ANZ New Zealand announced that it will increase its mortgage serviceability interest rate above 8%, which will dramatically impact a large share of fixed term borrowers that are still paying mortgage rates of 2% to 3%:

Speaking to interest.co.nz after ANZ NZ posted record annual profit of almost $2.3 billion, CEO Antonia Watson said 57% of the bank’s home loan book is still paying interest rates beginning with a two or three. Given the bank’s advertised six month, one, two and three year rates are now all well above 6%, chunky increases are ahead for many borrowers when they refix…

She says the 5.8% test rate was in place for about six months last year, “when people were getting home loans at 2.4%”…

It’s now at 7.95% and ANZ says it’ll be increasing to 8.15% “very shortly.”

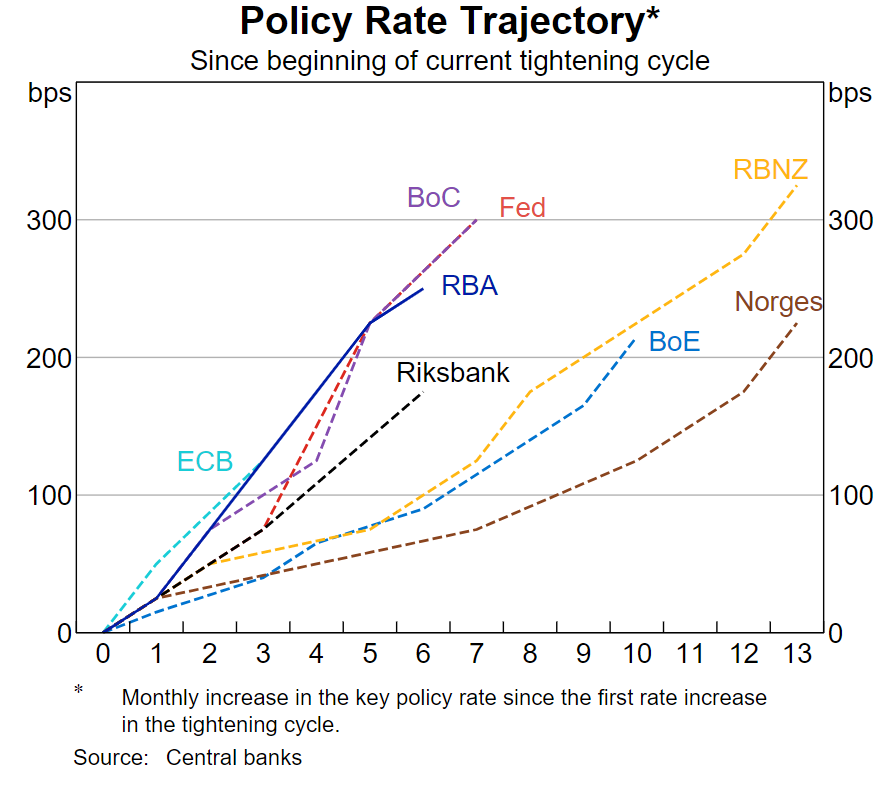

Unlike Australia, where floating rate mortgages dominate, the bulk of New Zealanders are on fixed rate mortgages of two years or less. This means that New Zealanders that originated mortgages at rock-bottom pandemic rates have yet to impacted by the RBNZ’s monetary tightening, which is among the most aggressive in the world:

RBNZ has aggressively lifted interest rates.

