Bond market “more psycho than psychic” on interest rates

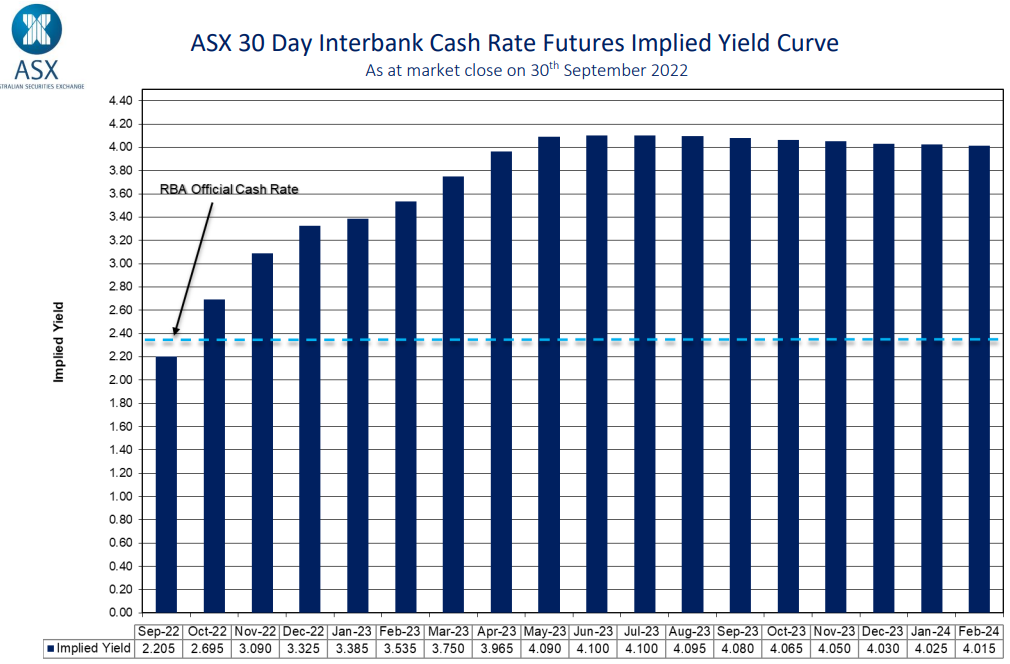

As of close of business Friday, the bond market was tipping that Australia’s official cash rate (OCR) would peak at 4.10% in mid-2023, which is 1.75% above its current level of 2.35%:

Bond market still incredibly bullish on interest rates.

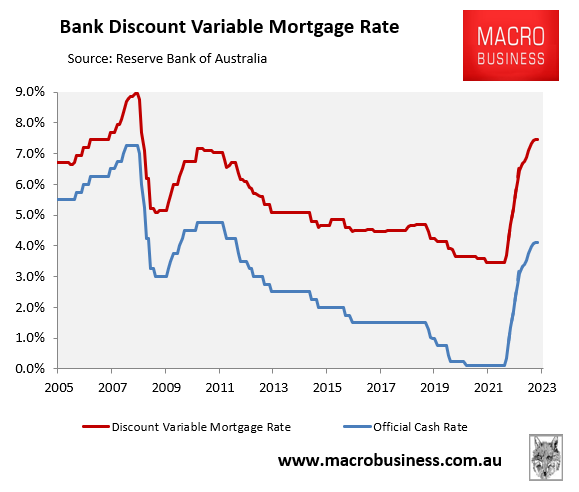

Under the bond market’s OCR forecast, Australia’s average discount variable mortgage rate would climb to 7.45% – well over double the 3.45% that presided immediately before the Reserve Bank of Australia’s (RBA) first rate hike in May, and the highest discount variable mortgage rate since October 2008:

Bond market: highest discount variable mortgage rate since 2008 GFC.

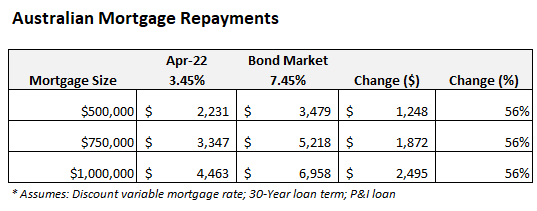

The impact on Australian mortgage holders would be devastating, with average monthly repayments on a typical variable rate mortgage soaring by 56% versus their level immediately before the RBA’s first rate hike:

Australian mortgage repayments to soar under bond market’s OCR forecast.

For a borrower with a $500,000 mortgage, this would represent an increase of $1,248 in monthly repayments – a vicious blow.

I have said from the get-go that I believe the bond market’s OCR forecasts are too hawkish and would push Australia into a painful recession if they came to fruition. This is primarily because household consumption is by far the economy’s strongest driver, and consumption would collapse through the combined impacts of: 1) Australian households having far less disposable income at their disposal; and 2) crashing housing values.

Alan Kohler has given a similar assessment, describing the bond market’s OCR forecast as “more psycho than psychic”, and warning that further aggressive rate hikes from the RBA would “be reckless, heartless and dangerous”. Kohler, therefore, is calling on the RBA to halt rate hikes:

Forecasts for the decline in house prices now range between 20 and 30 per cent, which would be the biggest fall in history…

A 20 per cent fall in values means that hundreds of thousands of families will be living in a house worth less than they paid, for at least five years, possibly 10.

What’s more, many of them will owe more on the house than it is worth, so they’ll have zero equity while scrimping to meet repayments, and worrying about keeping their job…

Is it necessary? In the United States, perhaps, but not in Australia…

In Australia, wage growth is about 3 per cent, half the rise in consumer prices; and inflation here is due to an energy price shock, increased demand from the pandemic cash flood, supply problems and rising profits – not wages.

There are three reasons the RBA has done enough already.

First, as discussed, APRA’s mortgage repayment buffer has been absorbed and house prices have begun their biggest ever crash.

Second, immigration has been rebooted and cheap labour is starting to flood back into the country.

And third, commodity prices have already fallen 20 per cent, including a 35 per cent fall in the oil price, in anticipation of recessions in the US, Europe and China.

The RBA has done enough: It would be reckless, heartless and dangerous to keep raising interest rates.

Hear, hear. Australian wages are growing well below the ~3.5% level the RBA previously nominated as consistent with keeping inflation within the target band over the medium term.

Moreover, the federal government has just launched the largest immigration program in the nation’s history, which will add a huge amount of labour supply next year and crush any prospect of accelerating wage growth.

The RBA should ignore the bond market and focus on the local economy. Because it risks breaking it if it hikes too far too quickly.