Credit Agricole with the argument. Fair enough but it is a temporary state of affairs. All we do is dirt and that has not changed. As well, not all correlation is causation. Australia has bugger all copper and the AUD parallels with equities is a COVID distortions phenomenon that won’t last, either.

Commodity prices impact the Australian economy and the AUD via their influences on net exports, Australia’s basic balance of payments as well as private and public demand. Higher commodity prices can lead to rising levels of mining and energy company investment as well as boost their profits that can be distributed to Australian households via higher dividends or higher wages. Higher mining and energy company profits also add to state and Federal government coffers via increasing royalties and corporate tax revenues.

These channels are clogged a bit at the moment, however. Mining and energy companies are unwilling to undertake significant investment in capacity following the mining investment boom in the early 2000s and in the face of a slowing Chinese economy. The turning away of governments and investors from fossil fuels also discourages investment in capacity. Households and governments would also currently rather save than spend any fillips they receive from larger mining and energy company profits.

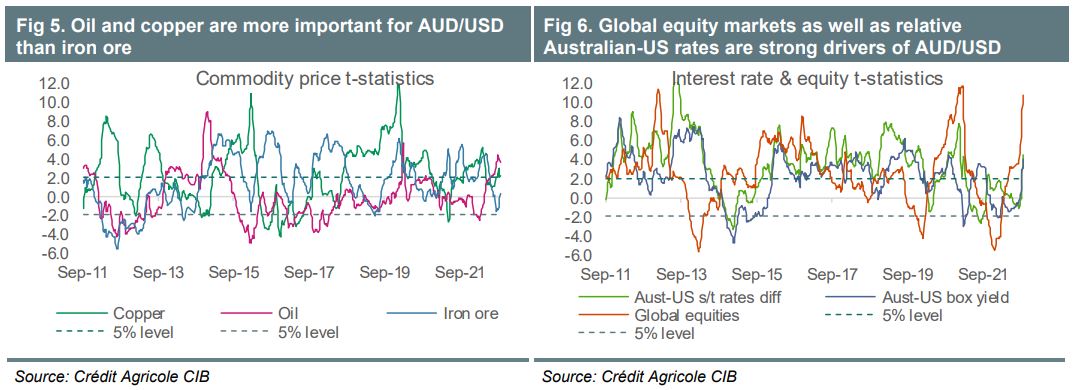

Despite these clogged channels, AUD/USD’s sensitivity to commodity prices remains high, but the importance of iron prices for the exchange rate has declined significantly while the significance of oil and copper prices has risen. The overall sensitivity of AUD/USD to commodity prices has also declined in comparison to that of global equity prices as well as relative Australian-US interest rates. Commodity prices now have less of an influence on AUD/USD than global equity prices, but are on par with relative Australian-US rates for influence.

The Australian economy and commodity prices

Commodity prices impact the Australian economy and therefore the AUD via several channels:

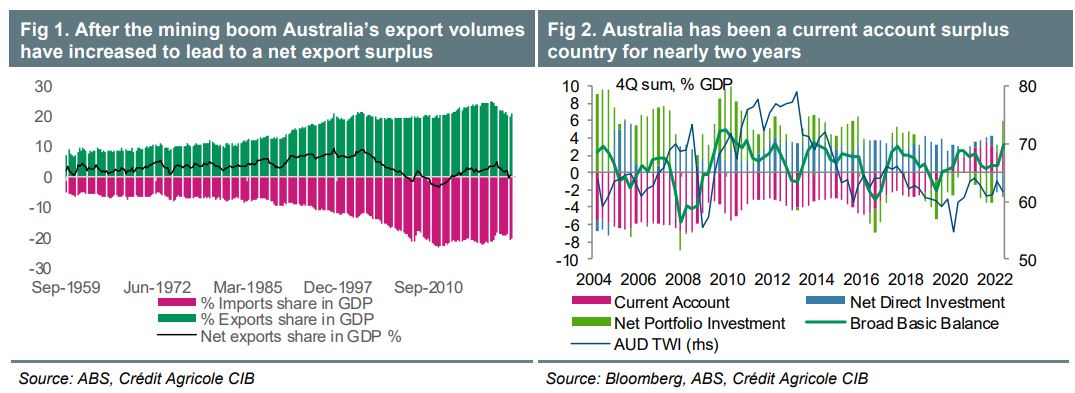

1. Net exports: the most obvious channel is via boosting Australia’s net exports and therefore GDP growth, but also by improving Australia’s basic balance of payments. The volumes of Australia’s commodity exports have picked up significantly after the mining investment boom and as this boom has yielded production dividends. These rising volumes and higher commodity prices have led to Australia becoming a current account surplus country (Figures 1 and 2).

