Policy director at the Centre for Future Work, Greg Jericho, has published an excellent 70-page paper entitled “Inflation: A Primer”, which shows (among other things) that real Australian wage growth has fallen for eight consecutive quarters. This is the longest run of falling real wages on record and comes at a time when real profits – even those outside of mining – have risen strongly.

Jericho argues that Australian workers have, therefore, been the victims of inflation, which has been driven higher by the actions of companies seeking to fatten their profit margins.

Below are extracts from Greg Jericho’s paper explaining these points. They will sound familiar to regular readers of MB.

_____________________________________________________________________________________

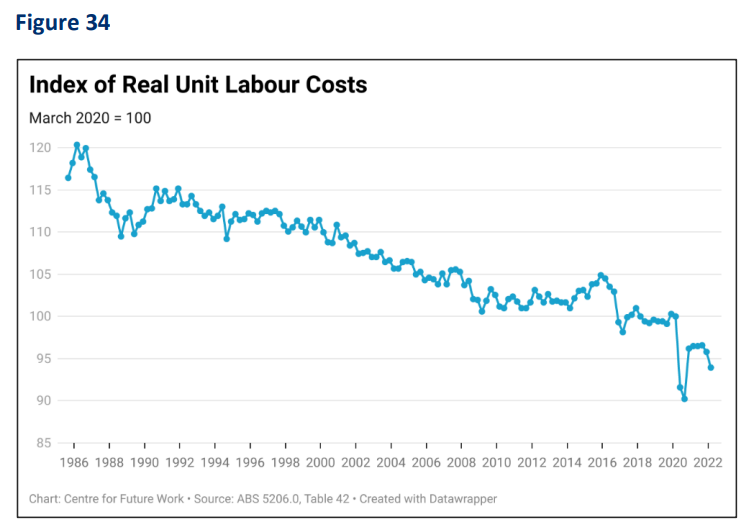

Real unit labour costs (measuring the ratio between real wage growth and productivity growth) in 2022 are actually 6% below where they were prior to the pandemic, further confirming that workers are the victims of this inflation – not its cause.

Indeed, given that the consumer price index grew faster than the wages price index for 8 consecutive quarters to June 2022, it would be rather perverse to argue the wages have driven inflation. But the argument that wage growth needs to be below inflation in order not to be inflationary is faulty on other grounds, as well. In fact, wages should rise faster than inflation, so that real wages keep pace with productivity growth and the labour share of total GDP is preserved. Failure to keep up with inflation, absent any government subsidies or tax cuts, means that workers’ standard of living will fall. Real wages – the value of wages after adjusting for inflation – measures the ability of workers to purchase goods and services with their incomes.

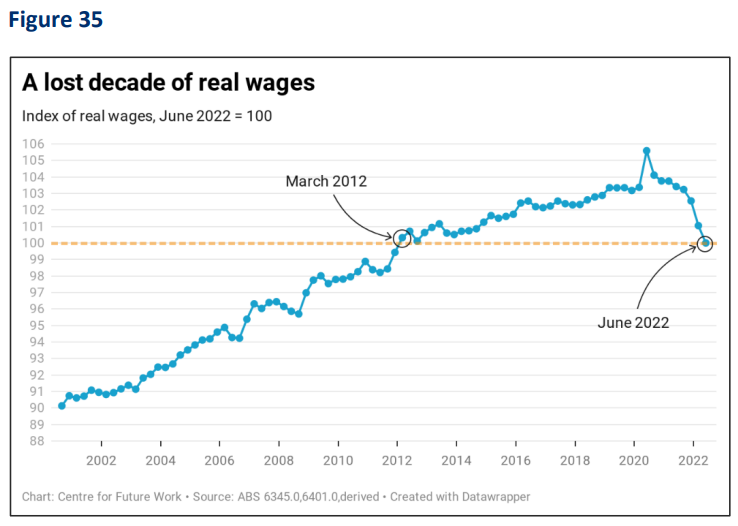

In the current situation, with prices rising faster than wages for an extended period of time, the real purchasing power of wages is falling. So quickly has it fallen in just the 12 months to June 2022, that average real wages were 3.3% below their June 2021 level (Figure 35). In effect workers’ average purchasing power was back to where it was in June 2012. It has fallen even further since.

