Below is economist Tony Alexander’s analysis of this week’s shock New Zealand inflation result, which saw inflation rise by 7.2% in the year to September – much higher than any market forecasts.

Alexander believes the Reserve Bank of New Zealand (RBNZ) will respond with further aggressive interest rate hikes, which will send mortgage rates higher.

If true, it would present further stiff headwinds for the nation’s housing market, which has already plunged 12.6% from its November 2021 peak.

_____________________________________________________________________________________________

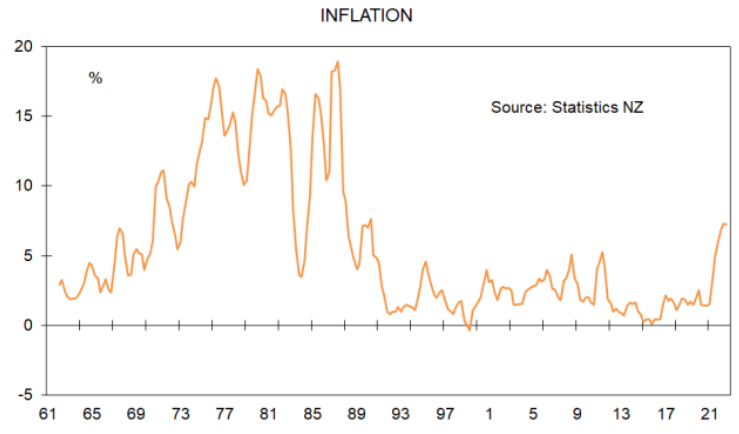

Everyone in the markets on Tuesday morning was primed for the annual inflation rate in the September quarter falling from the June quarter 7.3% down to something near 6.3% – 6.6%. In the event the rate reported was a much higher than expected 7.2%. The fall from 7.3% was within the range of statistical variation and on that basis, one cannot yet say that inflation is on its way down.

On the face of it the result implies a lot further upside for interest rates with monetary policy potentially staying tight for a lot longer than the next 12 months…

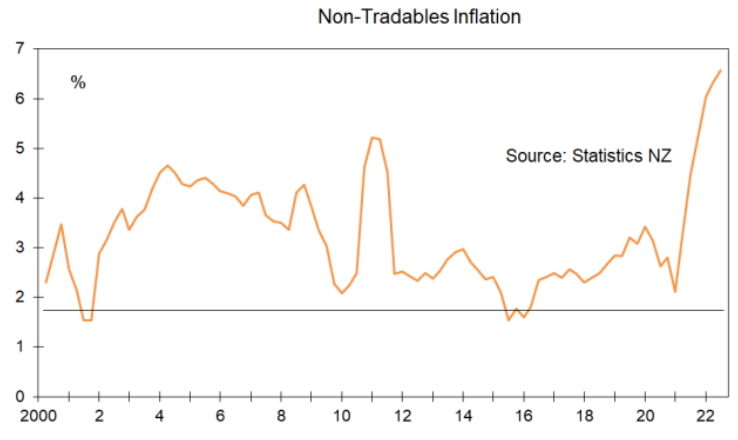

There are various ways of gaining insight into underlying inflation and one of them is to remove items which are imported or have their prices greatly affected by exchange rate moves. These are called tradables. The rate of tradables inflation eased to a horrible 8.1% from a terrible 8.7%. It is too high. But what really matters is non-tradables inflation.

That latter rate did not fall slightly or stay steady as was expected. It lifted from 6.3% to 6.6%. The lift is bad, but the magnitude of the outcome was only 0.3% generally above expectations and not the 0.7% or so error for the headline number.

The Reserve Bank had expected the headline rate to be 6.4% rather than 7.2%. The non-tradables rate they expected to be 6.3% rather than 6.6%.

Another way of measuring underlying inflation is to do what the Americans do and strip out food and household energy. Doing that we see that annual rate lifted from 6.1% to 6.3% with a 2.2% rise in the September quarter from 1.3% in the June quarter. No good news there but not a devastating outcome as suggested by the headline 7.2%.

We can also trim away the top 10% of items rising in price and the top 10% falling in order to get a better grasp of what is happening underlying the fluctuations. Doing that we get annual trimmed inflation rising from 6.6% to 6.9%. Again, not good but again not devastating.

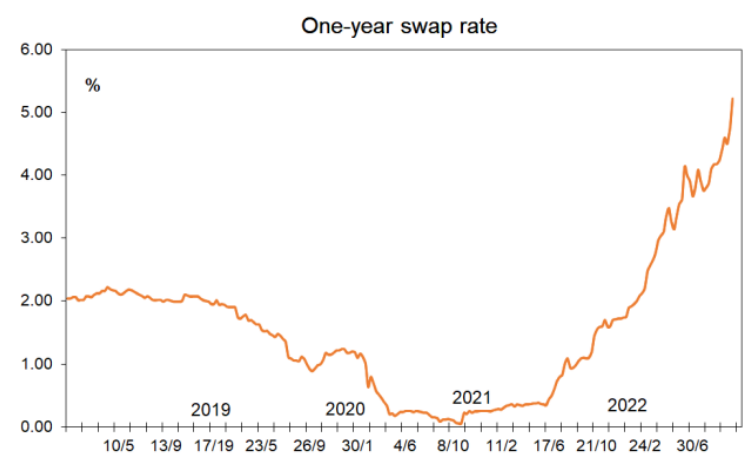

The shock inflation result says that there is more work for the Reserve Bank to do and that means the official cash rate looks set to go higher than thought previously. We can probably lock in a 0.75% rise come the review on November 23 plus some more warning words from the Reserve Bank. A 1% rise is also being talked about…

Because the higher-than-expected inflation number implies wholesale borrowing costs for banks sitting higher than expected, we should anticipate a round of fixed mortgage interest rate rises soon from the major lenders…

There is a round of fixed rate rises happening now… This is because the message from Tuesday’s CPI release was that interest rates need to be higher now than earlier hoped. That means the outlook for the economy has to be worse…