly assumed a 0.6 mbd December over September reduction in production, given the unsustainability of recent production prints from key members.

This includes a forecast for Saudi Arabia to normalize its production from 11 mbd in September—a level only exceeded in two months in history—to a more sustainable 10.6-10.7 mbd in 4Q22 and thereafter, allowing the Kingdom to keep some production capacity in reserve.

Meanwhile, traditional opposition from Russia to large cuts seems to be counterbalanced by challenges facing the country’s oil production due to Western sanctions on its energy and financial sector.

Our base line view remains that Russia will try to legally find alternative buyers of its oil on vessels not requiring Western insurance or services. However, the unprecedented mechanism of the price cap and fear of even tighter future sanctions are already creating apprehension among market participants, further limiting the availability of buyers and ships required to move Russian oil.

We believe Russia is at least 1 mbd short of tanker capacity and forecast Russian production falling in December by about 600 kbd below September levels.

The move from OPEC+ could trigger US countermeasures, including the additional releases from the Strategic Petroleum Reserve. For now we assume US SPR releases to end in October with additional 26 mn bbls of congressionally-mandated SPR sales to be delivered in 1Q23 instead of 4Q22.

While the growth path of the global economy remains highly uncertain, ultimately, it would take global GDP growth falling into negative territoryfor global oil demand to contract. Based on the historical GDP to global oil demand beta of 0.5, we estimate that world’s demand will grow 0.9 mbd yoy in 4Q22, to average 101.8 mbd. Inclusive in this growth is the 0.7 mbd increase in gas to oil substitution this winter.