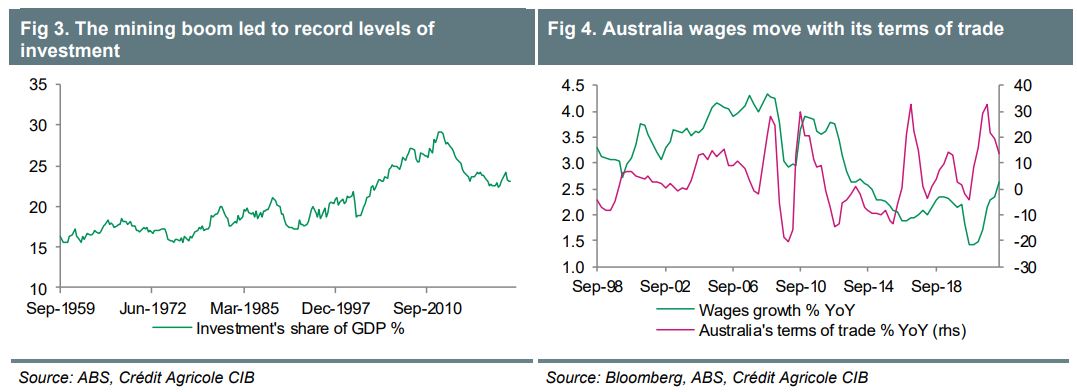

2. Investment: more subtly, higher levels of Australia commodity export prices encourage more investment in mining and extraction capacity by large mining and energy companies, if the rises in commodity prices are considered permanent. This impact on the economy has been blunted after the mining investment boom in the early 2000s and when companies invested in massive amounts of capacity. Indeed, investment as a share of Australian GDP almost reached Chinese levels, peaking at nearly 30% of GDP (Figure 3). Mining and energy companies therefore see little reason to add significantly to capacity in the face of a slowing Chinese economy and a move away from fossil fuels by governments and investors in order to mitigate climate change.

3. Household incomes and consumption: higher commodity prices impact households’ incomes and therefore their consumption via several channels. Higher commodity prices lead to higher mining and energy company profits, which can, as written above, lead to higher levels of investment and therefore employment and wages growth in the mining and energy sectors. If strong enough, mining and energy sector wages growth can bid up wages throughout the economy as different sectors of the economy compete for scarce workers. For existing mining and energy sector workers, higher commodity prices can also lead to higher wages. Higher share prices and dividends as a result of stronger mining and energy company profits can also lead to higher household incomes.

Whether or not all of this leads to strong consumption will depend on whether or not households view their higher incomes as permanent or temporary as well as the income groups receiving the boost to their incomes. If higher commodity prices lead to larger dividends rather than wages, they will likely have a smaller impact on consumption given the lower marginal propensity to consume among the higher income groups that own mining and energy company shares. Indeed, despite higher terms of trade, wages growth has been weakening in Australia since the end of the mining investment boom in about 2012 (Figure 4). Currently, higher living costs and interest rates as well as the threat of a downturn also mean that many wage increases are more likely to be used to meet necessities, higher interest payments or even be saved rather than spent.

4. Public demand: higher mining and energy company profits mean higher tax revenues for both the state governments via royalties and the Federal government via higher corporate taxes revenues. Indeed, this week’s Federal Budget had its deficit hole for the year to June 2023 filled in by about half in large part by higher-than-expected commodity prices. But, with Australia’s budget forecast to remain in deficit to the tune of about 1-2% of GDP for the coming four years and facing a growing structural deficit due to rising aged and healthcare as well as defence spending, the current Australian Labor Party (ALP) government has no room to spend its commodity dividends and will instead use them for Budget repair. State governments are in very similar positions.

