A good piece here from BofA sums up nicely where the Fed is at.

Bill Dudley, former President of the Federal Reserve BankNY, has been a vocal critic of the Fed’s slow response to emerging inflation in the past year and a half. We are quite sympathetic to his views and indeed we wrote pieces with very similar titles—“Is the Fed fighting the last war?”—on the same week last fall. However, we disagree with his latest piece. He asks, “Will Jerome Powell Be Like Volcker or Burns?” And he concludes “So far he is looking more like the latter.” Here we argue:

• From last summer to this summer the Powell Fed was looking uncomfortably Burnslike.

• However, next week the Fed is likely to hike by 75 bp for the fourth meeting in a row—a Volcker-like catching up.

• Today’s inflation is much less embedded than when Volcker took over the Fed in 1979.

You haven’t done nothin’

Dudley correctly points out that “to date, the Fed’s monetary tightening hasn’t done much to reduce inflation pressures or loosen the labor market.” Median inflation continues to move up on a year-over-year basis. Payrolls are rising three times faster than is consistent with a stable unemployment rate. The ratio of job openings to unemployed workers has only dropped from a record 2-to-1 in March, to 1.7 in August, but that is still well above a more normal ratio of 1-to-1. He concludes that “given the lack of progress, one might expect the Fed to take interest rates even higher than previously planned.” Instead the Fed has stuck to its September projection of a “moderately restrictive” peak funds rate of 4.50 to 4.75% and then a flat rates thereafter.

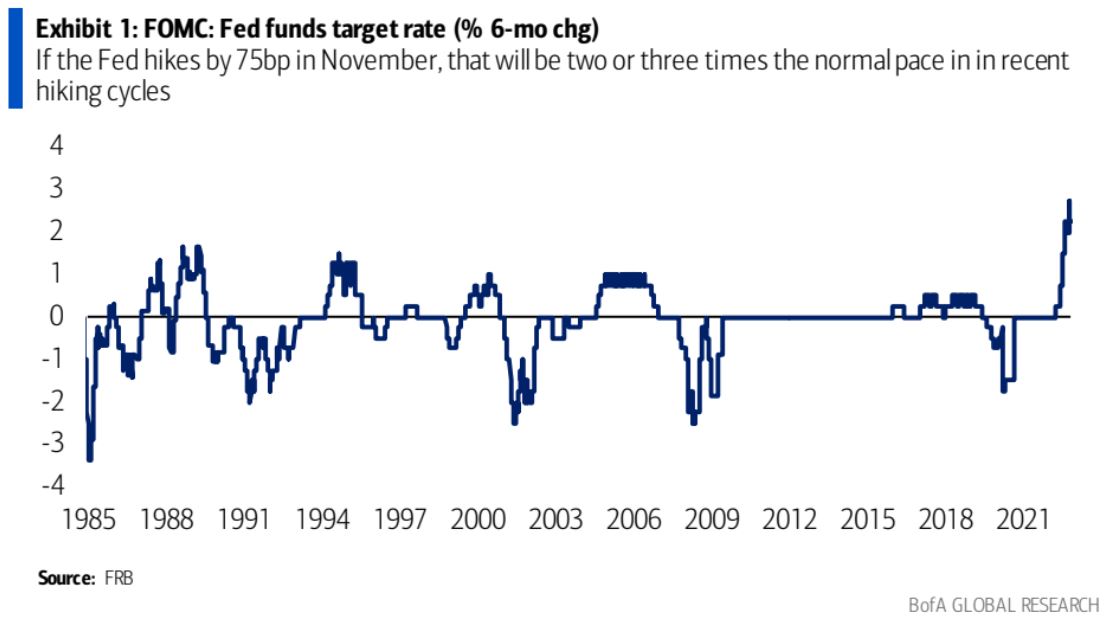

The times they are a-changin’

Stepping back this seems a bit harsh to us in four respects. First, the Fed seems to be learning from its mistake. We have been arguing that the Fed was six months late in starting their hiking cycle. However, the Fed is now moving at a remarkably fast pace. If they hike by 75 bp in November—as we expect—that will be 300 bp of hikes in just four meetings. That is two or three times the normal pace in recent hiking cycles (Exhibit 1).

Second, we think the FOMC’s median forecast of the terminal rate is more of a rough guess than some kind of commitment. The Fed has been steadily revising up its policy

projection in recent quarters. Last December they projected a peak rate of 2.1%, in March that rose to 2.8%, in June to 3.8% and in September to 4.6%. Unless the data turn very quickly we expect the Fed to do at least one more upward revision.

Third, it has been only about four weeks since the Fed met in September. Over that time the progress toward the Fed’s goals has been minimal at best. The only really good news was a sharp drop in job openings in the August release. But four weeks is a very small time frame for another reassessment by the Fed. Monetary policy works with long and variable lags and at some point the Fed will need to slow down.

Mini-Burns should be countered with mini-Volcker

Finally, we don’t see this as a choice between Burns or Volcker. Today’s Fed has made one serious mistake—starting to hike about six months late. By contrast, Burns presided over almost a decade of rising inflation (1970-78). He invented the idea of core inflation and then kept subtracting high-inflation components to prove that inflation was transitory. He was a major advocate of the disastrous wage and price controls of the early 1970s. And he repeatedly tried to deflect blame for high inflation to others—unions, monopolies and so on. His brief successor, G. William Miller was equally ineffective.

It was because Burns and Miller were so late that Volcker had to be so aggressive. By contrast, today a much milder recession should do the trick of getting inflation close to the 2% target. And let’s not forget that even Volcker did not get inflation all the way back to 2%, but backed off with inflation still hanging around 4%. In our view, miniBurns has already transformed into mini-Volcker.