Roy Morgan Research has modelled the direct impact of the existing 2.50% lift in the Official Cash Rate (OCR), as well as further expected rate increases of 0.25% during each of the next two months.

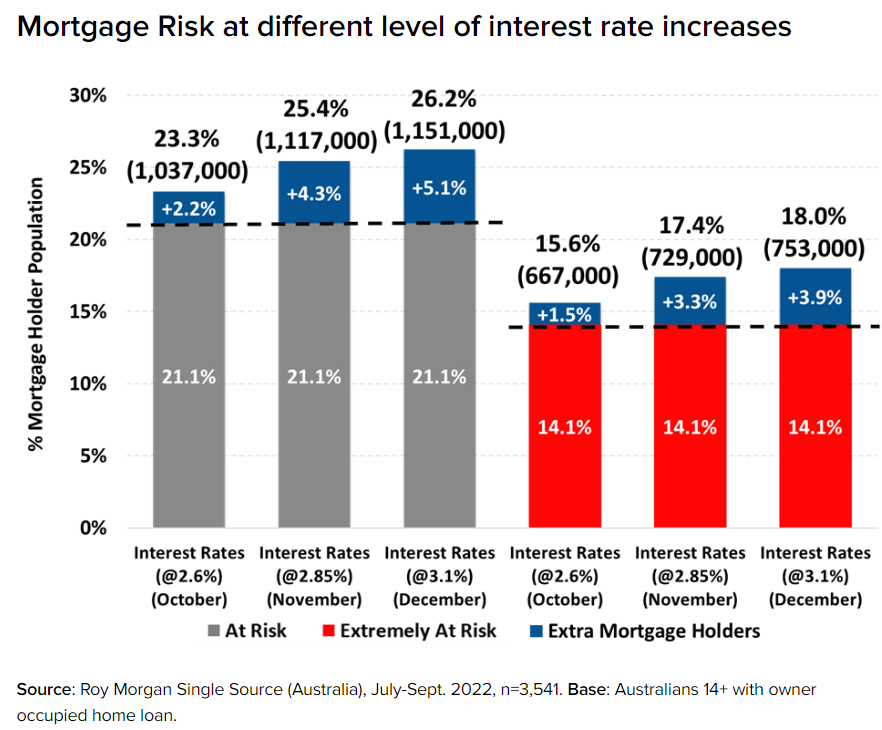

This modelling suggests that over one quarter of Australian mortgage holders would be classified as ‘At Risk’, meaning their mortgage repayments would be greater than a certain percentage of household income (i.e. 25% to 45% depending on income and spending).

This would be the highest share of mortgage stressed households since April 2012:

The RBA’s October interest rate increase means a projected 23.3% of mortgage holders, 1,037,000, would now be classified as ‘At Risk’ – an increase of 89,000 on the original figure of 948,000 (21.1%). The projected figure for October would be the first time in over four years, since September 2018, that over 1 million mortgage holders would be classified as ‘At Risk’.

If the RBA increases interest rates by 0.25% in each of the next two months that would increase official interest rates to 3.1% by the end of the year. These increases would mean 26.2% of mortgage holders, 1,151,000, would then be classified as ‘At Risk’ – an increase of 203,000 on September 2022.

This would be the most mortgage holders classified as ‘At Risk’ for over a decade since April 2012.

Advertisement

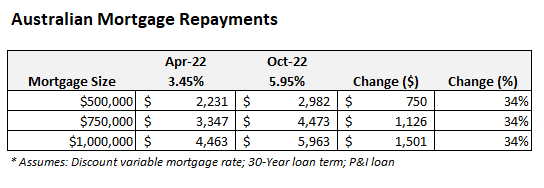

As illustrated in the next table, average variable mortgage repayments have already lifted by 34% versus their level in April immediately prior to the RBA’s first rate hike:

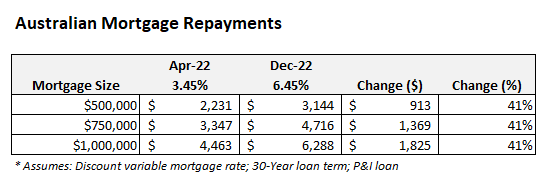

If the RBA was to hike another 0.5% over the next two months, then this would lift repayments a further 7% to 41% above their pre-tightening level:

Advertisement

Remember too that roughly 40% of mortgages taken out over the pandemic were fixed at rock bottom rates of around 2.25%. A significant chunk of these mortgages will expire over the next year and will reset to roughly double mortgage rates (or more), which will push many more mortgage holders into stress.

Given the mega size of recent Australian mortgages, it stands to reason that many of these borrowers will fall into stress amid the steepest lift in mortgage rates in this nation’s history.

Leith van Onselen is Chief Economist at the MB Fund and MB Super. He is also a co-founder of MacroBusiness.

Leith has previously worked at the Australian Treasury, Victorian Treasury and Goldman Sachs.