Is the AUD still sensitive to commodity prices?

The channels through which commodity prices impact the Australian economy are clogged up, but has this reduced their influence on the AUD? We use our FAST FX model to test the significance of commodity prices, global equity markets and relative Australian-US interest rates in determining the level of AUD/USD.

Commodity prices are still important for AUD/USD, but the exchange rate’s sensitivities have shifted away from iron ore and towards oil and copper (Figure 5).

The importance of iron ore prices in determining the level of AUD/USD has weakened to historically low levels. The impacts of coal and copper are strong, however. This shift in sensitivities is consistent with the changing composition of Australia’s exports. A weakening Chinese economy (especially its property sector) has hurt its demand for iron ore and coal. China’s energy demand has also fallen.

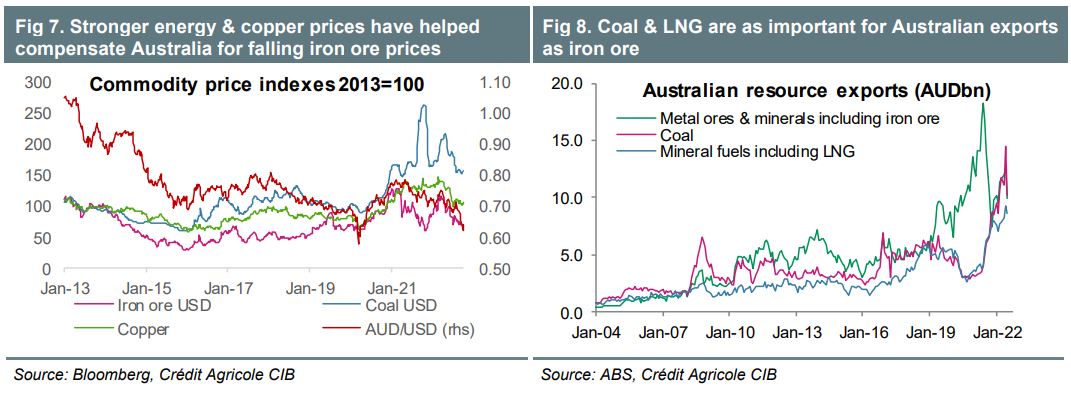

While China has a ban on Australian coal, Australia has found other countries to buy its coal. But, weakening Chinese demand for seaborne coal has weighed on the global coal price and Australia’s export price (Figure 7).

Australia has been compensated for declining Chinese demand for energy and iron ore by strong prices for coal and LNG due to the Ukraine crisis. Coal currently matches iron ore as Australia’s top export earner, and LNG is not far behind (Figure 8). Copper, as a ‘green’ metal, has received support from a push towards greener technologies by governments and investors. Copper prices have nonetheless softened due to weakening prospects for global growth.

The strongest driver of AUD/USD at the moment, however, is the performance of global equity markets and therefore risk (Figure 6). Importantly, the Australian-US short-term interest rate differential and the relative slopes of the AGB and UST yield curves are about on par in importance for AUD/USD as oil and copper prices.

Conclusions

Commodity prices impact the Australian economy and the AUD via their influences on net exports, Australia’s basic balance of payments as well as private and public demand. Higher commodity prices can lead to rising levels of mining and energy company investment as well as boost their profits that can be distributed to Australian households via higher dividends or higher wages. Higher mining and energy company profits also add to state and Federal government coffers via increasing royalties and corporate tax revenues.

These channels are clogged a bit at the moment, however. Mining and energy companies are unwilling to undertake significant investment in capacity following the mining investment boom in the early 2000s and in the face of a slowing Chinese economy. The turning away of governments and investors from fossil fuels also discourages investment in capacity. Households and governments would also currently rather save than spend any fillips they receive from larger mining and energy company profits.

Despite these clogged channels, AUD/USD’s sensitivity to commodity prices remains high, but the importance of iron prices for the exchange rate has declined significantly while the significance of oil and copper prices has risen. The overall sensitivity of AUD/USD to commodity prices has also declined in comparison to that of global equity prices as well as relative Australian-US interest rates. Commodity prices now have less of an influence on AUD/USD than global equity prices, but are on par with relative Australian-US rates for influence.