The reason wages are able to grow faster than inflation without causing inflation is because of productivity growth. Labour productivity measures the amount of real output produced per unit of labour time (an hour, a week, or a year). If workers can produce more real output in an hour for their employers, that means they can earn more per hour (in real, inflation-adjusted terms) with no change in the amount of labour cost built into each unit of output. There would be no pressure on the business to raise the price of their goods to maintain profit margins, and the total amount of profits would also rise thanks to the improvement in labour productivity. So not only should wages be keeping up with inflation: they should actually grow a little bit faster than inflation, so that real wages reflect the ongoing improvements in labour productivity…

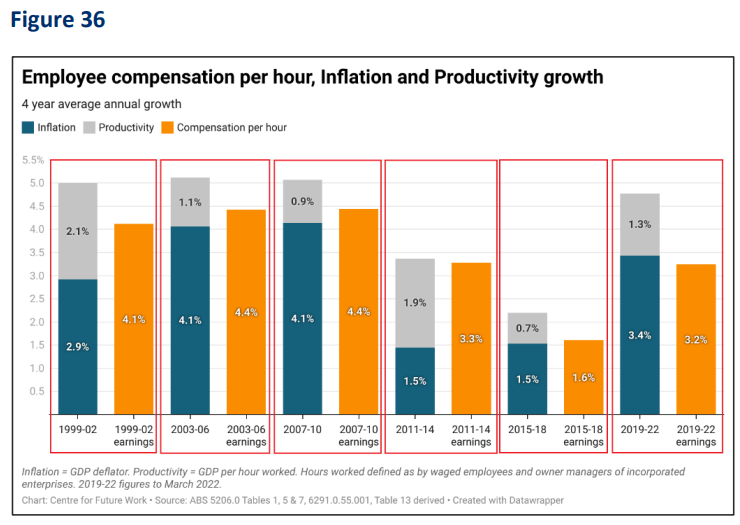

The problem is that while the relationship between real wages and labour productivity is commonly assumed in economic theory, it is not a given in real-world practice (see Figure 36). Wage rises depend on the ability of workers to negotiate better pay; the relationship is more honours in the breech than the observance. Since the turn of the century, there has been no time when sustained wages growth was faster than the sum of inflation and productivity, and hence that wages could be seen as driving inflation. And over the past three COVID-disrupted years, not only have wages not grown faster than inflation and productivity combined – they have actually grown by less than inflation alone. Unit labour costs have thus been growing slower than both actual and target inflation, suggesting that wages are actually reducing inflationary pressures in the economy…

Indeed, while the impact of wages on inflation is often discussed, the impact of profits on prices is rarely even mentioned. One exception was the Bureau of Statistics’ acknowledgment, noted on the release of its March 2022 national accounts report, that “Australian businesses benefitted from rising prices” (ABS 2022). The data indicated that mining company profits rose 14.7%, and that “the share of national income going to profits was a record high of 31.1%”…