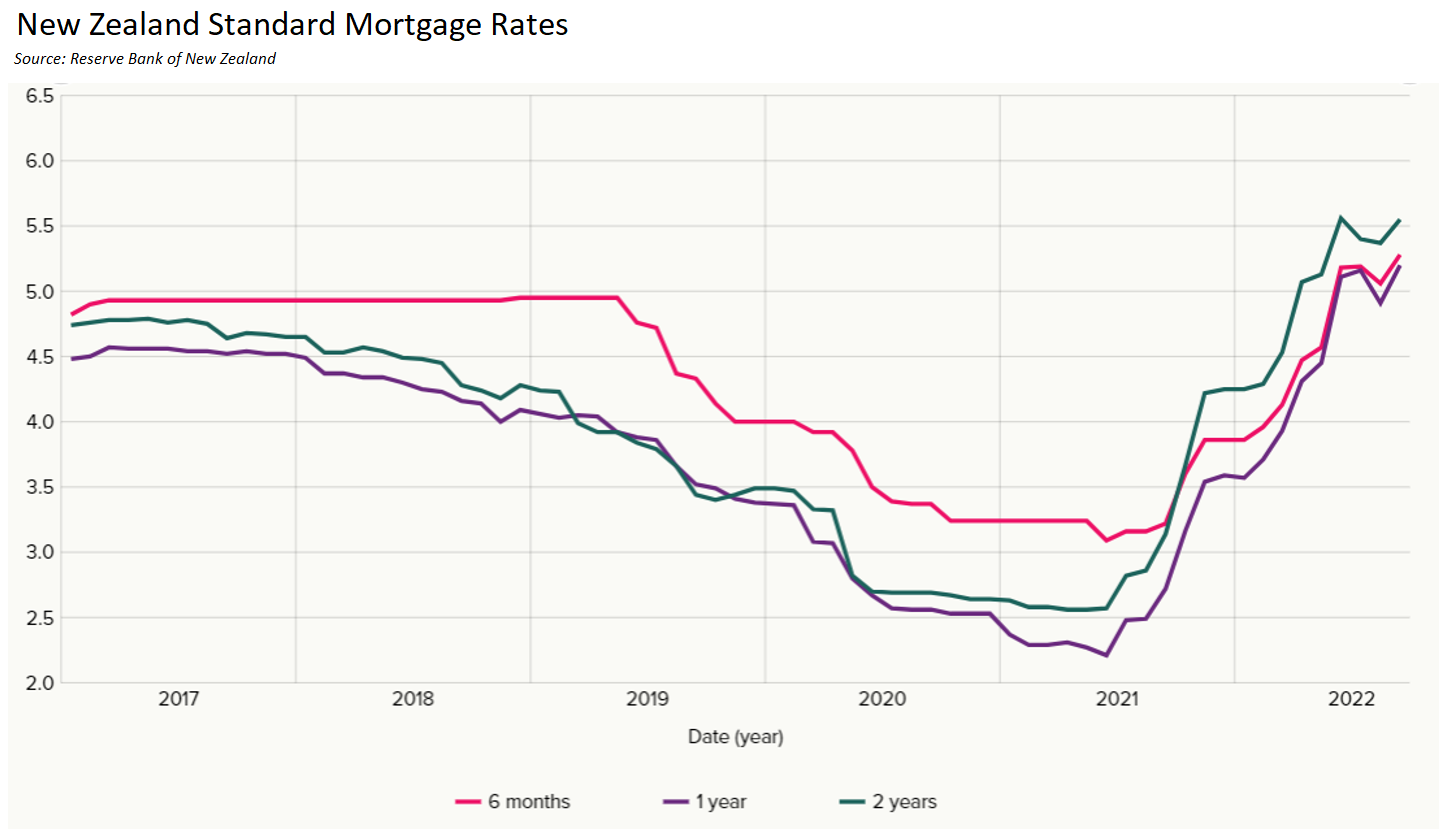

The RBNZ’s rate hikes have lifted one and two year fixed mortgage rates to more than double their pandemic lows, with further rises likely:

Big increases in New Zealand fixed mortgage rates.

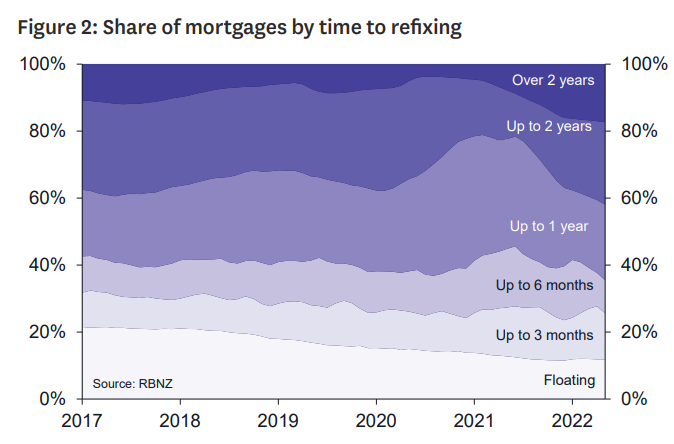

According to Westpac, “around 24% of mortgages will come up for re-pricing by the end of this year, and a further 23% by mid-2023”. Most of those borrowers “will face refixing at substantially higher interest… that’s 2 to 3 percentage points above what it was” when first originated:

New Zealand’s fixed rate mortgage reset.

That is when the impact of the RBNZ’s aggressive monetary tightening will hit hardest.

Household consumption will shrink and the New Zealand economy could be thrown into a sharp recession.

House prices, which have already fallen nearly 13%, will also very likely experience peak-to-trough losses of more than 20%.