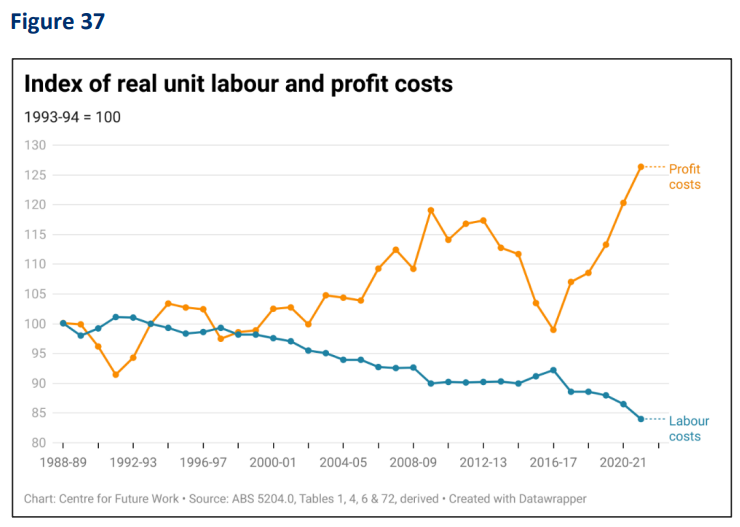

As of the June 2022 national accounts, for example, profits had grown over the previous 12 months by 28.5%, compared to a 6.8% increase in total wages. In the 12 months to June 2022, real unit labour costs have fallen 6.4%, while real unit profits (ie the level of profits per unit of output) had increased 13.1% (Figure 39). Even if we were to exclude the mining sector from profit growth, as some business groups suggest (presumably because recent profits in that sector are somehow “abnormal”), the rise in non-mining profits is still 9.4% – not only well above wages growth, but also inflation. However, given the importance of the mining industry within Australia’s economy, arbitrarily excluding its profits from a discussion of national income distribution is rather absurd. Mining industry profits been greatly outpacing wages in that sector for 5 years now, indicating that current super-profits are hardly a one-off abnormality. Moreover, excluding this most profitable sector from a discussion of profits and wages fairness would be like looking at a sporting league and suggesting the evidence shows all teams have an equal chance of winning – so long as we exclude the team that has won the title every year for the past 20 years.

The evidence is clear that profits are increasing much faster than both labour costs and overall inflation. This suggests that the greatest driver of inflation is firms being willing and able to increase their prices, far above what is “explained” by simply the growth of labour or other input costs…

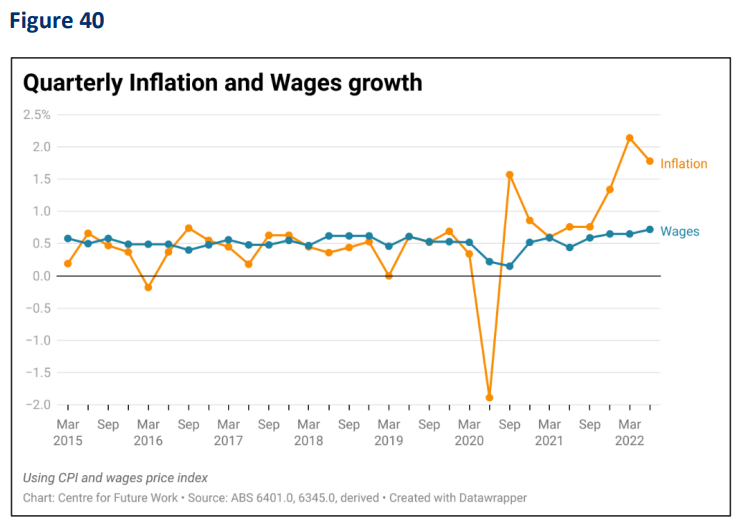

The demand-driven component of inflation is clearly not coming from increased wages. Wages growth remains below inflation, and the CPI has now outpaced the wage price index for 8 straight quarters (the longest such stretch ever; see Figure 40). This period has thus seen real wages decline by 5.3% in that time…

The rising rate of inflation has been accompanied by record levels of profits, contrasting with a large decrease in living standards – especially for lower income households which allocate more of their spending on essential items…

The fear of inflation has motivated monetary policy, and much of fiscal policy, for several decades now in Australia, but this fear has been mostly expressed as a fear of rising wages rather than rising profits. This recent spike in inflation has revealed that wages have been long suppressed; when prices do quickly increase, the cost to workers is felt much more directly than it is to employers.